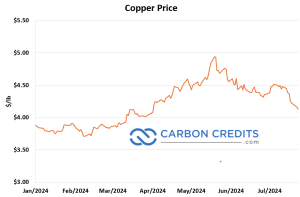

Copper prices fell below $9,000 a ton for the first time since early April due to a global stock market selloff and rising pessimism about demand in China and elsewhere. The industrial metal has dropped by about 20% since its mid-May record high, driven by concerns over increasing inventories and weak conditions in the Chinese spot market.

What Causes the Market Downturn?

Copper is hailed as the economic bellwether because it rises and falls in tandem with industrial production. The metal is also popular as “Doctor Copper”, a slang word for copper’s price to foresee the economy’s overall health.

As seen below, copper price at London Metal Exchange (LME) has been dropping since it hit record high in May.

The falling copper prices is further worsened by a significant selloff in global technology stocks and doubts about the growth of the artificial intelligence industry. The AI industry had previously boosted copper prices due to anticipated surges in data center use and power infrastructure.

Gong Ming, an analyst at Jinrui Futures Co., noted that global growth concerns could drive copper prices lower, although prices might find support around $8,900 due to potential supply risks. Copper dropped 2.2% to $8,900 a ton and was trading at $9,010 at the time of writing. Nearly all metals were lower on the LME, with tin declining 2.6% and zinc losing 1.5%.

Iron ore also declined by 0.9% to trade below $100 a ton in Singapore, with signs of robust supply continuing. According to Liz Gao, a senior iron ore analyst at CRU, weak steel demand and negative steel margins in China are causing mills to reduce production and avoid building raw material stocks.

Despite recent rate cuts by China’s central bank to revive the economy, copper price continued to fall. It marks the worst weekly slump in almost two years, as a modest rate cut in China failed to alleviate concerns about demand in the world’s largest commodities consumer.

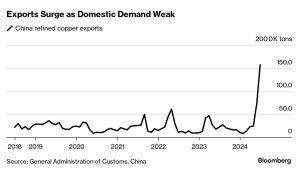

China’s Copper Exports Hit Record High

The red metal dropped for the 6th consecutive day despite China’s efforts to support its economy through unexpected interest-rate cuts. The lack of short-term stimulus from a recent major Communist Party meeting added to investor disappointment.

Ewa Manthey, commodities strategist at ING Bank NV, noted:

“We expect copper and other industrial metals to decline further in the near term. That trend would reflect “a softer demand outlook in China.

China’s refined copper exports reached a record high in June, driven by weak domestic demand, prompting smelters to seek overseas markets. Exports more than doubled to 157,751 tons from May, surpassing the previous all-time high of 102,000 tons set in 2012, according to customs data.

Asia’s largest economy experienced its slowest growth in five quarters in the three months through June. This leads to a 14% drop in global copper prices since mid-May.

The surge in exports is also reflected in the increased copper inventories at LME warehouses, which have more than doubled since mid-May, reaching their highest levels since September 2021. This increase is largely due to the lack of domestic demand.

Benchmark Minerals Intelligence believes that despite spot treatment and refining charges (TC/RCs) at record lows, Chinese smelters are maintaining strong output. Benchmark estimates most smelters in China are loss-making, despite improved by-product credits.

Interestingly, copper prices peaking in May increases scrap copper supply by 20% year-on-year. Most incremental supply went to Chinese smelters, boosting refined copper production.

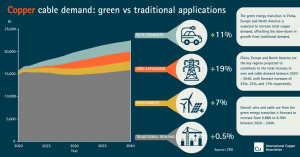

Copper Demand for Clean Energy is Positive

With prices now below the $9,000 threshold, scrap merchants are less willing to supply, and inventories are low. As scrap supply fades in Q3, raw material supply will tighten. Benchmark projects a refined copper production growth rate of 2.3% in H2.

Moreover, though China’s refined copper supply was strong in Q2, consumption growth was weak. High copper prices led to reduced restocking and plant utilization, causing a counter-seasonal stock-build and record exports in May.

Despite short-term pressures, end-use demand indicators are positive: electric vehicle sales are up 32%, and solar installations and grid investments increased 29% and 22%, respectively.