What is Lithium?

Lithium, hailed as the ‘white gold‘ of modern times, is reshaping battery technology. Known for its lightweight nature, unparalleled electrochemical potential, and high energy density, lithium stands at the forefront of energy storage, driving the global transition to renewable energy. Its journey from a basic mineral to a crucial battery component highlights its pivotal role in technological advancement and sustainable energy solutions.

Amid the push for net zero emissions by 2050, lithium assumes paramount importance. The soaring demand necessitates ramped-up production, urging advancements in mining, refining, and sustainable extraction and processing technologies.

As nations and industries align towards a greener future, lithium emerges as a linchpin in driving technical innovation and sustainability efforts. But before lithium turns out to be this important, it’s interesting that this unique element has a fascinating origin story.

Humanity’s interaction with lithium spans just over 200 years. In the 1790s, Brazilian scientist José Bonefácio de Andrada e Silva discovered two new minerals, petalite and spodumene, on the Swedish island of Utö.

Later, in 1817, Swedish scientist Johan August Arfwedson identified a new element in these minerals. Working in the lab of chemist Baron Jöns Jacob Berzelius, Arfwedson isolated a sulfate that did not contain any known alkali or alkaline earth metals. He named this new element lithium, derived from the Greek word “lithos,” meaning stone, due to its grey, stone-like appearance.

Where Does Lithium Come From?

Some of the lithium found in the rechargeable batteries of our smartphones, laptops, and EVs dates back almost 14 billion years ago.

The lithium cycle begins with magma that contains lithium rising to the Earth’s crust during volcanic activity. This magma cools and crystallizes into rocks such as granites or pegmatites. Over thousands of years, weathering breaks down these rocks, releasing lithium salts that flow into rivers. Most of this dissolved lithium ends up in the oceans.

However, in some high mountainous regions like the South American Andes, rivers terminate in closed basins. Here, water evaporation leaves behind lithium-enriched brine in salt flats, known as salars.

Besides these natural deposits, lithium can also be sourced from oilfield brines, geothermal brines, and clays. Although lithium is not rare, it is highly reactive and never found in its pure form in nature. It ranks as the 33rd most abundant element in the Earth’s crust, with an estimated 98 million tonnes.

What Are The Applications and Uses of Lithium?

Lithium stands out for its extraordinary properties. It is the lightest and least dense solid element on the periodic table, with a standard atomic weight of 6.94. Highly reactive, lithium metal ignites on contact with water, a familiar demonstration in chemistry labs.

Consequently, it is only found in mineral or salt forms in nature. In its metallic form, lithium is a soft, silvery-grey metal with excellent heat and electric conductivity, making it ideal for storing and transmitting energy.

Lithium is so soft it can be cut with a knife and has one of the lowest melting points (180.5 °C) and boiling points (1,347°C) among metals. Its high electrode potential and low atomic mass provide a high charge and power-to-weight ratio, which makes lithium especially suitable for use in rechargeable batteries.

Lithium Batteries: Powering the Future

A critical element in the production of rechargeable batteries, lithium is vital for electric vehicles (EVs), hybrids, laptops, and mobile phones. Lithium-ion batteries are favored by car manufacturers for their ability to store significant energy in compact spaces and quick recharge capabilities.

Notably, lithium iron phosphate batteries are esteemed for their safety and durability, making them ideal for stationary storage and secure EV applications.

In the realm of EVs and lithium-ion batteries, two primary types of lithium, lithium carbonate, and lithium hydroxide, dominate. Major lithium producers often supply both variants to meet the demands of EV manufacturers, alongside catering to other industries requiring diverse lithium applications.

Conversely, smaller lithium companies typically specialize in the production of a single lithium type.

Diverse Applications Beyond Batteries

The versatility of lithium goes beyond battery technology, impacting various sectors that leverage its unique properties. In aerospace, lithium’s lightweight yet robust characteristics enhance fuel efficiency and performance in aircraft and spacecraft.

