Disseminated on behalf of Li-FT Power Ltd.

The lithium market has entered a period of price decline, mainly because of weaker demand conditions and an oversupply of lithium carbonate in key regions.

The price dip reflects the seasonal winding down of demand typically seen at the end of the year when electric vehicle (EV) manufacturers prepare for a slowdown in post-peak sales. While September saw relative price stability, October’s downward shift reveals how the supply chain dynamics are pressing lithium markets. This is especially true in China’s case, which has been the dominant player in global EV sales in 2024.

- The slowdown underscores the lithium market’s key issue: maintaining demand growth and stabilizing prices amid fluctuating EV sales patterns.

China’s lithium market, the largest globally, saw prices fall by 3.3% in October, settling at about 73,000 yuan per ton. While a brief rebound was observed toward the end of the month, prices continue to reflect the underlying pressures of oversupply. This surplus is compounded by high inventories and the slower-than-expected uptake in EV markets outside of China.

The global market’s current inability to absorb excess supply effectively sets the tone for a persistent price slump, possibly extending into the next several years.

Li-FT Power: Exploring & Developing Hard Rock Lithium Deposits In Canada

Li-FT Power Ltd. (TSXV: LIFT) recently announced its first-ever National Instrument 43-101 (NI 43-101) compliant mineral resource estimate (MRE) for the Yellowknife Lithium Project (YLP), located in the Northwest Territories, Canada.

An Initial Mineral Resource of 50.4 Million Tonnes at Yellowknife.

This maiden estimate is a major milestone for the company and marks a significant step forward in the project’s development. Li-FT Power’s upcoming mineral resource is expected to further solidify Yellowknife as one of North America’s largest hard rock lithium resources.

Click to learn more about lithium and Li-FT Power Ltd. >>

Strategic Adjustments Among Lithium Producers

In response to these challenges, major lithium producers are taking action to manage costs and production levels.

Companies like Sinomine Resource Group have opted to cut production in higher-cost regions. In Zimbabwe, for instance, Sinomine has minimized its petalite mining operations to prioritize spodumene extraction, which has a lower production cost. This shift reflects a broader industry trend, where companies focus on streamlining their operations to protect profit margins as market prices dip.

Another significant strategic move within the industry was the recent acquisition of Arcadium Lithium by Rio Tinto. It is a substantial shift in the company’s approach to the lithium sector. This acquisition is particularly important for Rio Tinto as it extends the company’s footprint in lithium production beyond its existing projects in Serbia and Argentina, allowing it to target markets outside of China more effectively.

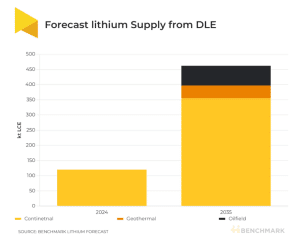

One of Arcadium’s main competitive advantages lies in its exploration of direct lithium extraction (DLE) technology. DLE can revolutionize the lithium market by unlocking reserves in brine deposits previously considered difficult to exploit using traditional methods.

Presently, there are 13 DLE projects in operation, with total output projected to reach about 124,000 tonnes in 2024. According to Benchmark’s data, DLE technology can account for 14% of the global lithium supply by 2035, producing around 470,000 tonnes of LCE. This growth underscores the increasing role of DLE in meeting lithium demand for battery and EV markets.

Global Investments and Expanding Lithium Supply Chain

Investments in lithium production continue to grow despite the current market downturn, which signals optimism about long-term demand.

In October, General Motors made a notable move by increasing its stake in the Lithium Nevada project to 38% with an additional $625 million investment. This initiative speaks of a long-term commitment to secure local lithium supplies. It aligns with the U.S. government’s strategic push to strengthen domestic EV battery production and reduce reliance on imports.

The U.S. Department of Energy has already extended a substantial loan of $2.26 billion to support phase 1 construction of this project. The figure reveals the critical importance of domestic lithium resources for national energy goals.

While traditional methods dominate current production, the lithium market is also increasingly exploring technological advancements. General Motors and other industry stakeholders are actively pursuing direct extraction methods to unlock challenging lithium deposits.

By experimenting with DLE, the U.S.-based Lithium Nevada project aims to reduce environmental impacts and shorten production timelines. These technological investments indicate that despite current pricing challenges, there’s confidence in lithium’s long-term demand potential. More so as EV adoption grows and global green energy transitions accelerate.

Long-Term Market Forecast and Expected Price Recovery

Looking ahead, lithium prices could remain in a tight range. Market experts’ forecasts suggest that the price of lithium carbonate will stay between $9,924 and $11,627 per metric ton until 2026. This projection reflects the industry’s cautious outlook as companies expect that demand growth will take time to balance the current surplus.

The expected long-term supply shortage is largely tied to the anticipated increase in EV adoption and the renewable energy transition. Both of these demand drivers require significant lithium resources.

However, automakers worldwide are adjusting their production strategies to balance profitability with sustainable growth. This brings uncertainty to the exact timing of the demand shift that will absorb today’s excess supply.

In summary, the lithium market in 2024 reflects a complex blend of challenges and opportunities. Prices remain low due to oversupply and fluctuating EV demand, especially outside of China, but the long-term outlook for lithium still holds promise.

The lithium industry’s ability to adapt to today’s market conditions will shape the future landscape of this essential resource, ensuring its place in the global shift toward a sustainable energy future.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.