Bloomberg Outlook 2024

According to the Bloomberg EV Outlook Report, the global electric vehicle (EV) market in 2024 shows varied progress across different regions and segments. Most notably, while overall EV sales are increasing, some markets are slowing, and many automakers have delayed their EV targets.

We crunched the report and have the following key takeaways, crucial for everyone interested in the industry to know.

Which Regions Are Charging Ahead in EV Sales?

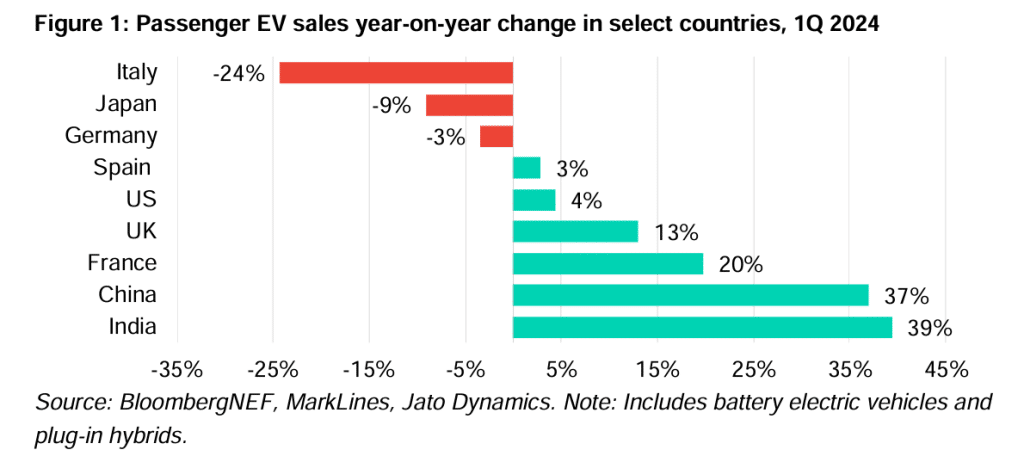

The EV sales growth slowdown varies globally. China, India, and France continue to see healthy growth, while Germany, Italy, and the US face challenges. Meanwhile, Japan’s market is hampered by a lack of EV commitment from major carmakers and no new mini-car models.

Despite the slowdown, global growth in 2024 aligns with BNEF’s forecasts. Some automakers have reduced their electrification targets, citing high production costs, while others, like Kia and Volvo, show strong results.

- Kia aims for 1.6 million EV sales by 2030 and plans to launch an affordable EV3 SUV. Remarkably, Volvo’s EV sales surged 53% in April 2024, driven by the EX30 model.

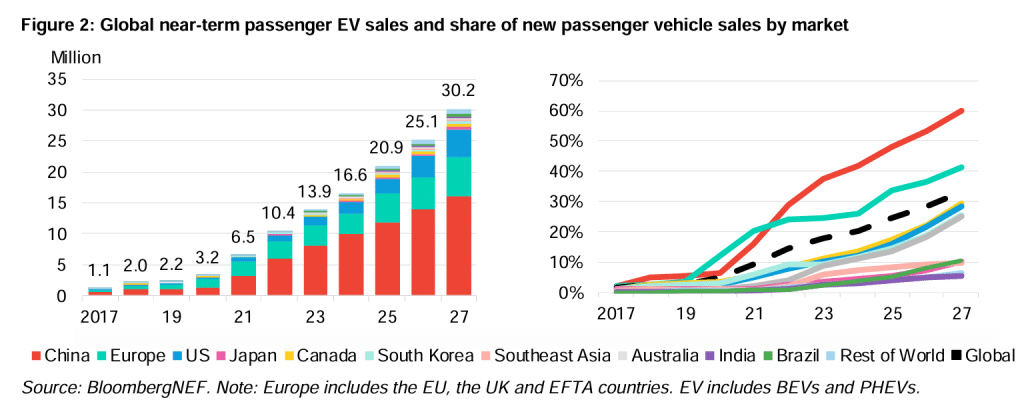

BNEF projects that global passenger EV sales will grow, though at a slower pace, rising from 13.9 million in 2023 to over 30 million by 2027. The annual growth rate will average 21%, down from 61% between 2020 and 2023.