Incorporating lithium into glass and ceramics yields stronger, more durable products with enhanced thermal resistance, ideal for sturdier and more efficient cookware, tiles, and household items.

Furthermore, lithium compounds serve as high-temperature lubricants, enduring extreme conditions to ensure smooth operation for heavy machinery and vehicles under intense stress and temperature. This wide array of applications underscores lithium’s pivotal role, not only in driving cleaner energy solutions like electric vehicles but also in propelling manufacturing processes and product functionalities across diverse industries.

The breadth of its applications underscores global dependence on lithium for technological advancements and sustainability initiatives. But how exactly is lithium produced or mined?

How is Lithium Mined?

Various ways are available to extract lithium, but two major ones exist to produce industrial lithium.

- Conventional Lithium Brine Extraction

The majority of commercial lithium production today comes from extracting lithium from underground brine reservoirs, primarily located in the Lithium Triangle of the Andes (Bolivia, Argentina, and Chile) and in China.

Lithium brine recovery is a straightforward but time-consuming process. Salt-rich water is pumped to the surface and into evaporation ponds. Over months, water evaporates, precipitating various salts and increasing lithium concentration in the remaining brine.

During evaporation, hydrated lime (Ca(OH)2) is added to remove unwanted elements like magnesium and boron. Once lithium concentration is sufficient, the brine is pumped to a recovery facility where the following steps occur:

- Brine purification to remove contaminants.

- Chemical treatment to precipitate desirable products and byproducts.

- Filtration to remove solids.

- Treatment with soda ash (Na2CO3) to precipitate lithium carbonate (Li2CO3).

- Washing and drying of lithium carbonate to produce the final product.

2. Hard Rock Mining

Hard rock mining, more complex and energy-intensive than brine extraction, involves extracting lithium from minerals such as spodumene, lepidolite, petalite, amblygonite, and eucryptite. Spodumene is the most abundant, providing most of the world’s mineral-derived lithium.

Australia leads in spodumene production, with operations also in Brazil, Portugal, southern Africa, and China. New mines are expected in North America and Finland by 2025. The process involves:

- Mining and crushing the ore.

- Roasting at 2012°F (1100°C), cooling to 140°F (65°C), milling, and roasting again with sulfuric acid at 482°F (250°C) (acid leaching).

- During acid leaching, lithium ions replace hydrogen in the acid, forming lithium sulfate and insoluble residue.

- Adding lime to remove magnesium.

- Using soda ash to precipitate lithium carbonate.

- Lime slurry may adjust pH to neutralize excess acid.

3. New Lithium Production Methods

In the US, commercial-scale lithium production mainly comes from a brine operation in Nevada. However, there’s growing pressure to increase domestic production to secure lithium supplies.

Opportunities for new methods include:

- Direct lithium extraction from geothermal brines (e.g., Salton Sea, CA) and produced water from shale gas fracking (Texas).

- Extraction from lithium-bearing clays in Nevada.

Various production methods are being tested, including:

- Acid leaching with sulfuric and hydrochloric acid.

- Using hydrated lime to remove impurities and neutralize waste before returning it to the environment.

These innovations aim to enhance domestic lithium production and ensure a stable supply of this critical metal.

What is The Current State of the Lithium Market?

In the rapidly evolving landscape of the lithium market, competition is fierce and dynamics are swiftly changing. With the price of lithium batteries constituting 40% of an electric vehicle’s production costs, major EV manufacturers like Tesla, Ford, and BYD are actively seeking cost-effective alternatives.

As global aspirations for emission-free transportation by 2050 intensify, about 30 nations have committed to phasing out the sale of new fuel-engine cars, driving demand for critical EV minerals.

China currently leads the lithium battery production market, but the United States and latecomer South Korea are aiming to challenge its dominance. Amid this dynamic environment, understanding the nuances of lithium is crucial. The next sections explore market and price dynamics, the key players, and the outlook associated with the burgeoning lithium industry.

