Compliance Carbon Credit Market Overview

The carbon market can be complex and a simple way to understand it is to

separate the two major sectors – Voluntary Markets and Compliance Markets.

This guide focuses on Compliance Carbon Markets, also known as Emissions Trading Systems (ETS).

After reading this, you’ll gain a basic understanding of how Compliance

Markets function, and how to invest within the space.

Executive Summary

Compliance carbon credit prices are largely driven by government policy.

Government strategy will dictate maximum emission limits (otherwise known

as allowances, or credits).

Carbon emitters buy or sell carbon credits based on emissions generated in

relation to their allowance limits.

If they are under their emissions limit, they sell their excess allowances.

If they are over their limit, they buy to cover the shortfall.

Compliance Carbon Market Landscape

The value of the global carbon credit market reached ~$850 billion in 2021,

a 164% increase from 2020.

Currently, there are three major Emissions Trading Systems around the

world. They are:

- European Union’s Emissions Trading System (EU)

- The California Global Warming Solutions Act (USA)

- The Chinese National Emission Trading System (China)

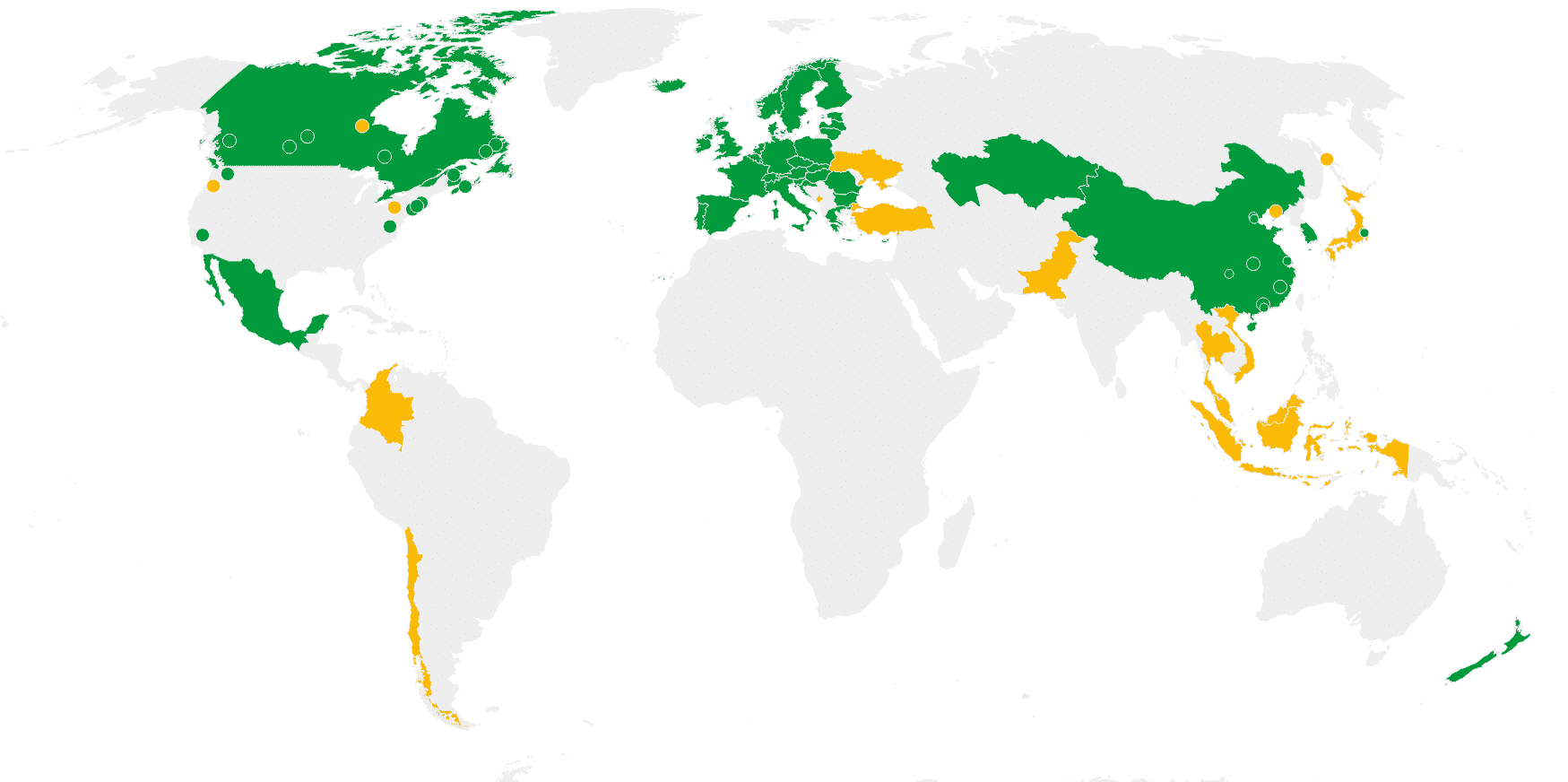

The picture below is a global ETS map that shows the current landscape of

the compliance credit market.

