Top research agencies and industrialists are expecting a steady uranium production in 2025. They think demand will grow due to the increasing global need for nuclear energy as a zero-carbon power source.

In 2024, the market saw an activity uptick, with producers reopening mines and planning expansions to meet the needs of nations like the US, Canada, and the EU. Additionally, adoption and investment in small modular reactors significantly increased uranium demand.

So, what’s in store for uranium in 2025? Can supply keep pace with soaring demand, or will it crumble under the pressure? And what’s the price forecast looking like? Let’s study the report to find out the answers…

2024’s Most Significant Uranium Deals

The demand for nuclear energy has risen leaps and bounds as countries seek low-carbon power to meet their energy demands. Electrification, big data centers, and artificial intelligence (AI) are fueling the push for more reliable and clean energy sources.

We have seen many retired power plants being reactivated, and new nuclear construction projects are happening worldwide. This is because, in this new dawn, governments and companies are prioritizing nuclear power as the pillar of the energy transition. And this scenario directly connects with the global uranium supply chain.

Significantly, the global uranium market is responding to this increased demand for nuclear energy. Uranium mining stocks surged in 2024 after top tech companies like Meta, Google, Microsoft, and Oracle announced their entry into nuclear to satiate the energy demand of their data centers. This further shows demand for uranium is going to rise.

One of the most notable deals of last year was Paladin Energy’s acquisition of Canadian company Fission Uranium for CA$1.14 billion. This deal was delayed but recently got clearance from Canadian authorities under the Investment Canada Act. Now Paladin will own Fission’s advanced PLS project in Saskatchewan- Canada’s premium uranium province.

Apart from this, several other uranium deals progressed smoothly:

- Uranium Energy Corp. resumed operations at Willow Creek in Wyoming, marking a key milestone in the company’s production efforts.

- Paladin Energy Ltd. successfully restarted its Langer Heinrich mine in Namibia, achieving commercial production.

- Boss Energy began its first drum of uranium produced at its Honeymoon project in Australia in April 2024.

- IsoEnergy’s acquisition of Anfield Energy expanded its uranium resources significantly. The company’s measured and indicated uranium resources increased to 17 million pounds, with inferred resources now at 10.6 million pounds. This positions IsoEnergy as a potential key player in the U.S. uranium market.

More Power per Punch: Nuclear Energy Outshines Fossil Fuels

Global Rise in Uranium Activity

Russia’s state-owned Rosatom has been offloading its stakes in Kazakhstan’s uranium mines, with Chinese companies stepping in as key buyers. Notable deals include selling 49.979% of Rosatom’s share in the Zarechnoye mine and transferring a 30% stake in the Khorasan-U joint venture to Chinese firms. These moves reflect a shift toward regional and China’s emergence in the uranium market.

Moving on, in Canada, Cameco Corp. has ambitious plans to increase annual output at its McArthur River mine from 18 million to 25 million pounds, alongside extending the operational life of its Cigar Lake mine. Recently, the US Nuclear Regulatory Commission has also approved Urenco USA’s request to amend its license, allowing for uranium enrichment levels of up to 10% at its New Mexico facility.

France has injected €300m ($330m) into uranium major Orano to revamp the country’s uranium industry. Additionally, Brazil is partnering with mining firms to revive uranium production which is stagnant since Indústrias Nucleares do Brasil SA began operating its sole mine in 1982.

Thus, globally, several countries and companies are stepping up initiatives to expand uranium production.

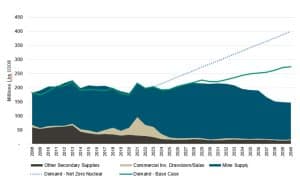

Uranium Supply and Demand Estimates (2008-2040E)

Source: Sprott (UxC and Cameco Corp. Data as of 9/30/2024)

Tax and Trade Tensions: Can Uranium Rise Above the Challenges?

Analysts highlighted several challenges for uranium production, ranging from timeline to geopolitical tensions, tax policies, and technical challenges faced by some uranium mining giants. We have explained these challenges below:

To begin with the U.S., Trump’s statement about imposing a 25% tariff on all products from Mexico and Canada has given rise to some serious concerns. In 2023, Canada supplied 27% of the uranium to U.S. nuclear plants, making it the largest supplier.

However, the U.S. faces challenges in boosting domestic production. According to the US Energy Information Administration, the U.S. purchased 40.5 million pounds of U3O8 in 2022.

Industry experts predict that utilities will push to ensure uranium imports from Canada remain unaffected by potential tariffs, as Canada is a critical and reliable partner.

Geopolitical tensions have further complicated the uranium trade. In May, the U.S. banned imports of Russian uranium, which accounted for 11.8% of its 2022 uranium supply. In response, Russia restricted enriched uranium exports to the U.S. which escalated trade tensions.

Even leading uranium producers faced substantial setbacks. Kazakhstan’s NAC Kazatomprom, the world’s largest producer, reduced its 2025 output target due to difficulties in securing sulfuric acid, a key material for extraction. Similarly, Orano suspended mining activities at its Somair project as it faced financial strains and permit issues.

Uranium’s Future: Predictions for 2025

Uranium prices had a rollercoaster year in 2024.

In November 2024, Uranium spot price retraced to $77.08, according to the Sprott Uranium Report. Despite the dip, prices remain higher compared to historical levels, with the Sprott Physical Uranium Trust helping to stabilize around $80.

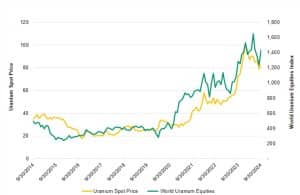

Image: Uranium Miners vs. Spot Uranium (2014-2024)

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

Looking ahead, several factors are driving optimism for uranium’s 2025 future. A persistent supply crunch, growing focus on nuclear energy, global energy policies, and geopolitical shifts will drive demand in the future.

- While short-term volatility may persist, experts predict uranium prices will rebound to $90–$100 per pound by mid-2025.

However, significant investments in new mines, conversion plants, and enrichment facilities will be needed to ramp up uranium production. Moreover, overcoming the challenges we have explained before would also play a significant role in uranium’s bright future.

- Click here for Spot Uranium Prices

- SEE MORE: The Atomic Awakening: Fueled by Uranium