Asia-Pacific’s Dominance and Its Global Impact

The global lithium market has been significantly shaped by the commanding influence of the Asia-Pacific region, spearheaded by economic powerhouses such as China, Japan, and Korea. Recognizing the transformative potential of lithium, especially in battery technology, these nations swiftly invested in the industry, initially targeting consumer electronics and later expanding into EVs.

Their strategic vision included not only production and processing but also the entire lithium supply chain, from extraction to advanced battery manufacturing. This comprehensive approach has granted them considerable leverage over global battery technology trends and pricing dynamics.

In contrast, North America has struggled to keep pace with this rapid progress. Hindered by a fragmented approach and a lack of cohesive strategy and investment, the region’s lithium industry lags behind its Asia-Pacific counterparts.

This disparity has hindered the development of a robust domestic lithium market in North America. This leaves the region vulnerable to supply fluctuations and pricing determinations driven by Asia-Pacific leaders.

China’s stronghold extends beyond LFP batteries, encompassing lithium-ion battery, cathode, and anode production, as well as lithium, cobalt, and graphite processing and refining.

Despite efforts by governments in Europe, the United States, and South Korea to develop domestic battery supply chains, the majority of the EV battery supply chain is expected to remain concentrated in China for the foreseeable future, maintaining its lead in global battery production capacity until 2030, as projected by the International Energy Agency (IEA).

The Shifting Trend in Lithium Batteries

Tesla and Ford Motor, along with other major automakers, have embraced lithium iron phosphate (LFP) batteries as a cost-effective alternative for some of their EVs, moving away from cobalt-based and nickel-based lithium-ion batteries prevalent in Europe and the US. LFP batteries, identified as the most economical lithium-ion battery type in 2022, now constitute around 40% of global EV production. Demand for this battery is projected to rise substantially in the coming years.

Tesla’s shift to LFP batteries at its Shanghai plant since October 2022 signals a broader industry trend. Its peers like Mercedes-Benz Group AG, Volkswagen AG, and Rivian Automotive Inc. also commit to integrating LFPs into their vehicles.

This shift is largely facilitated by Chinese manufacturers like Contemporary Amperex Technology (CATL) and BYD, which dominate the LFP market, accounting for 99% of global LFP battery production. CATL, in particular, stands as the world’s largest EV battery maker, supplying batteries to Tesla and various other automakers.

Understanding Lithium Prices: Key Factors and Trends

The global appetite for lithium has surged, propelled by the burgeoning battery industry and the widespread adoption of lithium-ion batteries in electric vehicles (EVs). This surge in demand casts a glaring spotlight on the current state of lithium supply, underscoring the escalating consumption rates worldwide.

In this segment, we delve into the intricate dynamics of various factors driving the market, examining how the industry is responding to this mounting need. Key factors such as supply and demand dynamics, mining capacities, geopolitical influences, and technological advancements play pivotal roles in shaping the delicate balance between supply and demand.

Understanding these factors is crucial for stakeholders in the lithium industry, from miners to battery manufacturers and investors. Here are the primary elements that impact lithium prices:

Navigating the Supply-Demand Dynamics

The lithium market exhibits characteristics of an immature market. The supply swings between deficit and surplus due to strong growth and infrastructure development challenges.

With rechargeable batteries constituting around 85% of global demand, the surge in EV uptake has led to soaring demand.

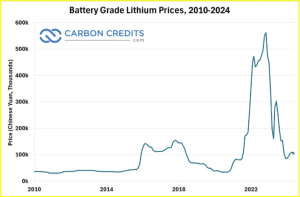

However, the slow pace of infrastructure development has hindered supply growth, resulting in price spikes in 2022. As EV subsidies decrease and prices normalize, we anticipate a controlled decline, settling around $20,000 per tonne by the decade’s end.

