Do the emerging carbon markets have an integrity problem?

Some certainly think so.

Some experts say as little as 5% of carbon offsets on the Voluntary Carbon Markets (VCM) actually measure up.

Most analysis is less dramatic, but there’s a perception that important weaknesses remain in the market.

One key problem aspect of the integrity problem is additionality. Simply put, offsets need to do something. Selling a carbon credit for something that already exists – say, a piece of prime forest – doesn’t provide a new offset; it just maintains the status quo.

If there is an integrity problem, how does the VCM address it? In the wake of COP 26, a few ideas have come to the fore.

1) Steer the market’s offset appetite in the right direction

Mark Carney, carbon maestro and former Bank of England governor, laid out a vision this week for offsets as the last rung of the net-zero ladder.

Decarbonize, come as to a net-zero carbon emissions policy as possible and then use offsets to finish cleaning up.

The risk right now, as he sees it, is that companies use offsets to avoid any uncomfortable decarbonization, thus reversing the process.

Despite that risk, players have the chance to direct the VCM strategically. Carney’s vision is one option – buying offsets after some of the hard work of decarbonization, or even alongside it. Other options would be to push the price of credits on the VCM higher, forcing entities to use offsets selectively.

2) Embrace the COP 26 framework – rough as it is

Fortunately, the COP 26 Article 6 agreement appears to have achieved at least one major goal; establishing a rough framework or standard for the VCM. Only time will tell, and a lot of the agreement is open to interpretation.

But if the Glasgow Agreement can become a standard – perhaps alongside third-party standards like Verra and the Gold Standard – then the VCM will receive a much-needed legitimacy boost.

Markets are accustomed to using multiple standards; the VCM could easily fit that mold, with offsets offered that conform to the Glasgow Agreement and third-party quality assurances. Broader implementation of those standards will also lead to higher offset prices.

3) Reward quality offsets

The simplest way to address the integrity issue is simply to reward high-quality credits. Easier said than done, but post-COP 26 has already seen an increase in grassroots-led efforts to produce carbon offsets of a high standard.

Those efforts range from Canadian energy producers funding local projects, to Scottish construction companies seeking employee input on carbon-reduction schemes. In the latter effort, the brainstorming campaign itself was a simple offset scheme, planting trees for every idea submitted.

Market solutions to market problems

As is often the case, the best solution to the integrity problem is simply to let markets develop naturally. The VCM is still young and underdeveloped, but the Glasgow Agreement may prove to be a stabilizing force.

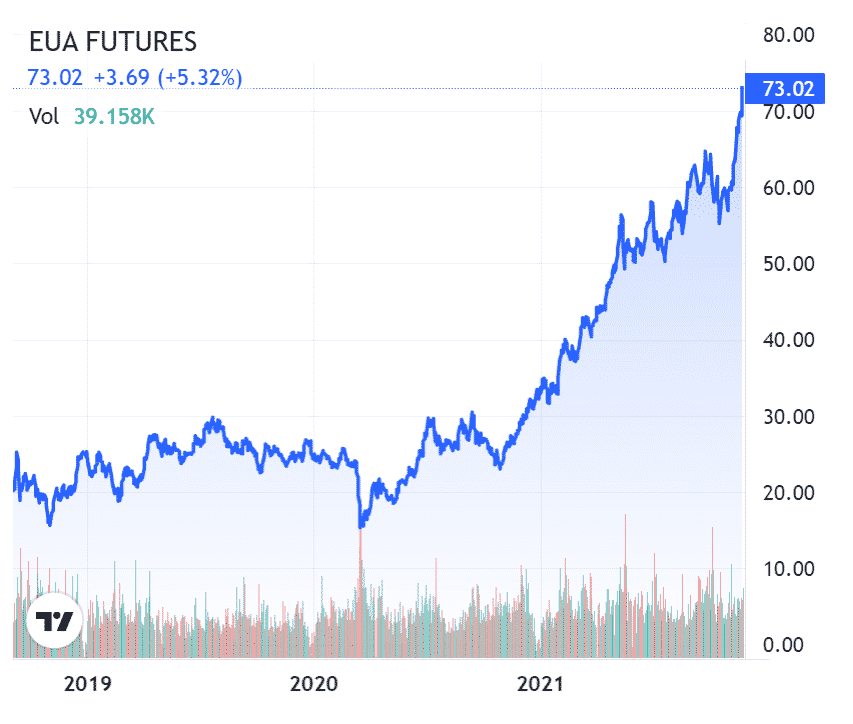

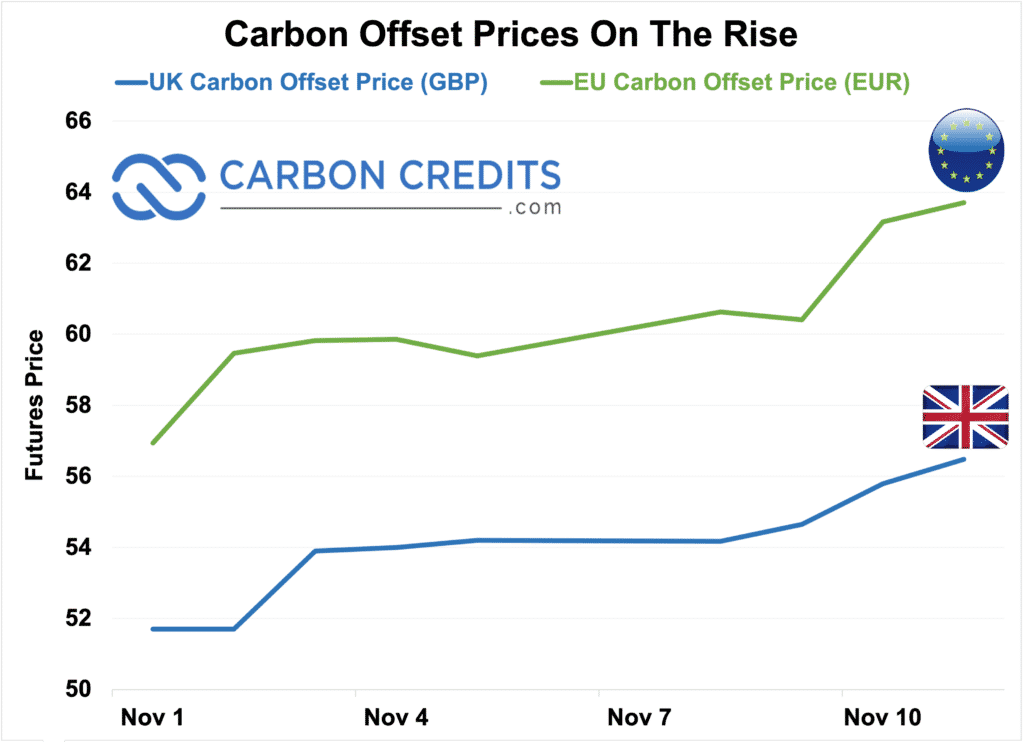

Carbon prices would seem to agree – Australia notched another all-time high for carbon offset this week as global carbon prices continued to climb.

Despite any lingering problems, the outlook for carbon offsets is overwhelmingly positive. The VCM is projected to be worth 100 billion USD by the end of the decade. The price of carbon will need to climb well over $100 per tonne in order to help nations meet their Paris Agreement goals.

Futures prices for the EU ETS have already passed 70 euros per tonne (over $80 USD) and are creeping ever-closer to the $100 mark.

Key point – aside from structural agreements like Glasgow, the VCM is hitting these goals on its own. Markets solving their own problems: the VCM is front and center in demonstrating the power of market forces.