The Paris Agreement created different ways to fight climate change and the EU’s Carbon Border Adjustment Mechanism (CBAM) is one of them.

Several efforts were made to limit GHG emissions globally. All these measures seek to influence the carbon price tied to producing goods or services that emit CO2.

The main purpose of carbon prices is to reduce carbon emissions, particularly in high emitting sectors. At the same time, revenues from carbon pricing present opportunities for governments and businesses to support the shift to a sustainable economy.

But latest events in the carbon market urged regulators to review their climate policies. And the EU has been very active in this case as it aims to be the kingmaker in the sector.

This guide will explain one of the EU’s latest policy proposals on carbon pricing: the Carbon Border Adjustment Mechanism (CBAM).

But before we discuss the details of the EU’s CBAM, let’s explain first the general term it falls under – the Border Carbon Adjustment or BCA.

The BCA Approach to Carbon Pricing

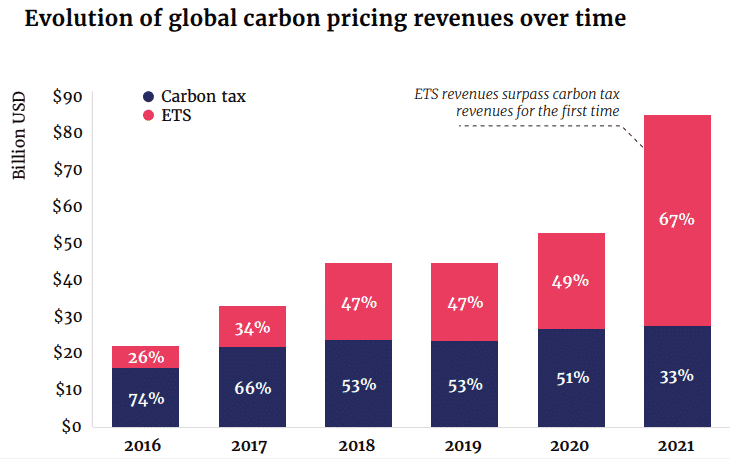

Among the different types of carbon pricing, carbon taxes used to be the highest generating revenue instrument.

But that was before 2021 when revenues from Emissions Trading Systems (ETS) exceeded carbon taxes revenues for the first time. The chart below shows that.

ETS refers to the compliance carbon market where carbon prices are driven by government policy. They’re also called the cap-and-trade emissions system.

Government policies usually inform the maximum emission limits (cap) which are also known as allowances or credits that an entity can emit.

Carbon polluters can buy or sell carbon credits based on emissions they produce in relation to their allowance limits.

If they are below their cap, they can sell their excess allowances. But if they are over their limit, they can buy to cover the shortfall.

Despite surging carbon prices and higher revenues via the ETS, there are still some issues with carbon pricing.

And one of them is carbon leakage which is a big concern for industry stakeholders and politicians alike.

- Carbon leakage refers to the risk where emissions reduced in one country are offset by increased emissions in another country.

It can reduce the efficiency of climate policies by shifting emissions to laxer countries. This can lead to an increase in global carbon emissions.

And so, cross-border approaches to carbon pricing come into play to address the issue of carbon leakage. They’re increasingly recognized by countries and a Border Carbon Adjustment or BCA is one of those approaches.

BCA is an environmental trade policy that applies domestic carbon pricing to imported goods. This carbon pricing mechanism reflects the regulatory costs born by domestically produced carbon-intensive products but not by the same, foreign-produced products.

It’s a policy option that exists in the absence of a global, unified carbon pricing policy or an international agreement on how to deal with it.

Even if BCA is a very recent policy for carbon pricing, some countries are citing it as a means to adopt a direct carbon price. These nations include Ukraine, Uruguay, and Taiwan.

But the EU’s approach would be by far the biggest one – its CBAM.

What is the EU CBAM?

The EU’s CBAM is one form of BCA mechanism for carbon pricing. Its ultimate goals are twofold:

- To reduce GHG emissions and

- To avoid trade advantages and disadvantages as countries have different climate policies’ ambition

CBAM creates a level playing field by making foreign importers face the same costs and incentives that domestic producers experience.

- In essence, it protects the climate ambition and the domestic industry of the country enacting it.

In July 2021, the European Commission (EC) presented the “Fit for 55” legislative package. It contained 13 policy measures to reduce the EU’s GHG emissions by 55% in 2030 from their 1990 levels. It has a main goal to reach climate neutrality or net zero emissions by 2050.

That package includes the CBAM, which will introduce a carbon price on certain products imported into the EU. The EU Council and the European Parliament are responsible for enacting the EU CBAM proposal.