Therefore, any imbalance in the supply and demand equation directly affects prices. Any oversupply can depress prices until demand catches up.

Conversely, a surge in demand, driven by the EV boom, can outpace supply, pushing prices up. This is exactly what happened in November 2022 when a record-breaking lithium price rally happened, reaching over a fivefold increase.

Today, lithium spot prices see an even greater increase of 191%+ from July 2025. It jumped from $8,259 per tonne to a whopping $24,086 per tonne in February 2026.

Unraveling Geopolitical Influences

Geopolitical factors significantly influence the lithium market due to the concentration of lithium reserves in specific regions. Countries like Australia, Chile, and Argentina hold substantial lithium reserves and are major players in the global supply chain. Political stability in these countries is crucial. Any political unrest or policy changes can disrupt supply and affect global prices.

Moreover, government policies regarding mining operations, environmental standards, and export regulations can also impact lithium production and prices. Favorable policies can boost production, while restrictive regulations can hinder it.

International trade policies, including tariffs and trade agreements, further influence the flow of lithium across borders. For example, trade tensions between major economies can lead to tariffs on lithium products, affecting global supply chains and prices.

This is what happened recently with the United States announcing its plan to increase tariffs on Chinese imports, including EVs, batteries, and solar cells.

Breaking Down Technological Developments

Advancements in technology have a dual impact on lithium prices by affecting both demand and supply.

- Battery Technology: Breakthroughs in battery technology can significantly influence lithium demand. The development of alternative battery chemistries, such as solid-state batteries or sodium-ion batteries, could reduce reliance on lithium, potentially decreasing its demand and price. On the other hand, innovations that enhance lithium-ion battery performance can boost demand.

- Extraction and Processing Technologies: Technological improvements in lithium extraction and processing can increase supply efficiency and reduce production costs. For example, advancements in direct lithium extraction (DLE) techniques can make it easier and more cost-effective to extract lithium from brine resources, positively impacting prices.

Disentangling Environmental Regulations

Environmental considerations are increasingly shaping the lithium market today.

Stricter environmental regulations on mining practices can limit lithium supply and drive up prices. Mining operations must comply with environmental standards to mitigate their impact on ecosystems and water resources, which can increase operational costs.

Furthermore, the growing emphasis on reducing the environmental footprint of lithium extraction is prompting the industry to adopt greener practices. These sustainable techniques, such as using renewable energy in mining operations and recycling water, may initially increase costs. However, they are expected to lead to long-term sustainability and potentially stabilize prices.

There is also rising pressure from consumers and investors for companies to adhere to environmental, social, and governance (ESG) criteria. Companies that prioritize sustainable and ethical practices may gain a competitive edge, influencing market dynamics and prices.

Quality Challenges in Battery-Grade Lithium Production

As lithium increasingly powers rechargeable batteries, ensuring high-quality lithium products for battery use becomes paramount. Producing battery-grade lithium involves intricate refining processes to meet stringent quality and purity standards.

New refineries typically start with lower-quality technical-grade lithium, necessitating refining improvements to achieve battery-grade purity. Consequently, despite an overall supply surplus, the battery-grade lithium market may face short-term constraints until refining operations are optimized.

What are the Top Lithium Producing Countries?

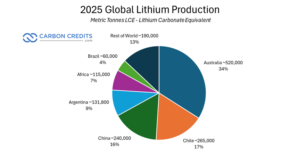

In 2025, three countries – Australia, Chile, and China – dominated global lithium production, collectively accounting for 67% of the total output.

Australia: Leading the Charge

Australia stands as the world’s top lithium producer, sourcing the mineral directly from hard-rock mines, particularly spodumene. Over the past decade, Australia witnessed a remarkable surge in production. In 2013, output stood at 13,000 metric tons, soaring to an impressive 520,000 metric tons by 2025.