By 2027, EVs will comprise 33% of global new passenger vehicle sales, with China and Europe leading at 60% and 41%, respectively.

The Nordics will reach 90%, while Germany, the UK, and France exceed 40%. The US will see 29% EV sales, slowed by election-related uncertainties. Japan lags behind, but emerging economies like Brazil and India will experience rapid growth.

Overall, the global EV fleet will expand to over 132 million by 2027, up from 41 million in 2023.

- The long-term market outlook for electric vehicles is positive despite near-term challenges.

Economic improvements are expected to drive continued growth, with EVs reaching 45% of global passenger vehicle sales by 2030 and 73% by 2040. However, Southeast Asia, India, and Brazil will lag behind the global average and require stronger regulatory support.

[Disseminated on behalf of Uranium Royalty Corp.]

Learn more about their portfolio of geographically diversified uranium interests >>

Decarbonizing Commercial Vehicles

When it comes to decarbonizing commercial vehicles, including vans, trucks, and buses, electrification is also accelerating.

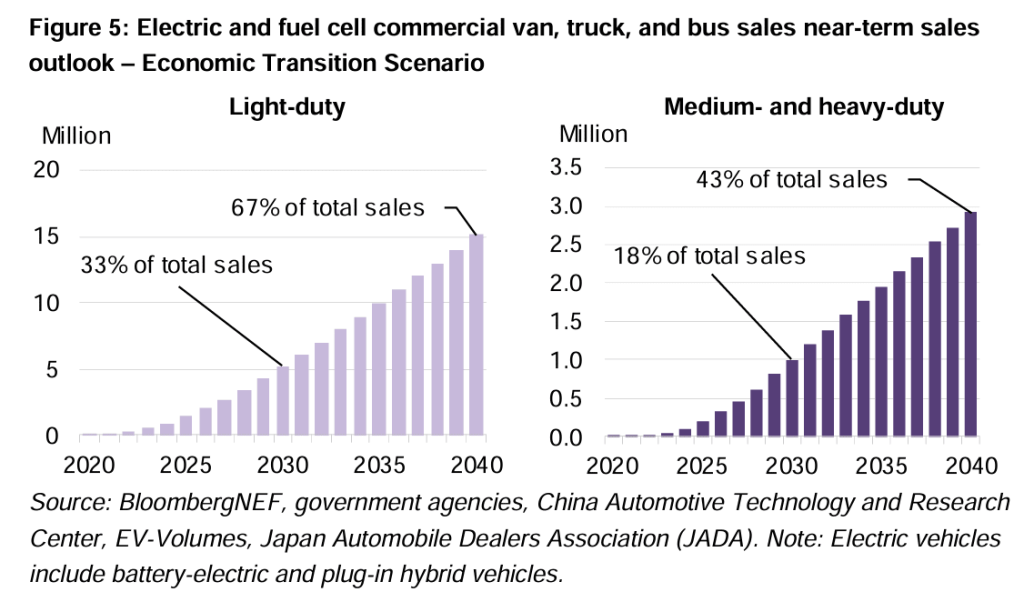

Electric light-duty delivery vans and trucks are quickly gaining market share in China, South Korea, and parts of Europe, while the US still lags. As seen below, the global e-van market will near one-third of sales by 2030, reaching two-thirds by 2040.

Electric heavy trucks will become economically viable for most uses by 2030, with initial adoption in urban areas and later expansion to long-haul routes.

On the other hand, fuel cell trucks will remain viable for some applications, though their future is less certain. Zero-emission trucks will make up 18% of global sales by 2030 and 43% by 2040.

Who Will Drive the Future of Electric Trucks?

New environmental policies in Europe and the US will drive the adoption of electric and fuel-cell trucks. EU CO2 targets suggest high electrification rates by 2030. For instance, municipal buses are rapidly electrifying, expected to exceed 60% of sales by 2030 and 83% by 2040.

