Corporate buyers continue to rely on traditional carbon credit purchasing methods. Meanwhile, potential buyers of carbon removal credits need more education before committing to these newer options. This year’s NASDAQ survey revealed that even though companies are interested in CDR credits, a major proportion is unaware of the latest technologies like enhanced rock and coastal weathering, enhanced coastal weathering, ocean alkalinity enhancement, etc.

The survey revealed:

- Support for maximizing the impact of carbon credit purchases increased from 25% in 2023 to 27% in 2024.

- Support for offsetting emissions with carbon removal credits decreased from 24% in 2023 to 22% in 2024.

CDR: A Vital Tool for Achieving Net Zero

Carbon dioxide removal (CDR) is crucial for companies striving for net zero. Since Nasdaq’s first Global Net Zero Pulse survey, the voluntary carbon market (VCM) has evolved with new corporate feedback, updated SBTi guidelines, and U.S. government advice. The VCM allows companies to voluntarily buy credits that fund projects reducing emissions.

It is a well-known fact that limiting global warming to 1.5°C still requires removing massive amounts of CO2. Another proof is the palpable rising heat that emphasizes the urgency.

However, with growing concerns about greenwashing, companies are being more careful. This creates an opportunity to explore new CDR credit options with better risk protection. Companies must also closely examine their buying preferences for both traditional and new carbon removal efforts.

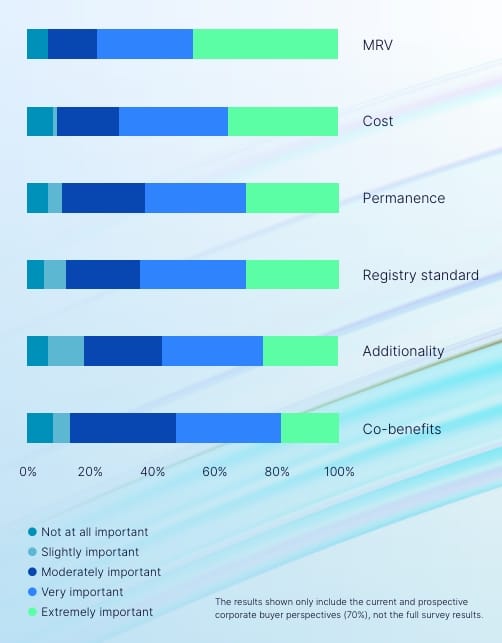

Companies need to evaluate the importance of the following criteria before buying carbon removal credits.

From June to July 2024, Nasdaq ESG Advisory conducted a survey focused on corporate buyers to explore market demand. The survey covered three key themes to help scale the VCM and drive CDR adoption.

1. Corporate Net Zero Alignment

Companies are increasingly adopting alternative strategies to reduce their emissions, but some emissions remain beyond their control. This is where they need carbon dioxide removal (CDR).

- Currently, 40% of corporate buyers understand their company’s path to reducing emissions between 2024 and 2030. They also give importance to CDR.

- About 30% expect to cut emissions by up to 40% without using CDR credits, while 31% plan to reduce emissions by up to 60% by 2030 before turning to CDR.

By 2050, the number of companies aiming for 80% or greater will become 3X. This indicates that CDR credits play a vital role in these efforts, with 87% of corporate buyers recognizing their importance in their net-zero strategies.

Moreover, B2C companies are more involved and use CDR as a key part of their strategy. This also shows the growing consumer demand for sustainable tools.

2. Carbon Credits Purchase Strategies

More companies, including those that haven’t been active in carbon markets before, are now planning to buy carbon credits. In the past, some companies have purchased carbon credits to offset emissions, but now even more are showing interest. This highlights rise in corporate demand for carbon credits.

Survey findings reveal a growing trend toward purchasing carbon reduction, avoidance, and removal credits. The energy and materials sectors, especially industries like cement, steel, and chemicals, are leading this shift. These sectors are hard-to-able and face considerable challenges to reducing their emissions. Thus, making carbon removal credits a key part of their mitigation strategy.

Additionally, corporate sectors are now aligning their carbon credit buying plans with their overall sustainability goals with a robust strategy in place. Another interesting factor is- corporate buyers tend to prefer locally sourced carbon credits. The report showed that this trend is especially strong in Canada and Asia-Pacific, where about two-thirds of respondents prefer to purchase local credits.

NASDAQ revealed,

- While in 2024, less than 10% of respondents expect to abate 80% or more of their emissions with CDR, this increases by 1.5x in 2030 and 2x in 2050.

This upward trend is particularly noticeable among sectors like information technology, financial services, consumer staples, and utilities.