Chile: Brine Extraction Expert

Chile follows closely behind Australia in lithium production, albeit with more modest growth. The South American nation primarily extracts lithium from brine sources, with production climbing from 13,500 tonnes in 2013 to 265,000 metric tons in 2025.

China: Closing the Gap

China, also harnessing lithium from brine, has been steadily approaching Chile’s production levels. From a modest 4,000 metric tons in 2013, China ramped up domestic production to 240,000 metric tons in 2025.

Additionally, Chinese companies have expanded their influence in the global lithium market, with three of them ranking among the top lithium mining entities. Tianqi Lithium, the largest among them, holds a significant stake in Greenbushes, the world’s largest hard-rock lithium mine in Australia.

Argentina: A Rising Contender

Argentina emerges as the fourth-largest lithium producer, tripling its output over the past decade. With increased investments from international players, Argentina aims to further enhance its lithium production capacity.

With major producers scaling up to meet the surging demand, particularly from the clean energy sector, like electric vehicle batteries, the lithium market recently experienced a surplus. This oversupply led to a significant price collapse of over 80% from the record highs witnessed in late 2022.

How to Invest in Lithium? Stocks, ETFs, and Derivatives

Due to the nascent stage of the lithium market, the range of investment products available is relatively limited compared to other commodities. Nevertheless, investors can still tap into this dynamic market through two primary avenues: lithium stocks and lithium ETFs.

Lithium Stocks:

Investing in individual stocks remains one of the most direct ways to gain exposure to the lithium industry. However, it’s crucial to recognize that stocks serve as proxies for the market’s performance.

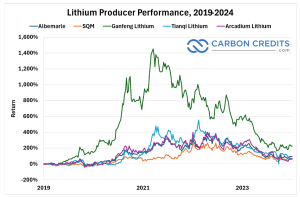

The soaring costs of lithium don’t always translate into corresponding increases in lithium stock prices. Establishing new mining operations can be capital-intensive, and ultimately, a stock’s valuation hinges on the company’s financial health. Despite this caveat, lithium stocks have demonstrated robust performance over the past five years.

Investing in lithium stocks offers several benefits. Firstly, individual lithium stocks provide significant earning potential if the company performs well. Additionally, many lithium stocks pay dividends, offering investors regular income that can be reinvested to bolster portfolio growth.

Moreover, some lithium producers have alternative revenue streams, which can help mitigate the volatility associated with lithium prices. However, investing in lithium stocks also entails certain risks. For instance, putting all investments into one or two lithium stocks can result in a lack of diversification in the portfolio.

Furthermore, the return on lithium stocks is heavily dependent on the financial health of the company, necessitating regular updates on the company’s fundamentals and thorough research.

Lithium ETFs

For investors seeking exposure to the lithium market without the time-intensive task of researching individual stocks, lithium exchange-traded funds (ETFs) offer a convenient option. These ETFs track an index composed of a diversified collection of lithium stocks, providing you with instant access to a broad portfolio that includes both lithium producers and manufacturers.

Here are two prominent lithium ETFs:

- Global X Lithium & Battery Tech ETF (LIT): LIT comprises 39 different lithium and battery stocks. With $4.5 billion in assets under management, this ETF charges an annual fee of 0.75%.

- Amplify Lithium & Battery Technology ETF (BATT): BATT is solely focused on lithium battery providers. Holding $194 million in assets, this ETF charges an annual fee of 0.59%.

Investing in lithium ETFs presents its own set of benefits. ETFs provide instant diversification across a broad range of lithium-focused stocks, thereby reducing the risk associated with individual stock selection. Also, ETFs spread investment risk across a large portfolio of stocks, making them less risky than individual stocks.

Furthermore, similar to individual stocks, some lithium ETFs offer dividend schemes, providing investors with the opportunity for positive cash flow. Nevertheless, there are risks associated with investing in lithium ETFs as well.

For example, during upward trends in the lithium market, returns from ETFs may not be as substantial as those from individual stocks. And take note, ETFs are not free products; providers charge investors a percentage fee for operating and maintaining the ETF.

