As the demand for data centers surges, several regions in the U.S. are emerging as significant markets, alongside a notable increase in renewable energy projects supporting this growth, according to S&P Global Market Intelligence data.

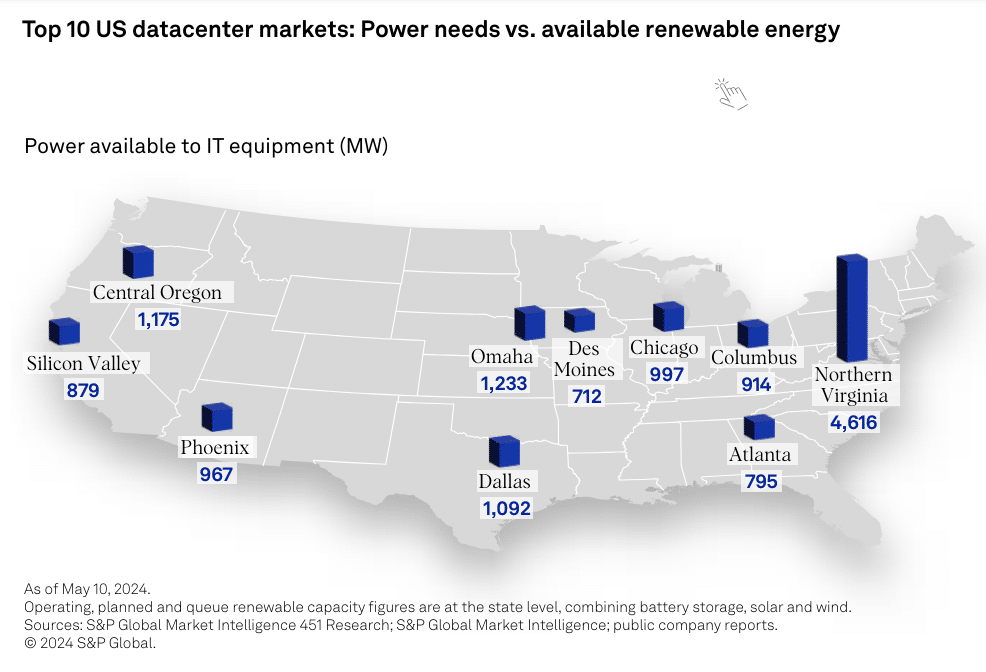

Northern Virginia remains the leading data center market in the US and is second only to Beijing globally. It is set to retain its top position in North America, with 280 data centers in development, adding to the more than 300 already operational in the state.

The region’s data center power consumption is expected to exceed 10 GW by 2028. Dallas and Phoenix are ranked second and third in projected data center demand by 2028. Each of them anticipate to add over 3 GW of capacity in the next five years.

Several other regions are becoming hot spots for data center development, with ten markets projected to surpass 1 GW of demand by 2028. Thanks to the growing presence of tech giants like Google and Meta, Omaha, Nebraska, currently ranks second in operating data center power demand.

