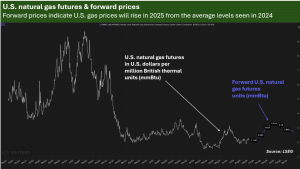

As the northern hemisphere summer winds down, U.S. natural gas markets are already preparing for the upcoming winter and looking ahead to 2025. The markets are forecasting a sharp rise in Henry Hub futures, the benchmark for U.S. natural gas prices.

Data from LSEG shows that prices could average $3.20 per million British thermal units (mmBtu) in 2025. This is a significant increase from the $2.22 average so far in 2024. This projected 44% price jump would represent the steepest annual climb since 2022, potentially increasing energy product inflation trends.

Renewables Rise, but Gas Still Powers the Grid

According to the U.S. Energy Information Administration (EIA), natural gas generates 43% of the nation’s electricity, coal 16%, and nuclear nearly 19%. Renewables provide around 21%, accounting for 84% of new capacity additions in 2023, down slightly from 85% in 2022.

Joey Mashek from Burns & McDonnell highlights that while renewables are growing, natural gas is replacing coal in a one-for-one swap in many states. This transition has led to a 25% drop in CO2 emissions since 2005.

Despite the bullish outlook for the future, U.S. natural gas markets have been relatively downbeat throughout 2024. Prices reached 4-year lows in the spring, as major storage hubs entered the year with unusually high stockpiles. This is due to mild winter temperatures that reduced heating demand.

These bloated inventories have remained around 10% above the long-term average, limiting price progress even during the summer months when increased cooling demand typically drives up consumption.

This past summer, U.S. natural gas consumption surged in July and August due to higher demand for air conditioning. However, prices failed to gain momentum. Recently, they slumped by around 3%, as a storm forecast to hit Louisiana threatened to disrupt power and reduce gas use at liquefied natural gas (LNG) export plants.

U.S. Gas Production Hits Record Highs

Amid the uncertain price landscape, U.S. natural gas production has been strong. Through the first eight months of 2024, average daily dry gas production hit a record 102.5 billion cubic feet per day (Bcf/d), a slight increase from the same period in 2023. This is also nearly 9.5% above the average production rate between 2020 and 2022.

The EIA forecasts that production will rise further, averaging 105 Bcf/d by 2025. Similarly, the demand for U.S. natural gas is poised to grow as well. This is primarily due to the power generation, industrial processes, and LNG export sectors.

According to the EIA, the power sector alone accounts for 38% of total U.S. gas demand, while industrial use contributes an additional 32%. The LNG export sector represents about 10% of total demand.

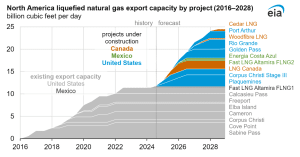

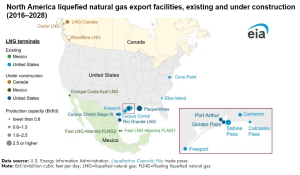

U.S. natural gas exports offer significant opportunities. The country currently has 5 LNG export projects under construction with a combined capacity of 9.7 Bcf/d. These projects include:

- Plaquemines (Phase I and II),

- Corpus Christi Stage III,

- Golden Pass,

- Rio Grande (Phase I), and

- Port Arthur (Phase I).

Developers expect the first LNG production from Plaquemines LNG and Corpus Christi LNG Stage III by the end of 2024.

U.S. LNG exports could hit new records as new export terminals begin operations, tapping into the increasing global reliance on natural gas. Feedgas, the amount of natural gas consumed by LNG export facilities, is projected to rise from 13 Bcf/d to 17 Bcf/d by the end of 2025.

This surge in LNG exports, coupled with the growth in power generation, is expected to tighten the U.S. gas supply, putting upward pressure on prices.

LNG Exports Set to Break Records, Tightening U.S. Supply

The expected 31% increase in LNG demand is just one factor contributing to the tightening supply of natural gas. The power sector is also expected to consume more gas as it continues to replace inefficient coal-fired plants with gas-fired units.

Gas plants produce about 77% less carbon dioxide than coal plants, making them a more environmentally friendly alternative. As U.S. electricity consumption continues to grow, gas-fired power plants will play a significant role in meeting that demand.

This combination of increasing demand and tightening supply is reflected in the current upward trend in forward gas prices. By 2025, the average price for Henry Hub futures is projected to be $3.20/mmBtu, significantly higher than the average in 2024. This increase is likely to motivate producers to boost output, but it could also begin to curb demand. It is particularly true among industries sensitive to rising gas costs.

The Risks and Challenges for Gas-Dependent Sectors

Although higher natural gas prices might prompt producers to ramp up supply, they could also create challenges for certain sectors. The industrial sector, which consumes about a third of U.S. gas, may look to electrify some processes if gas prices climb too high. Additionally, LNG exporters that do not have favorable long-term contracts may find it harder to remain competitive if gas prices continue to rise.

While LNG exporters currently enjoy a price differential that allows them to profit from selling gas to international markets—especially Europe, where Dutch gas prices are 4.6x higher than Henry Hub prices—this gap is expected to narrow. By 2025, the price differential between U.S. and European gas prices is forecast to shrink to 3.5x.

Furthermore, natural disasters such as storms off the Louisiana coast pose another risk. The Gulf region is a critical hub for both natural gas production and LNG exports. Thus, any disruptions due to weather could temporarily reduce demand and complicate the supply chain. This could create volatility in the market, even as overall production remains high.

As U.S. natural gas markets prepare for the coming winter and look ahead to 2025, the outlook for prices suggests a significant increase driven by tightening supply and rising demand. The power generation, industrial, and LNG export sectors will continue to be the primary drivers of gas consumption, with LNG exports set for particularly robust growth.

As the market evolves, it’s worth keeping a close eye on the balance between supply, demand, and the growing role of the U.S. in the global natural gas market.