Direct Investment Through the Commodities Market

For those interested in direct investment, lithium can be traded in the commodities market through futures and options. These derivatives allow you to buy and sell access to lithium as a material, though they come with significant risk and volatility, making them unsuitable for inexperienced investors.

Futures Contracts

A futures contract is an agreement to buy or sell a commodity at a future date for a specified price. There are two types:

Standard Futures Contracts: You commit to buying the actual commodity. If you hold the contract until expiration, you must purchase the physical lithium.

Cash Settlement Futures Contracts: Instead of exchanging the physical commodity, the parties settle the contract’s value in cash.

Options Contracts

Options contracts allow you to trade the value of an asset, with the added flexibility of choosing whether to execute the contract at expiration. This differs from futures contracts, which must be executed regardless of market conditions. When buying an options contract, you pay an upfront fee known as a “premium.”

Investing in lithium offers several pathways, including stocks of lithium producers or users, funds that aggregate lithium-related equities, and direct commodity trading through futures and options. Each method carries different levels of risk and complexity, catering to various investor preferences and experience levels.

Who are the Major Lithium Companies?

1. ALBEMARLE: Market cap: US$14 billion

Albemarle, based in North Carolina, stands as the largest lithium company by market cap and the world’s leading lithium producer, boasting over 7,000 global employees. Following a 2022 realignment, Albemarle now operates two primary business units, with a particular focus on lithium-ion battery and energy transition markets under its Albemarle Energy Storage unit. This division oversees lithium carbonate, hydroxide, and metal production.

With operations spanning Chile, Australia, and the US, Albemarle holds a diverse portfolio of lithium mines and facilities. In Chile, the company produces lithium carbonate at its La Negra conversion plants, leveraging brine from the Salar de Atacama.

In the US, Albemarle aims to bolster domestic production in line with the Inflation Reduction Act. It owns the Silver Peak lithium brine operations in Nevada’s Clayton Valley, set to double lithium production by 2025. Albemarle received a $90 million critical materials award from the US Department of Defense in September 2023 to enhance domestic lithium production and support the EV battery supply chain.

Additionally, the company plans to revive the Kings Mountain lithium mine in North Carolina, backed by US government funding. Albemarle also plans to develop the Albemarle Technology Park in North Carolina for advanced R&D in lithium innovation.

2. SQM: Market cap: US$12.07 billion

SQM, a chemicals giant, operates in over 20 countries, serving customers across 110 nations. The company’s diverse business areas span lithium, potassium, and specialty plant nutrition.

Primarily operating in Chile, SQM extracts brine from the Salar de Atacama and processes lithium chloride into lithium carbonate and hydroxide at its Salar del Carmen lithium plants near Antofagasta. The company is expanding production at Salar del Carmen from 180,000 MT to 210,000 MT, initiating this year.

To mitigate environmental impact, SQM announced a $1.5 billion investment in the Salar Futuro project, focusing on advanced evaporation technologies, direct lithium extraction, and a seawater desalination plant.

Despite uncertainty stemming from Chile’s National Lithium Strategy, SQM’s existing contracts, extending through 2030, are expected to be respected by the government. In early 2024, a partnership was formed between SQM and state-owned mining company CODELCO, with CODELCO holding a majority control stake.

In Australia, SQM is developing the Mount Holland lithium project, recognized as one of the world’s largest hard-rock deposits, in partnership with Wesfarmers. Anticipating lithium hydroxide production to commence by H1 2025, SQM’s lithium carbonate capacity was projected to reach 210,000 tons by the beginning of 2024.

3. Tianqi Lithium: Market cap: US$10.43 billion

Tianqi Lithium is a subsidiary of Chengdu Tianqi Industry Group based in China. As the world’s largest hard-rock lithium producer, Tianqi Lithium operates assets in Australia, Chile, and China. The company holds a notable stake in SQM, having acquired a 2.1% share in 2016, later increasing it to 23.77%.