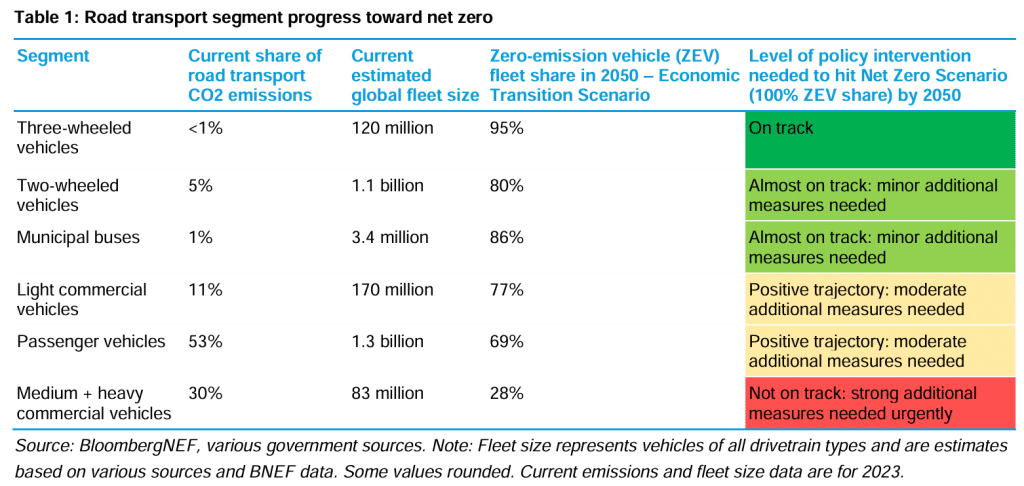

However, global road transport is not yet on a net zero trajectory, and protectionist policies could hinder progress. To achieve zero emissions by 2050, combustion vehicle sales must end by around 2038, with leading markets phasing out earlier, per BNEF analysis.

The Nordic countries are the only ones projected to fully phase out combustion vehicles before 2038 in the Economic Transition Scenario (ETS). Therefore, governments need to balance industrial strategies with maintaining competition and affordability in the EV market. Stronger regulatory pushes are necessary to bridge the gap between the Economic Transition Scenario and the Net Zero Scenario.

- Significant spending is required for both scenarios.

The cumulative value of EV sales across all segments will reach $9 trillion by 2030 and $63 trillion by 2050 in the Economic Transition Scenario. In the Net Zero Scenario, this value jumps to over $98 trillion by 2050.

Governments are fiercely competing to develop local supply chains, with EVs and batteries remaining central to industrial policies for decades.