On March 15, 2022, the Council reached an agreement on the CBAM regulation.

As per Bruno Le Maire, French Minister for Economic Affairs, Finance and Recovery:

“The agreement in the Council on the CBAM is a victory for European climate policy. It will give us a tool to speed up the decarbonisation of our industry while protecting it from companies from countries with less ambitious climate goals.”

He added that it will also incentivize other countries to become more sustainable and emit less.

Another main aim of EU CBAM is to avoid carbon leakage. It can happen when production relocates to other countries with weaker climate policies (lower carbon prices).

If that occurs, it can lead to a loss of revenues in countries with ambitious climate goals like the EU.

CBAM will also encourage trading partners to establish their own carbon pricing policies.

How Does the EU CBAM Work

EU’s CBAM is designed to function in parallel with the EU’s Emissions Trading System (EU ETS). In particular, it will gradually replace the free allocation of EU ETS allowances.

EU ETS is the European carbon credit contract that is exchange-traded. It is by far the biggest regulated carbon market trading carbon credits or the EU allowance (EUA).

When an entity buys a carbon allowance from the EU ETS, they gain permission to generate one ton of CO2 emissions. Carbon revenues then flow vertically from companies to regulators.

Under the voluntary carbon market (without government regulation), companies can also buy carbon credits generated by various projects around the world. They range from nature-based projects like reforestation and technology-based carbon removal projects.

The idea is pretty much the same: one carbon credit = one ton of carbon emissions offset or avoided. Firms can also buy credits from different carbon exchanges to voluntarily offset their emissions.

On the other hand, the EU’s CBAM involves applying a carbon price to imports of certain goods to the EU. This price is proportionate to the goods’ “embodied emissions”, referring to the emissions generated during their production. They don’t mean the carbon that the goods physically contain.

Under the CBAM, EU importers must buy CBAM certificates in relation to the goods’ embodied emissions. Just like the current EU allowance, each CBAM certificate equals one ton of emissions.

-

Essentially, the number of CBAM certificates must be equal to the total embodied emissions of the imported goods.

And the price of CBAM certificates should reflect that of the EU ETS allowances in the week before the import of goods.

Once a carbon price has been paid in the country of origin of the imported goods, the required CBAM certificates can be reduced by such paid amount (e.g. the origin country’s own ETS or carbon tax).

CBAM certificates will be valid for two years from the date of purchase.

CBAM’s Application

The EU CBAM applies to the import of electricity and certain goods including:

- steel,

- iron,

- cement,

- fertilizer, and

- aluminum sectors

Initially, it will apply only to Scope 1 emissions or direct emissions. But importers need to report on embodied Scope 2 indirect emissions from electricity consumption as well.

Determining embodied emissions can be done in two ways:

Actual emissions: recorded at production installation level (at country of origin) and verified by accredited verifiers.

Default values: applied where importers cannot show actual emissions generated by the goods. It refers to the average emissions in the country of export, plus a mark-up.

For electricity, calculations will rely on third-country default values. But electricity imports from countries whose markets integrate with that of the EU would be an exception.

The CBAM will enter into force as early as 2023 in a transitional way, and it is likely to fully apply from 2026. During its transitional period (2023-2025), EU importers must meet reporting requirements. But they don’t need to buy CBAM certificates yet.

Once the carbon policy is fully in force in 2026, importers have to pay for CBAM certificates to import CBAM goods.

