This year has seen the rapid growth of the carbon capture, utilization, and storage (CCUS) industry, owing to strong global policy support for projects and initiatives increasing capture capacity.

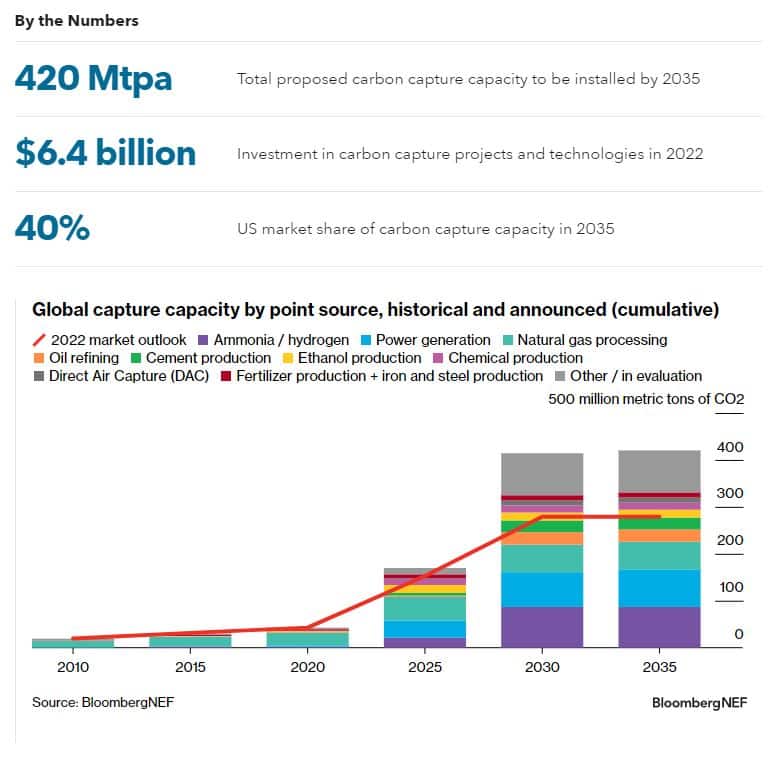

According to research company BloombergNEF (BNEF), the industry will see a 50% increase by 2025. It will reach 420 million metric tons a year by 2035.

Investments in CCUS infrastructure amounted to $6.4 billion in 2022, while funding this year will reach $5 billion.

CCUS Growth and Expansion

The CCUS market has initially focused on natural gas processing. But as decarbonization efforts intensify, it is expanding into carbon-intensive sectors, including power, cement, iron and steel.

BNEF reported that the industry captured over 140 million metric tons per annum (mtpa) from 2022. It is forecasted to grow at a 18% compound annual growth rate and capture 420 mtpa by 2035. This represents 1.1% of current global annual emissions.

The major sectors that will drive CCUS expansion include ammonia or hydrogen production and power generation. Together, they will account for 33% of announced carbon capture capacity.

It is interesting to note that the cement sector has experienced a massive increase in proposed carbon capture capacity – 175%.

It is interesting to note that the cement sector has experienced a massive increase in proposed carbon capture capacity – 175%.

Startups are also developing innovative technologies that can capture CO2 from the atmosphere and lock it away for good by injecting it into the cement.

The BNEF market outlook further noted that the US will remain the leader in deploying carbon capture. It will keep 40% in market share in 2035, followed by the UK at 16% share.

Canada ranks third at 12% while other large country emitters, including Australia, the Netherlands, and China will take 3-4% share.

The Setbacks

While the future of CCUS looks promising, some challenges are just around the corner.

The major hurdle is the lack of transport and storage capacity in deploying carbon capture projects. One solution to this challenge is commercialization as what some national governments and companies are promoting.

Yet, the high costs in constructing storage are not acknowledged by policies such as the EU’s Net Zero Industry Act.

In the US, permits for transport and storage were denied. Recently, the Environmental Protection Agency (EPA) called on states to have their own regulatory frameworks for CCUS. This followed when policymakers questioned the agency’s limited permit issuances.

In the private sector, oil majors aiming to be first movers in advancing carbon capture and storage turn to mergers and acquisitions. For instance, ExxonMobil acquired Denbury, a small-scale oil business running an extensive CO2 pipeline transport network across the Gulf Coast.

In a similar move, Occidental Petroleum also bought Carbon Engineering, a Canadian Direct Air Capture (DAC) supplier for >$1 billion.

Remarkably, the BNEF highlights that DAC is far more costly than previously thought. This carbon capture technology costs up to $1,100 per ton but can potentially drop to $400/ton by 2030. This decrease would be possible if the industry can develop enough supply chains to scale the technology.

The cost of capturing carbon differs across industries. In facilities where CO2 concentration is high, the cost ranges from $20-$28 per ton while for industrial sources, it can go up to $80 a ton of CO2.

Total costs for CCUS can increase to $92-$130 per ton of CO2, and it can swell 2-4x more for transporting liquid CO2.

Industries like cement, iron and steel, and power, which emit a lot of CO2, are using carbon capture methods more. This is driven by the incentives provided by the government in the US and EU, making CCUS more practical.

For instance, building new gas power plants with carbon capture may be less expensive than making power without capturing carbon in Germany by 2024, especially when factoring in carbon price.

The CCUS industry is experiencing rapid growth and diversification across sectors due to strong global policy support. Although promising, challenges such as transport and storage capacity constraints, high construction costs, and regulatory hurdles pose significant barriers. Addressing these challenges will be crucial for CCUS to play a substantial role in global emissions reduction.