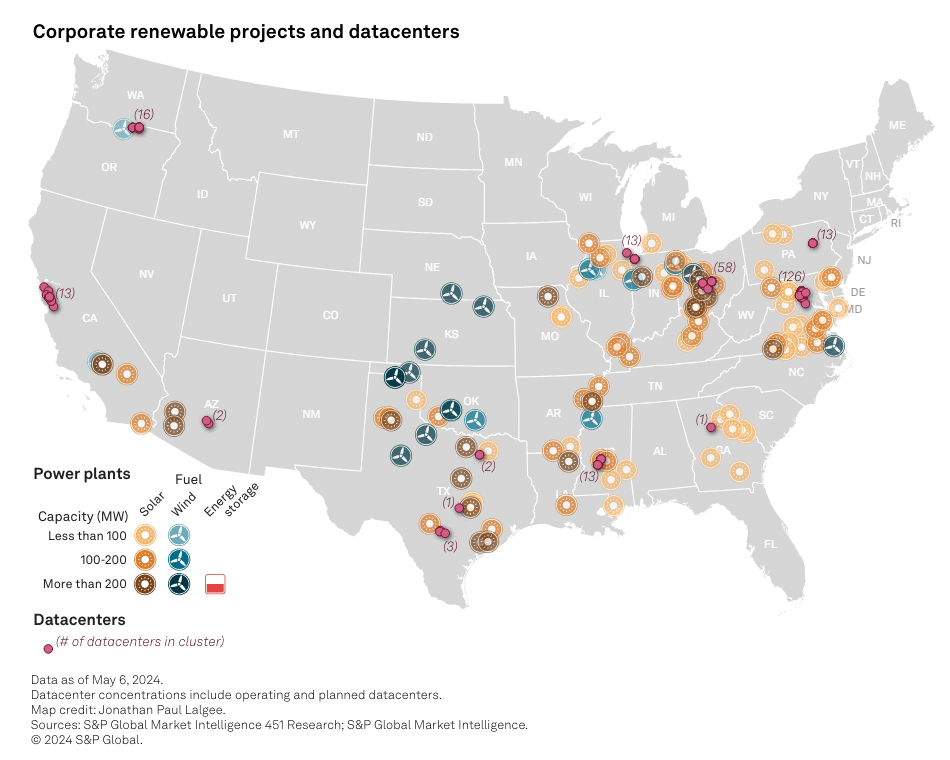

In Texas, data centers will benefit from an extensive array of renewable energy projects. The state has nearly 150 GW of wind, solar, and battery storage capacity in development—the largest pipeline in the US.

Over 63 GW of renewables are being developed in California. Thus, the state’s interconnection queue has expanded to 395 GW of renewable capacity.

The Power Play Among Hyperscalers

Hyperscalers, the large-scale cloud service providers using data centers at the heart of their operations, rank among the top corporate buyers of renewable energy worldwide. As of March 2024, Amazon, Meta Platforms, Google, and Microsoft hold the first 4 spots in contracted renewable energy capacity.

However, these rankings are expected to shift following several major deals announced by Microsoft in April and May 2024. Together, these four companies have contracted over 33 GW of wind, solar, and battery storage capacity in the US. Amazon accounted for about half of this total and Meta adding another 9 GW.

Power projects in 26 states have agreements with these cloud service providers. And their geographic reach is continuously expanding as they develop new data centers.

Currently, Amazon, Google, Meta, and Microsoft collectively own or lease about 9 GW of data center capacity in the US. Based on current development plans, this capacity could nearly triple to just under 26 GW by the end of 2028.

All four companies have set ambitious goals to source 100% of their power from clean energy. With the expanding pipeline of clean energy contracts, the 2028 data center power demand projections may even be conservative.

Data Center Demand by Utility: VEPCO Leads the Charge

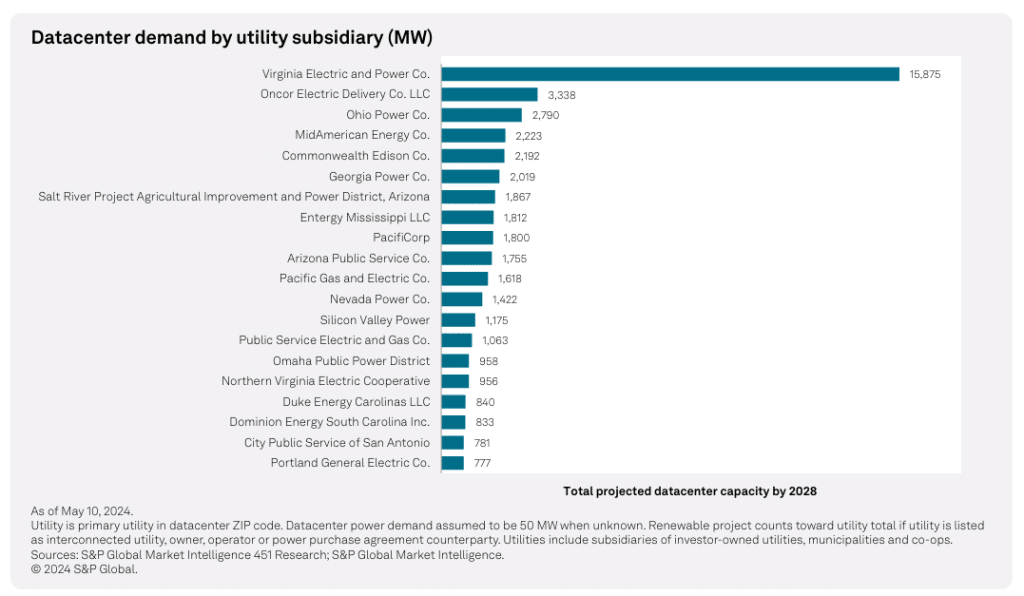

Dominion Energy Inc. subsidiary Virginia Electric and Power Co. (VEPCO), which services Northern Virginia, home to the largest data center fleet in the country, leads all US utilities in energy demand from data centers with 4.6 GW. This demand could surge to 15.9 GW by 2028, nearly 5x that of second-place Oncor Electric Delivery Co.