In Australia, Tianqi owns the Greenbushes mine, acquired in 2012 through the purchase of Talison Lithium. The company also developed a lithium hydroxide plant in Western Australia’s Kwinana Industrial Area, commencing production in Q3 2019. Subsequent output began in mid-2021.

Rising lithium prices and its Hong Kong listing in 2022, which raised approximately US$1.7 billion, contributed to Tianqi’s buoyancy. Commercial production at Kwinana’s Train 1 commenced in December 2022, with Train 2 anticipated to start in 2024. Once operational, the hydroxide plant is projected to produce 48,000 MT per year, utilizing lithium from Greenbushes.

In February of the current year, Tianqi Lithium updated its total mineral reserves at Greenbushes to 447 million tonnes, with an average lithium oxide grade of 1.5%, equivalent to about 16 million tonnes of lithium carbonate.

What is In Store for Lithium?

Forecasting lithium supply beyond the end of the decade presents challenges due to limited visibility into existing, planned, and potential projects. While projections until 2030 can be reasonably accurate, the landscape becomes murkier.

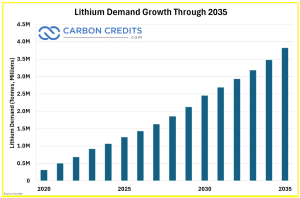

On the demand side, projections suggest that it will increase to almost 4 million tonnes, as shown below. But of course, as discussed earlier, various trends impact this demand trajectory.

Incentive pricing becomes a critical factor in determining the attractiveness of new projects. With an estimated 1.5 million tonnes of supply, the fully allocated cost of lithium would be around $15,000 per tonne, suggesting market pricing would exceed this threshold.

Navigating the Immaturity of the Lithium Market

Forecasting the future of the lithium market is hindered by its relative immaturity. Lack of globally accepted specifications and pricing anchors complicates pricing dynamics.

Lithium products, akin to specialty chemicals, require precise specifications, yet the industry’s growth trajectory impedes standardization efforts. While greater standardization is anticipated in the future, it will evolve gradually.

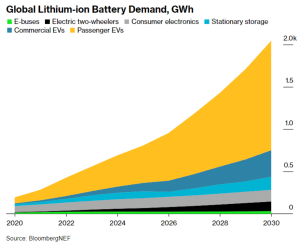

According to Bloomberg estimates, demand for lithium-ion batteries will increase tenfold over the next decade. This surge in demand is largely driven by the global commitment of over 100 countries to achieve net zero emissions within the coming decades.

As part of this commitment, many nations are turning to the electrification of transportation as a crucial solution to reduce GHG emissions and combat climate change. This shift towards electrification underscores the growing importance of lithium-ion batteries in powering EVs and other clean energy technologies.

The Role of Partnerships in Shaping the Lithium Industry

In 2022, a significant portion of the lithium supply was dominated by a handful of companies. However, future industry dynamics are expected to witness a decline in their market share, as smaller firms expand and new ventures emerge.

While horizontal integration may not be a prevailing trend, vertical integration is poised to play a pivotal role. Partnerships between miners and refiners offer mutual benefits, enabling risk-sharing and capital investment in new projects.

Collaborative efforts between upstream and downstream operations enhance expertise, improve margins, and capture a larger market share. Such partnerships, exemplified by ventures like Pilbara Minerals and POSCO in South Korea and SQM and Wesfarmers in Western Australia, are anticipated to become increasingly common in the industry’s future landscape.

Conclusion

The evolution of lithium, from its discovery over two centuries ago to its pivotal role in powering modern technology, underscores its significance in shaping our present and future. As the world accelerates towards a sustainable energy paradigm, lithium emerges as the linchpin of this transition, fueling advancements in battery technology and driving the proliferation of electric vehicles and renewable energy storage solutions.