CBAM Carbon Pricing Impact on Non-EU Countries

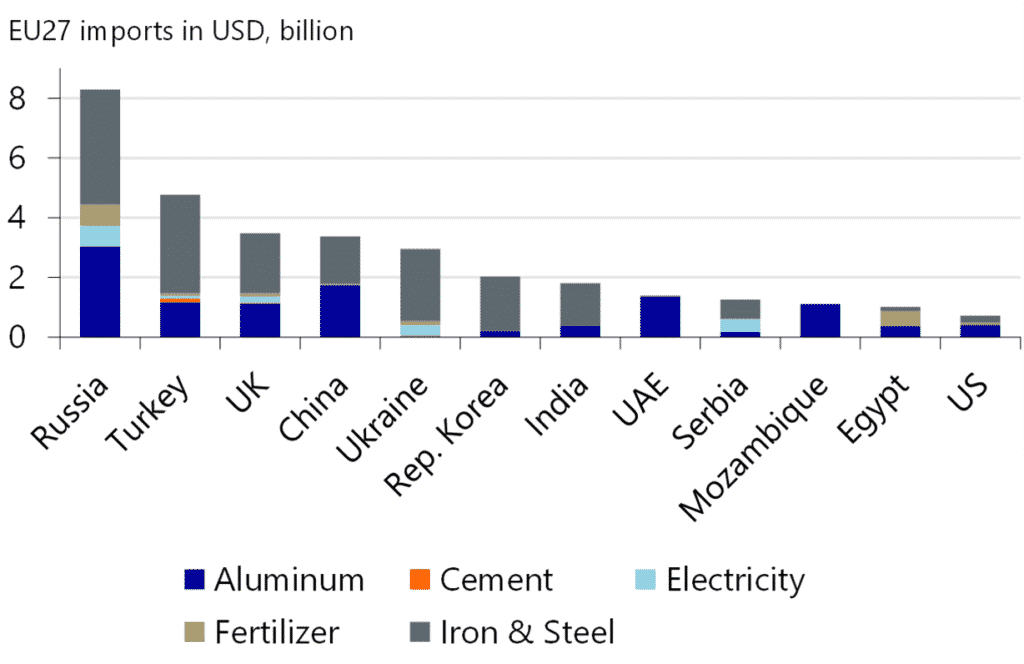

To know which non-EU countries are most likely impacted by the CBAM, studies look at the exports of CBAM products.

Obviously, Russia is the biggest provider of CBAM products to the EU. It is then followed by Turkey, the UK, and China as shown in the graph below.

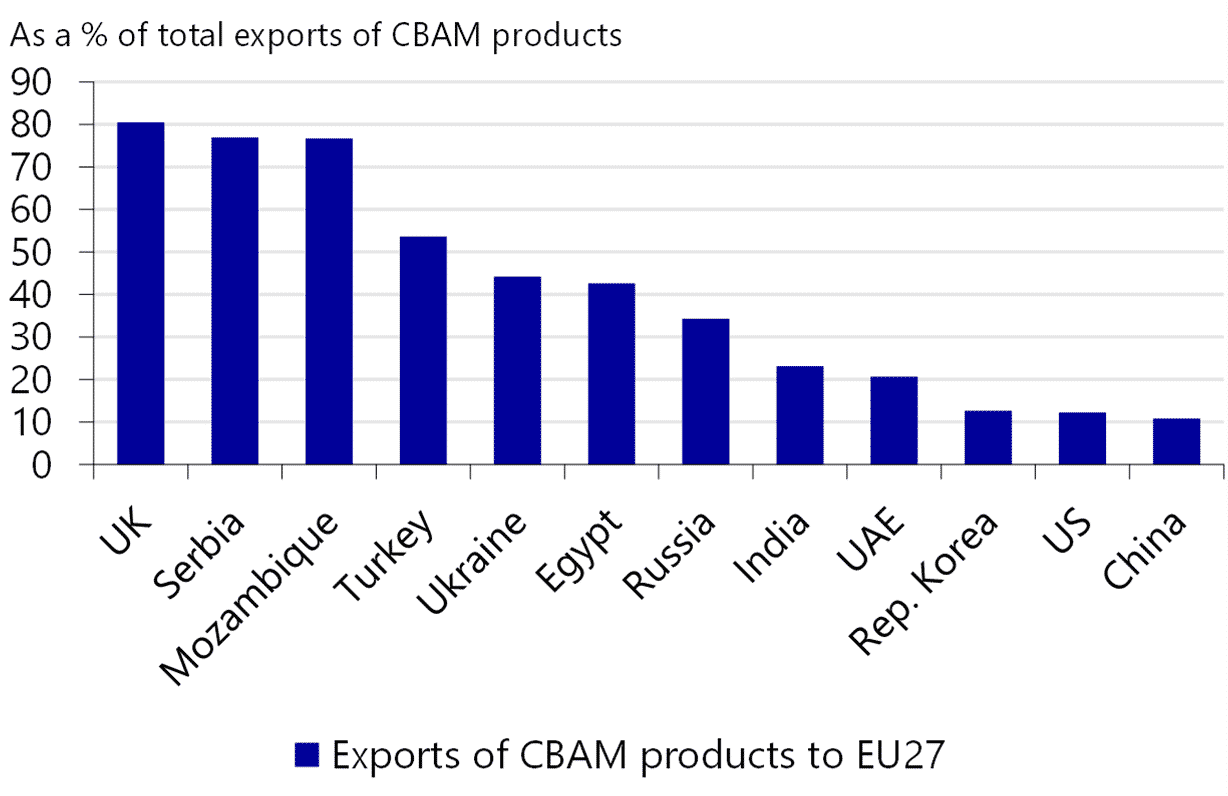

Meanwhile, the most affected non-EU states under CBAM would be the UK, Serbia, and Mozambique as shown in the chart in terms of export percentage. Around 80% of their CBAM exports go to the EU.