VEPCO currently has 5.5 GW of operating renewable capacity and an additional 8.7 GW in development. State law requires VEPCO to source 100% of its energy sales from clean energy sources by 2040, alongside meeting the rapidly rising data center demand.

By 2028, the top 10 utilities by data center load could have a combined capacity demand of 35.7 GW. These utilities operate 54.4 GW of wind, solar, and battery storage capacity, with another 52.3 GW in development.

Several have created dedicated green tariff programs for data center companies to purchase carbon-free electricity. The increasing data center load projections are driving these utilities to expand their renewable portfolios.

Oncor, covering large parts of Texas, including the Dallas-Fort Worth area, is expected to see 3.3 GW of data center demand by 2030, though this may be a conservative estimate. Oncor has 40.6 GW of renewable capacity either operating or in development across Texas.

Ohio Power Co., serving the Columbus area where Amazon leads data center development, is projected to have 2.8 GW of data center power demand by 2028. However, Ohio Power currently has just 1.6 GW of combined operating and planned renewable capacity.

Data Center Power Demand on the Rise

The energy needs and power demands of data centers are expected to grow impressively over the next 5 years. As the data center segment evolves rapidly, upward revisions to demand are likely as the power needs of AI become better understood.

The critical question is whether data centers will have access to sufficient green energy supply during this rapid growth.

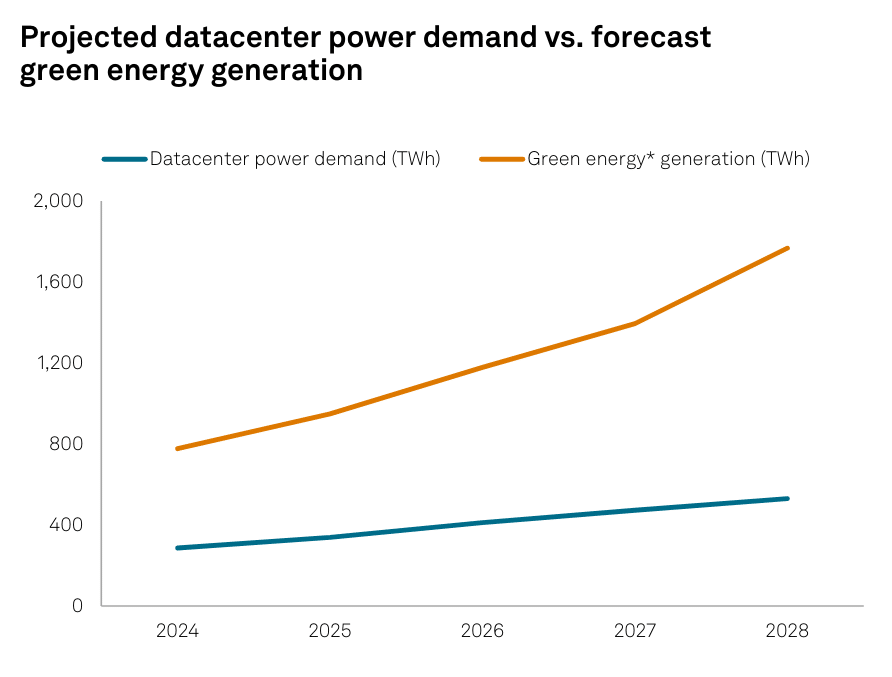

S&P Global Research estimates that firm data center commitments through 2028 will drive an 85% increase in data center demand. This reached an aggregate demand of 60.6 GW and 530.6 TWh of electricity use. This translates to an added demand of 27.9 GW and a usage growth of 244.1 TWh, constituting 10%-12% of US electricity usage.

Baseline estimates suggest that green energy expansion (solar, wind, and battery storage) will keep pace with data center growth rate. Declining costs for green energy and durable federal subsidies will drive significant expansion.

Federal tax credits are fully transferable, allowing data center stakeholders to easily contract with new renewable power facilities. Additionally, renewable mandates enforced by Renewable Energy Certificate markets in many states further support project returns.

The US data center market is experiencing robust growth, driven by technological advancements and the increasing power demands of hyperscalers. As data centers continue to proliferate, the integration of clean energy solutions remains vital to sustain their expansion and environmental impact.