Figure 1: Global ETS Map of Current Compliance Credit Market Landscape

So, let’s break down each major compliance credit market…

Starting with the European Union’s Emissions Trading System (EU ETS) –

which accounted for 90% of the global compliance market.

The European Union ETS

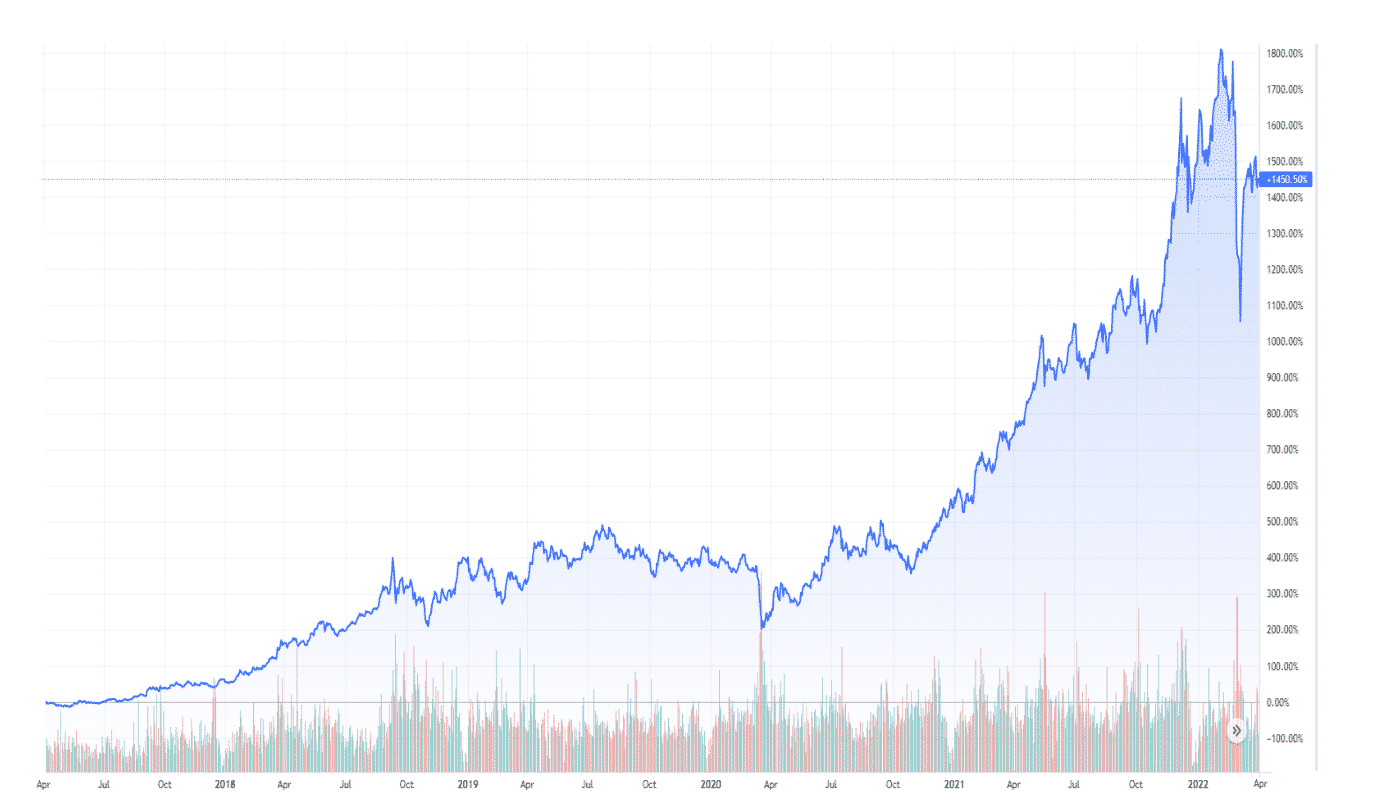

The EU ETS was the first ETS created in the world, operating since 2005. It

is the most liquid carbon futures exchange globally.