It’s important to note that based on the current ETS systems in major trading partners with existing carbon pricing, there’ll be some exceptions in EU CBAM.

For instance, CBAM products from the UK are an exception due to the country’s own emissions system. While imports from South Korea will also have lower CBAM prices than other jurisdictions because of its own carbon pricing.

CBAM Effects on the EU Member States

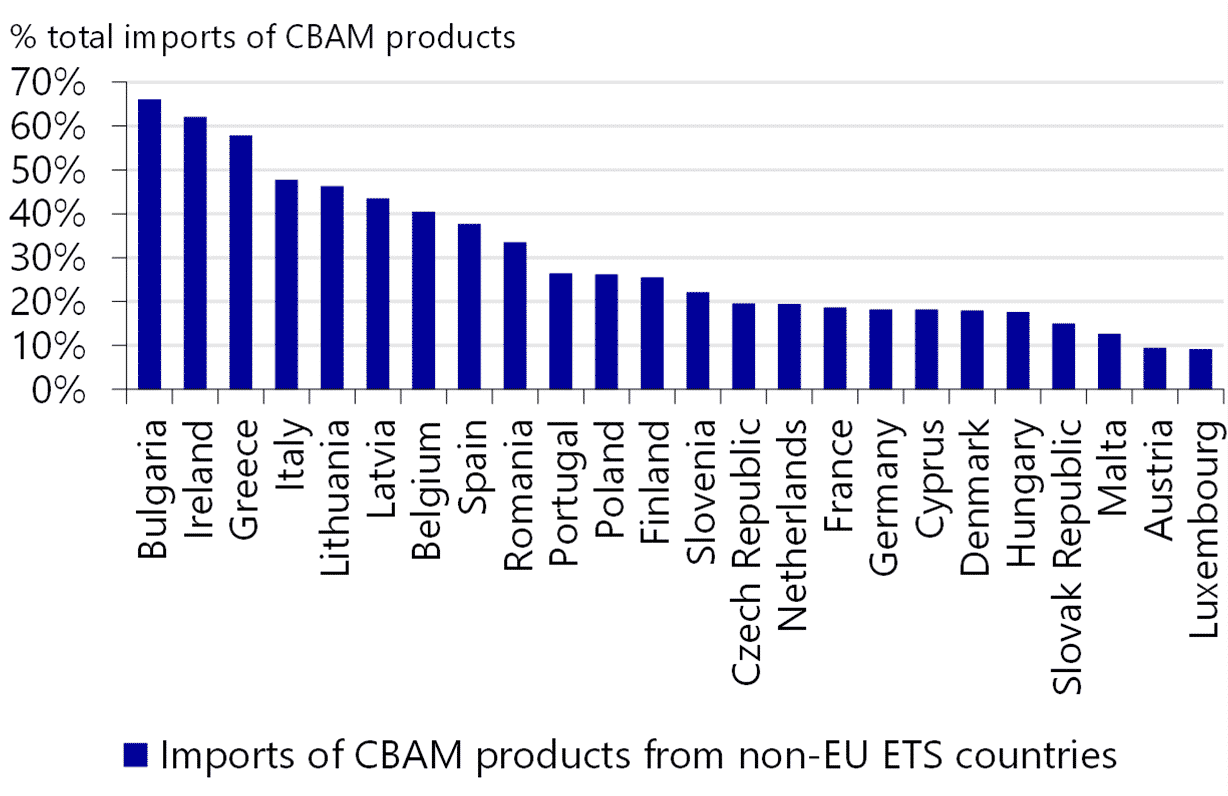

Not only non-EU nations but also the EU member states themselves could be hurt by the CBAM as they may face higher import costs.

In particular, Bulgaria would be the most at risk of having imports taxed by the CBAM. This is because it has a high reliance on CBAM imports from other countries outside the EU.

The chart below shows other EU member states affected by the CBAM carbon pricing mechanism.