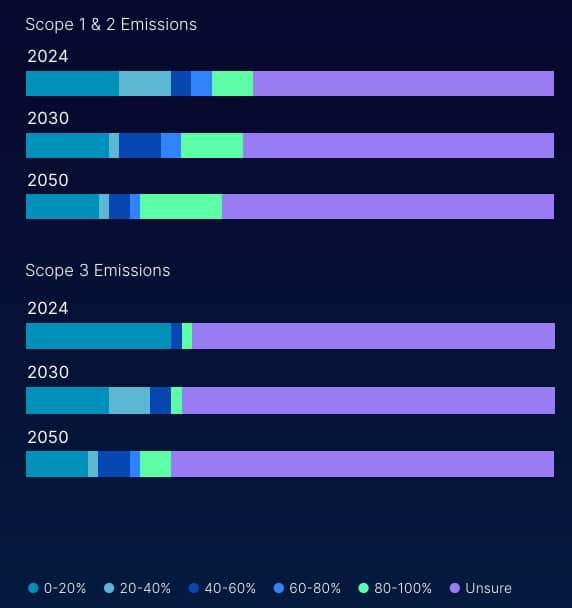

Understanding the Scope of Emissions

Many companies are uncertain about how carbon dioxide removal will fit into their plans for reducing current emissions and in the future. A significant number of respondents in recent surveys expressed doubts about their understanding of how much of their Scope 1 and 2 emissions can be reduced through CDR.

This is the reason why they hesitate to use carbon dioxide removal (CDR) until they have significantly cut their emissions. Companies not including CDR in their strategy often focus on cutting emissions first.

Another complex scenario is reducing Scope 3 emissions, which encompass the largest portion of a company’s total emissions but are often the hardest to tackle. Consequently, companies having solid knowledge of this platform are using CDR to address these challenging Scope 3 emissions.

However, even though companies are facing uncertainties in their emissions profiles, CDR will be crucial to meet their sustainability goals.

The following figure indicates the expected percentage of a company’s emissions to be abated using high-quality carbon removal credits.

3. Carbon Market Dynamics

The report has thrown light on how companies’ decarbonization and carbon credit strategies are influenced by changing policies and regulations. While carbon removals were mostly unregulated, rising concerns from stakeholders have caught the attention of regulators. As a result, the voluntary carbon markets are now under more scrutiny.

Since last year’s survey, several major policies were introduced by the SEC, California Air Resources Board (CARB), Federal Trade Commission (FTC), and European Commission (EC). These climate-related policies are putting pressure on both public and private companies.

In fact, 72% of respondents reported feeling the impact, especially from the SEC’s Climate Disclosure Rules and California’s AB-1305.

Interestingly, a deeper look reveals regional differences. Canadian respondents said these policies directly affect their carbon credit strategies. On the contrary, fewer U.S. (72%) and European (60%) respondents felt the same impact. U.S. and Canadian companies are primarily focused on the SEC’s Climate Disclosure Rules and California’s AB-1305.

In Europe, 33% of companies are more focused on EU regulations, which ban greenwashing and require companies to verify environmental claims before promoting them.

Clearer regulatory standards will increase transparency for U.S. and EU companies regarding their decarbonization and carbon credit plans. Without these guidelines, companies may hesitate to use carbon removals to offset residual emissions due to concerns over potential anti-greenwashing lawsuits.

Growing Interest in Carbon Credits Education

Corporate buyers are showing increased interest in learning more about carbon removals. The recent survey of NASDAQ revealed that 80% of respondents want more education on the topic. Many companies are turning to external experts to help them make informed decisions about carbon credit purchases.

Carbon credit registries like Puro.earth set standardized protocols and track credits to ensure market credibility. For 62% of corporate buyers, these registries and standards play a key role in their purchasing decisions.

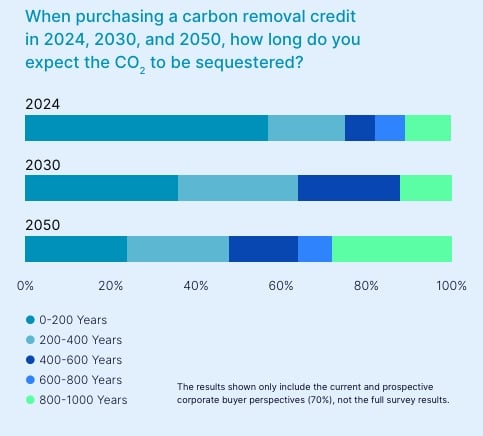

Subsequently, this is becoming important as they navigate the complexities of different carbon removal methods, such as terrestrial, technological, and ocean-based options. Additionally, corporate buyers are increasingly expecting carbon credits to offer long-term CO2 storage. This shows a clear shift towards prioritizing permanent solutions for carbon removal.

From CDR to carbon credits to carbon offsets, understanding all these factors is critical for building effective decarbonization strategies for the corporate sector. And NASDAQ’s report is a perfect guide to that.

From CDR to carbon credits to carbon offsets, understanding all these factors is critical for building effective decarbonization strategies for the corporate sector. And NASDAQ’s report is a perfect guide to that.

Source: Data and Visuals collected from 2024 NASDAQ Global Net Zero Pulse.