In the last 5 years, the EU carbon allowance futures are up over 1,400%,

and up ~270% in the last 3 years alone. As such, it’s one of the

top-performing asset classes worldwide over that period.

Figure 2: European Union Allowance (EUA) Futures Price Chart

EU ETS jurisdiction covers the 27 EU states and 3 European Free Trade

Association states – Iceland, Liechtenstein, and Norway.

The total GHG emissions in this jurisdiction amount to 3,893 mega-tons

(Mt) per year, making it the second-largest ETS in the world.

The sectors regulated under the EU ETS during its first compliance phase were:

- Power stations and other combustion installations with >20MW thermal

rated input - Industries including oil refineries, coke ovens, and iron/steel plants

- Operations that produce cement, glass, lime, bricks, ceramics, pulp,

paper, and cardboard

But there’s only one additional sector regulated during the EU ETS’s second compliance phase:

- Aviation (>10,000 tons CO2/year for commercial aviation; >1,000

tons CO2/year for non-commercial aviation)

Lastly, under its third compliance phase, the additional sectors

regulated under EU ETS were:

- Carbon capture and storage installations

- Production of petrochemicals, ammonia, nonferrous and ferrous metals,

gypsum, aluminum, as well as nitric, adipic, and glyoxylic acid

In total, there are 10,569 power plants and manufacturing facilities that

participate in the EU ETS. These entities have a commitment to:

(1) Reduce GHG emissions to at least 55% below 1990 GHG levels by 2030

(2) Achieve net-zero GHG emissions by 2050

As for the price, carbon on the EU ETS is priced at USD ~$80 per ton but in February 2023, it reached record level of over 100 Euros.

The EU ETS has collected USD $80.7 billion since inception, with USD

$21.8 billion in 2020 alone.

The California Global Warming Solutions Act

This ETS has been operating since 2012 and its jurisdiction covers

California only.

The overall GHG emissions in this jurisdiction amount is 425 million tonnes (Mt) per year.

There are several sectors regulated under the California ETS during its first phase. They were:

(1) Large industrial facilities (cement, glass, hydrogen, iron and steel,

lead, lime manufacturing, nitric acid, petroleum and natural gas systems,

petroleum refining, and pulp and paper manufacturing)

(2) Electricity generation

(3) Electricity imports

(4) Other stationary combustion

(5) CO2 suppliers

While the following sectors were added during its second phase:

(1) Suppliers of natural gas

(2) Suppliers of certain distillate fuel oils

(3) Suppliers of liquid petroleum gas

(4) Suppliers of liquefied natural gas

There are 330 registered entities participating in the California ETS,

which equates to more than 550 facilities. They commit to:

(1) Return to 1990 GHG levels by 2020

(2) 40% reduction from 1990 GHG levels by 2030

(3) Achieve carbon neutrality by 2045.

The current price for carbon under the California ETS is USD ~$30 per ton.

The California ETS has collected USD $14.24 billion since inception,

including USD $1.7 billion in 2020 alone.

China’s Carbon Compliance Markets

Contrary to popular western narratives, the Chinese are serious about

growing their climate-related ambitions. The China National ETS began its operation in 2021.

Its jurisdiction covers all of China. This national ETS expanded on

successful pilots in eight major regions between 2013 and 2016. It operates

on the Shanghai Environment and Energy Exchange (SEEE).

The overall GHG emissions in this jurisdiction amount to 12,301

mega-tons (Mt) per year.

This dwarfs the EU ETS, which has been operating for nearly 20 years.

The only sector regulated in the China ETS is the power sector. However,

the sector scope is expected to expand to cover seven additional sectors.

These are petrochemical, chemical, building materials, steel, nonferrous

metals, paper, and domestic aviation.

There are 2225 registered entities that participate in the China ETS, with

a commitment to:

(1) Reduce carbon emissions per unit of GDP by 18% compared to 2020 levels

by 2025

(2) Reach peak CO2 emissions and lower CO2 emissions per unit of GDP by

over 65% compared to 2005 by 2030

(3) Achieve carbon neutrality by 2060

The current price for carbon on the China ETS is USD ~$9 per ton.

Other compliance credit markets (ETS) that exist today are the Korean ETS,

the Kazakhstan ETS, the New Zealand ETS, the Japan ETS, the Canada ETS, and

the Mexico ETS.

These ETS were not covered because they are not liquid, and are very

difficult for a typical investor to gain exposure to.

Analysis of Risks / Challenges to Major ETS

The risks to compliance carbon credit markets for an investor are two-fold.