How Lithium Batteries Are Revolutionizing the EV Market

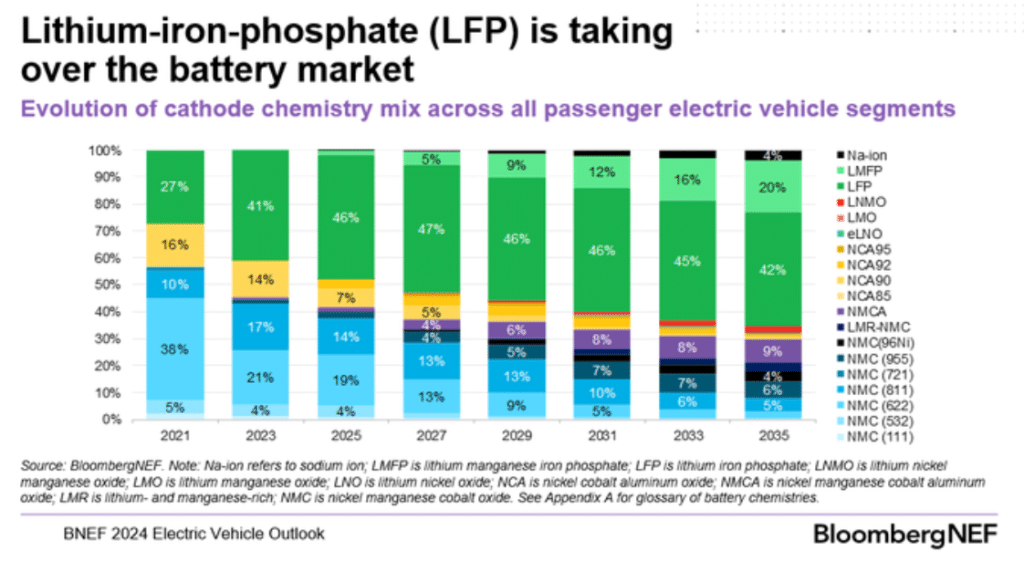

Lithium-iron-phosphate (LFP) batteries are dominating the EV market, reducing the need for metals like nickel and manganese. Competitive pricing is driving improvements in LFP technology, including super-fast charging, cold temperature performance, and higher energy densities.

LFP is projected to capture over 50% of the global passenger EV market within two years, particularly in China, where many LFP cell manufacturers are based. This shift results in lower-than-expected consumption of nickel and manganese, with 2025 estimates for nickel at 517,000 metric tons and manganese at 131,000 metric tons.

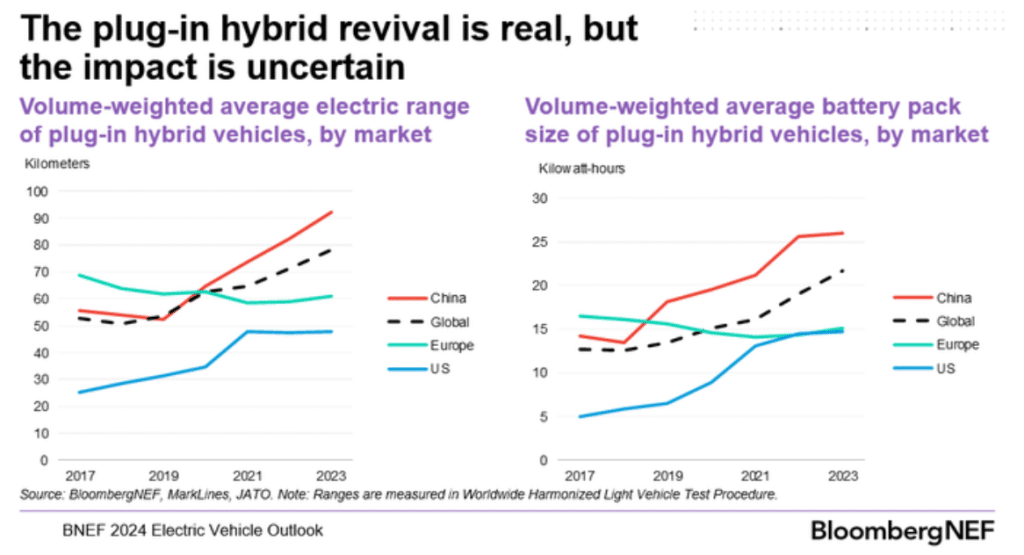

Plug-in hybrids (PHEVs) are experiencing a resurgence, driven mainly by China, which became the largest PHEV market in 2022. The average electric range of PHEVs reached 80 km in 2023, with some models in China exceeding 100 km.

Chinese PHEV battery packs are nearly twice the size of those in the US and Europe, often designed to meet fuel economy regulations. While PHEVs are seen as a bridge to a zero-emission future, their effectiveness is questionable. If they replace BEVs and aren’t fully utilized in electric mode, they could increase oil demand, undermining their environmental benefits.

Charging into the Future: What Does a Fully Electric Fleet Mean?

A fully electric vehicle global fleet could consume twice the electricity the US did in 2023, per BNEF market outlook. By 2050, in the Net Zero Scenario, an all-electric vehicle fleet will require about 8,313 TWh of electricity, double the US’s 2023 consumption.

Despite the increase, EVs can support energy system electrification through smart charging and flexible pricing. The EV charging industry must rapidly mature, requiring $1.6 to $2.5 trillion in infrastructure, installation, and maintenance investment by 2050.

The adoption of EVs and electrification of commercial vehicles are on the rise, driven by new policies and technological advancements in battery technology. However, significant investments in infrastructure and regulatory support are crucial to sustain this momentum and achieve long-term environmental goals.