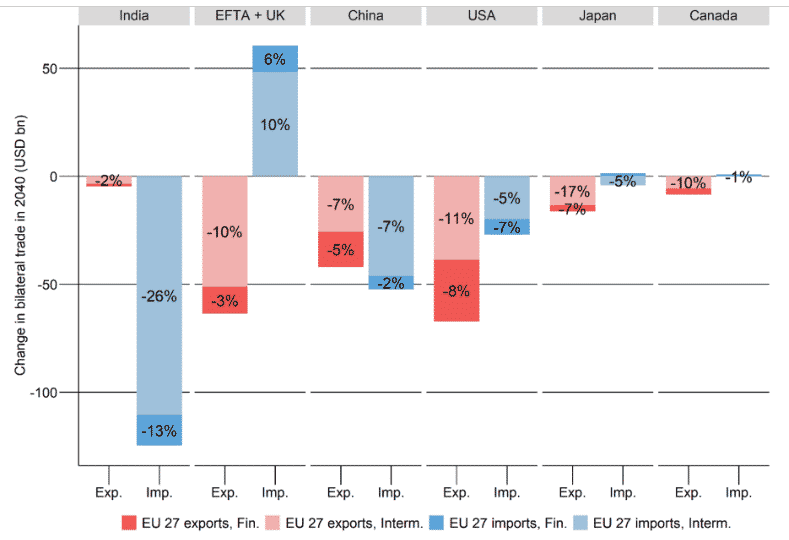

Another possible impact of the CBAM is on the bilateral exports of the main European trading partners of carbon-intensive products.

The figure below shows the impact on EU bilateral exports to (in red) and imports from (in blue) selected countries in 2040. A darker shade refers to the final products exported.

Interestingly, there are trade imbalances favoring Canada, Japan, and the US. The UK and European Free Trade Association (EFTA) are extreme cases. They benefit from low-carbon compensation and so increase their exports.

On the other hand, the CBAM deeply affects India, with a -26% drop in its exports to the EU as projected.

EU CBAM Drawbacks and What it Means for Businesses

The proposal for the CBAM is now under review by the European Parliament and the European Council. Some amendments proposed include making the transitional period shorter and sooner. This is to rid of the EU ETS free allocation much more rapidly.

While the CBAM holds promising changes in carbon pricing in the EU ETS, some find it so complicated. Others said that this BCA policy involves a very complex administrative process.

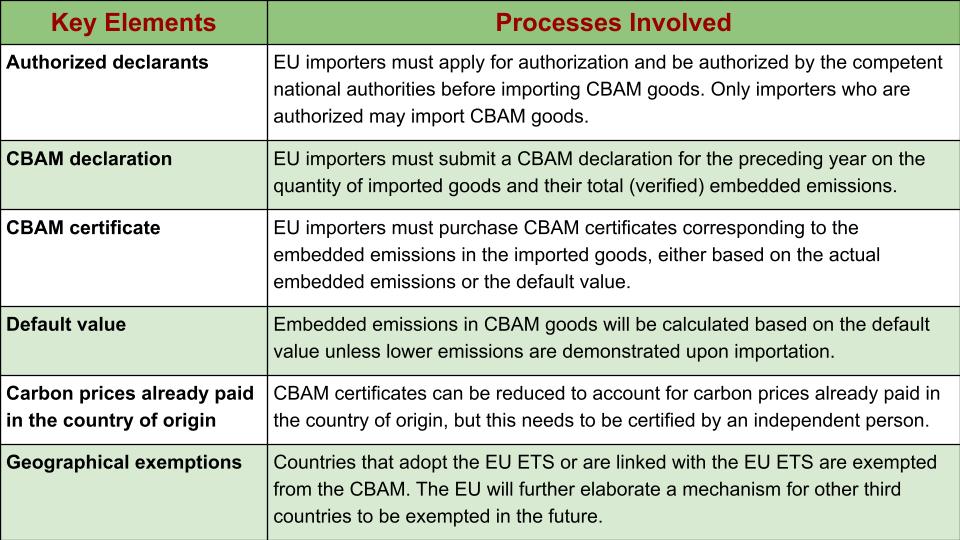

The following are the key elements of the CBAM administration process:

Even if the CBAM still needs approval to become a policy, some proactive steps can help businesses prepare in advance to avoid high administrative burdens.

For instance, companies may:

- Evaluate potential CBAM impact on their operations: purchase data, bill of material, etc.

- Quantify CBAM exposure: value and number of transactions of goods to import/export

- Review global value chain and footprint: ex. determine strategies for investing in manufacturing facilities to reduce emissions

- Identify alternative sources available: goods with lower to no CBAM impact

The EU CBAM and other BCA mechanisms are gradually taking shape. They will make a significant impact on reducing carbon footprint and reaching net zero emissions.

The impact is not only in the EU region but also across the global sourcing and distribution footprint of the businesses covered by the CBAM.

The CBAM carbon pricing may give companies more work to do when it comes to accounting and administration. But it also presents a great opportunity to meet their Environmental, Social, and Governance (ESG) criteria. ESG is one of the criteria that investors look into when making their investments.

You can check out our news page to stay on top of the recent events in the EU carbon market. You can also monitor carbon prices here to help guide your investment decision.