The global demand for lithium metal batteries is surging, yet production falls short of meeting the need, hindering industry growth. According to Benchmark’s Solid-State and Lithium Metal Forecast, the sector faces challenges in sourcing adequate lithium metal for battery production, despite its high capacity potential.

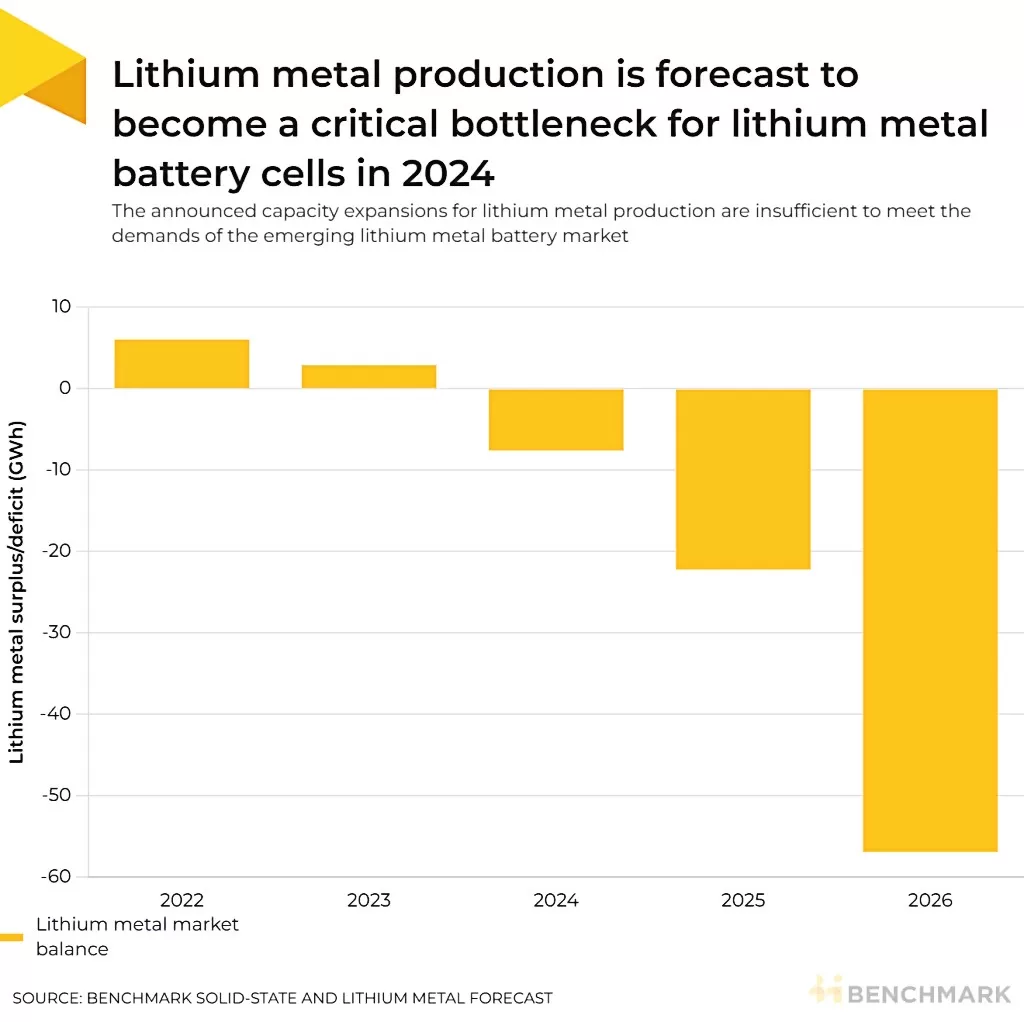

In 2024, if all suitable lithium metal produced were used for batteries, it could support 5 to 10 gigawatt-hours (GWh) of cell production. However, much of the lithium metal is diverted to other industries, leading to a supply deficit this year. From almost 10 GWh in deficit in 2024, jumping to around 60 GWh by 2026.

Chinese Dominance and Global Ambitions

China dominates global lithium metal production, accounting for over 90% of capacity in 2023. This dominance is poised to continue, with China aiming to double its capacity within the next 3 to 5 years.

Currently, some companies worldwide are scaling back output and spending due to improved supply prospects and slowing demand from EVs. Yet, Chinese firms are taking a different approach.

China’s leading lithium companies, Tianqi Lithium Corp. and Ganfeng Lithium Group Co., are undeterred by recent profit declines and aim to expand their market presence. Despite sharp drops in net income in 2023 due to plummeting prices, both companies are focused on acquiring global lithium reserves and increasing production capacity. They believe in the long-term potential of rising demand for lithium, looking beyond current challenges.

Tianqi seeks partners to explore high-quality lithium sources, accelerating work at its Yajiang mining project in Sichuan province. Meanwhile, Ganfeng plans to develop low-cost resources like lithium derived from brine and expand processing facilities in China and Argentina.

These companies’ optimism aligns with other Chinese miners like CMOC Group Ltd. and Zijin Mining Group Co. They are also eyeing opportunities in battery materials amid signs of a potential price recovery.

However, this total capacity may not meet the requirements of next-generation battery technologies.

Growing Demand Amid Technical Hurdles

The deficit arises as demand for lithium metal batteries grows rapidly, exceeding 10 GWh by 2026. Developers are transitioning from cell development to pilot production, driving up demand for lithium metal.