The first risk is tied to policy change/error. Policymakers aim to hold carbon prices

relatively stable. If the price is too low, investors are not incentivized

to finance ‘green projects’ which generate credits. If the price is too

high, entities regulated on the compliance side may experience a slowdown

in growth, which is generally bad for the economy.

The second risk is tied to geopolitical tensions and their spillover impacts on various

commodity markets. Here is one example of each risk.

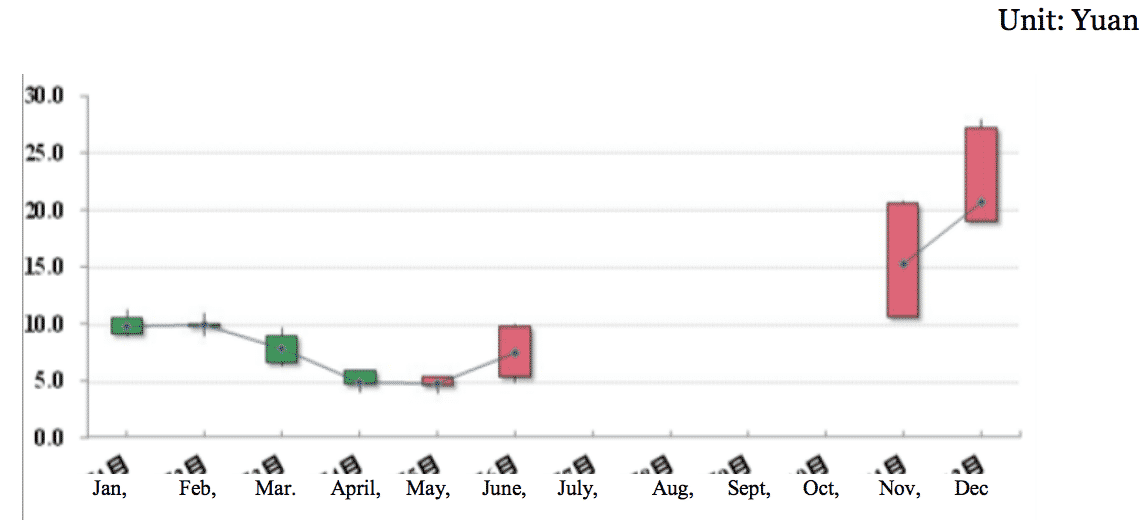

Example #1: Policy Change / Error and Market Response

During the Shanghai Emissions Pilot, the Shanghai government did not

provide policy detail about the next compliance cycle following 2015.

- As a result, the price of carbon fell more than 50% from ~10 yuan down

to ~5 yuan.

In May 2016, the Shanghai Municipal Development and Reform Commission

issued detailed clarifications, specifically around the allowance carryover

policy from the previous compliance cycle.

The carbon price on the Shanghai ETS ballooned to nearly 30 yuan per ton

over the next 7 months once the market gained this policy clarity. Below

you’ll see the month-over-month price trend during this policy change.

Figure 1: Carbon Price during Shanghai Emissions Pilot 2013-2015 (Yuan

per ton)

Example #2: Geopolitical Tensions and Market Response

KRBN, the largest Carbon ETF in the world, experienced substantial price

volatility between late February and early March 2022.

The Russia / Ukraine conflict forced markets to price at the risk of a

geopolitical landscape that would decrease the availability of critical

energy resources.

As a result, commodities such as oil experienced a drastic price increase.

The EU energy markets are tight on supply and they are heavily dependent on

Russian oil/natural gas exports.

The scramble to secure critical ‘dirty’ energy forced the EU ETS market to

price in the potential for non-enforcement of the ETS for some

participating entities.

Additionally, the EU carbon border tax on emissions produced from exports

is set to begin in mid-2022. If Russia/EU trade were to continue as normal,

Russian entities could hedge their EU carbon border tax bill by holding EU

ETS carbon credits.

EU sanctions on Russian assets/exports would eliminate trade between the

countries. This particularly includes the ability or need for Russian

entities to hold EU ETS carbon credits.

Investing in the Compliance Carbon Credit Markets

Diversification is critical to investing in carbon markets. Some of the

opportunities to diversify in this market are:

- Internationally (California ETS vs EU ETS)

- Across compliance cycles within an ETS (EU ETS 2022 futures vs EU ETS

2023 futures) - Compliance vs Voluntary credits (carbon allowance futures vs company

who generates credits)

Diversifying amongst compliance / voluntary credits is the most important.

If you were bullish on gold, would you only buy physical gold?

Of course not.

You’d buy physical gold and a basket of gold miners who had stronger

outlooks for growth relative to their competitors. Carbon credits are no

different.