Disseminated on behalf of Li-FT Power Ltd.

Lithium producers are facing challenges due to the low prices of lithium, prompting them to take measures to cut costs and protect profits. The drop in lithium prices has been significant, driven by increased supply and a slowdown in electric vehicle (EV) sales.

In response to these market conditions, lithium producers are reducing production, scaling back expansion plans, and focusing on cost-saving initiatives. The world’s biggest provider of lithium for EV batteries, Albemarle, announced additional cost-saving measures, reducing capex by delaying planned lithium investments.

Albemarle’s Cost-Cutting Measures

Albemarle outlined plans to cut capital expenditures for 2024 by $300 million to $500 million compared to 2023.

Moreover, the company aims to slash costs by about $100 million, with over $50 million targeted for the current year. They’ll be implementing measures such as reducing headcount and decreasing spending on contracted services.

The leading lithium producer’s Q4 2023 financial report showed a significant decline in adjusted EBITDA. It has a net loss of $315 million, representing a 125.3% decrease year-over-year. Net sales totalled $2.36 billion, down 10.1% compared to the previous year.

Looking ahead to 2024, Albemarle has identified strategic investments and projects for slow down in response to current market dynamics.

Albemarle’s Chairman and CEO Jerry Masters noted that new greenfield projects, particularly in the West, are not economically feasible at current lithium lithium prices.

Construction and engineering work at the Richburg, SC, MegaFlex conversion facility has been halted until prices improve. But permitting activities will continue at the company’s Kings Mountain site in North Carolina.

In terms of future initiatives, Albemarle will prioritize large, high-return projects that are nearing completion or in startup stages. Meanwhile, they’ll be limiting mergers and acquisitions activity.

Projects that will continue development include the commissioning of the Maison lithium conversion facility and the expansion of the Kemerton lithium conversion facility in Western Australia.

The Rise and Fall of Lithium: From EV Boom to Market Downturn

During 2020 and 2021, the electric vehicle (EV) market experienced significant growth, leading to a surge in demand for lithium, a key component in EV batteries. EV sales saw remarkable increases, with a 45.9% jump in 2020 and a further 100% increase in 2021. This led to a total of EVs sold at 9.78 million units.

This surge in demand created a deficit in lithium supplies in 2021, quickly turning into a surplus of 40,000 metric tons of lithium carbonate equivalent by 2022. Despite the surplus, market expectations continued to drive lithium prices upwards.

However, the boom in the lithium market was short-lived as the global economy weakened and EV sales slowed down, particularly in Mainland China, due to the repeal of EV subsidies. This led to a significant downturn in the lithium market in 2023.

-

As more lithium production capacity comes online, the surplus of lithium is expected to widen further, reaching 100,000 Mt of LCE in 2024.

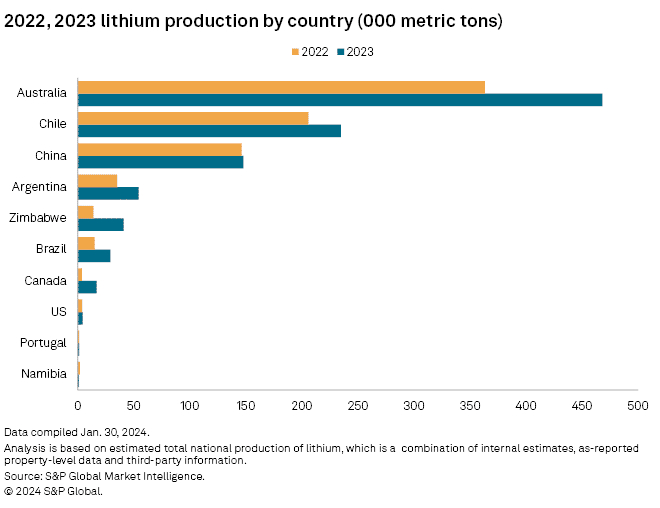

Australia remains the largest producer of lithium, followed by Chile and China. The U.S. lagged far behind, at the 8th spot after Canada.

Production of lithium is forecasted to increase by 35.7% in 2024 compared to the previous year. Analysts anticipate that lithium prices will stabilize and reach a cyclical bottom in 2024 as inventory build ups are relieved.

The current market conditions are particularly challenging for lower-grade spodumene concentrate and lepidolite producers. These producers are feeling the brunt of the downturn, as they are more susceptible to price changes and are typically the first to reduce output when prices drop too low.

For instance, Pilbara Minerals, an Australian spodumene producer, announced that it’s unlikely to pay an interim dividend for the first half of fiscal year 2024 to preserve its balance sheet.

Similarly, some spodumene producers have been considering changes to pricing settlement terms to prevent buyers from relying on inventories. For example, IGO Ltd. modified the offtake pricing model for spodumene from the Greenbushes deposit, the world’s largest lithium spodumene deposit. The company also announced a reduction in production for the second half of 2024.

Core Lithium Ltd., another Australian producer, halted mining operations at the Grants open pit to slow output and alleviate oversupply. Analysts anticipate that Australian lithium miners will continue to curtail supply in the near term due to uncertain prices.

What Lithium Producers and Investors Can Expect

As some lithium miners reduce production, investors in lithium projects are grappling with whether to proceed or postpone project development. Analysts anticipate that projects may face delays, with a particular impact on unfunded greenfield projects. They also foresee more higher-cost and pure-play lithium producers exiting the market or postponing their projects due to the current challenging conditions.

With lithium projects facing financial challenges, analysts also expect an increase in merger and acquisition (M&A) activity. Major producers with positive cash flow may seek deals in the market, while junior companies may attempt to sell projects, especially given the scarcity of private capital compared to previous years. But this isn’t the case with Li-FT Power (LIFT; LIFFF), the fastest developing North American lithium junior.

Li-FT Power‘s strategy centers on consolidating and advancing hard rock lithium pegmatite projects in Canada, focusing on established lithium districts. The company is well-financed to advance its projects, underscoring its dedication to exploring and developing top-tier lithium assets in Canada.

The tumultuous journey of lithium producers reflects the cyclical nature of commodity markets, where booms are often followed by busts. As Albemarle and other key players in the industry adapt to the challenges posed by plummeting lithium prices, their resilience and strategic responses will shape the future landscape of the lithium market.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: LIFFF.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.