The precursor to lithium metal, lithium chloride, is sourced directly from brine or converted from lithium carbonate. However, most brine resources have unsuitable impurity profiles, and converting lithium carbonate incurs significant capital expense.

Next-generation lithium metal batteries require thinner lithium metal foils for the anode, challenging traditional production processes. Overcoming this technical barrier is crucial for industry growth, with companies exploring novel approaches to address this challenge.

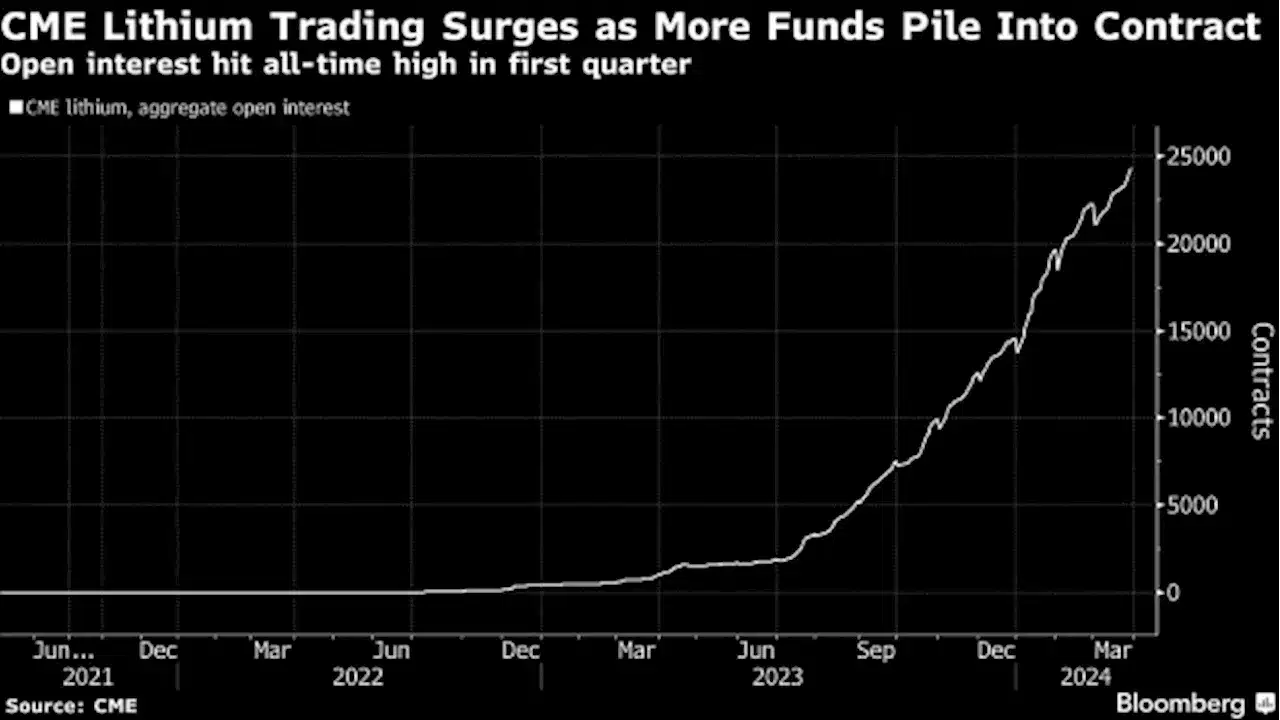

Nevertheless, trading of the metal in CME Group Inc. is experiencing a significant surge, drawing increased attention from funds amid declining battery metal prices.

The contract has seen open interest reach a record high of 24,328 contracts in the first quarter, extending to September 2025. This uptick in open interest indicates a notable increase in liquidity within the contract. This further suggests a maturing market for the lithium industry.

Trading Surge Reveals Market Resilience

The growth in open interest follows a robust year in 2023, primarily driven by arbitrage trading between China and the US. Notably, China introduced its lithium carbonate contract on the Guangzhou Futures Exchange in July last year. In turn, this further contributes to the trading activity.

This development underscores the growing importance of lithium derivatives markets as key tools for industry participants to manage price risks.

The rise in liquidity in CME’s lithium hydroxide contract is a positive sign for an industry grappling with challenges. Prices of lithium have declined by over 80% from their record high in November 2022. This drastic drop in prices has been attributed to shifting market dynamics, swaying between fears of shortages and the emergence of surplus inventories.

Despite the challenges facing the industry, the surge in open interest offers assurance to funds and financial participants. It provides them with the confidence that they can easily trade the contract, enabling them to enter and exit positions as needed, even in the face of adverse price movements.

Additionally, more Asia-based funds are showing interest in trading the CME contract this year, reflecting the growing appeal of lithium as an investment opportunity.

Moreover, the current market conditions, with lithium prices in contango (futures prices higher than spot prices), present lucrative opportunities for funds.

The contango structure allows traders to profit by buying futures contracts and selling them at a higher price in the future. This has attracted the attention of funds looking to diversify their portfolios and capitalize on the volatility in commodity markets.

The increasing liquidity and trading activity in CME’s lithium hydroxide futures contract signal a growing interest in lithium derivatives. With trading volume on pace to surpass last year’s record, lithium futures are attracting the attention of investors seeking exposure to the rapidly evolving battery materials sector.