In recent developments within the global nickel market, the trajectory of prices has undergone a significant downturn, reflecting a complex interplay of economic factors and strategic decisions.

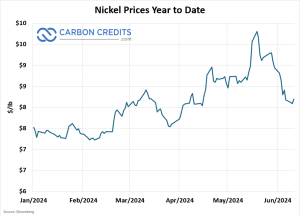

The London Metal Exchange (LME) three-month closing nickel price experienced a notable decline from $19,830 per metric ton at the end of May to $17,891 per ton by June 10. This movement marks a pivotal shift, as it is the first time since mid-April that nickel prices have dipped below the $18,000 per ton threshold.

Nickel Price Movement and Market Influences

The retreat in nickel prices can be largely attributed to decisive actions taken by investment funds. These investors opted to liquidate their long positions amid a backdrop of strengthening US dollar and less-than-stellar manufacturing data emerging from China. These factors collectively exerted downward pressure on nickel prices, overturning earlier gains made in May when prices surged to a nine-month high of $21,615 per ton.

During that period, concerns over potential supply disruptions and increased investor optimism in the base metals sector had fueled a bullish trend. However, as economic indicators shifted, investors reevaluated their positions, leading to a swift reversal in nickel prices.

This price drop occurred despite bullish headlines, including the following major market events:

- European Central Bank’s interest rate cut,

- Ongoing production standstill in New Caledonia, and

- Potential permit terminations for ferronickel and nickel pig iron plants in Indonesia.

The sharp price decline reflected a contraction in investment funds’ net long positions on the LME. This indicates a substantial liquidation of long positions.

Nickel Supply Chains in Focus

Beyond these market dynamics, the strategic maneuvers of key global players have also influenced nickel’s price trajectory.

Notably, the United States has expressed a strategic interest in forging a partnership with the Philippines, the world’s second-largest nickel producer, to secure nickel supplies essential for its burgeoning battery sector. This strategic move comes at a time when the US is grappling with the reality of its limited domestic nickel reserves compared to major producers like Indonesia.

The Philippines exported 39.9 million metric tons of nickel ore to China, underscoring its importance in the global supply chain. The US anticipates a substantial increase in nickel demand for EV batteries. It has an expected growth of 211,000 metric tons between 2023 and 2028. This demand surge underscores the need for a reliable nickel supply chain.

Furthermore, Indonesia’s significant processing capacity falls under the US government’s “foreign entities of concern” (FEOC) guidance, making Indonesian nickel potentially ineligible for certain US EV tax credits. This has led the US to enter trilateral talks with the Philippines and Japan.

Discussions are underway to enhance infrastructure and production capabilities in the Philippines. This market development signals a potential shift in global nickel trade dynamics as the US seeks to fortify its supply chains for EV production.

Short-Term Slump, Long-Term Promise: Nickel’s Dual Outlook

Looking forward, analysts predict that the global primary nickel market will continue to face challenges driven by oversupply conditions throughout the remainder of the year. Despite bullish sentiments, the underlying imbalance between supply and demand is expected to restrain nickel prices.

Short-Term Price Outlook:

The sharp price drop observed in June aligns with analysts’ earlier expectations of a potential correction. Despite a strong buying surge in May, investor confidence in nickel remains vulnerable due to the fundamental oversupply in the market.

Analysts anticipate that weak global primary nickel market fundamentals will continue to exert downward pressure on prices. Specifically, they forecast that total primary nickel stocks, measured in terms of weeks of consumption, will reach a 4-year high in 2024. This anticipated increase in stocks will likely limit any significant price recovery for the remainder of the year.

Long-Term Considerations:

While short-term price movements are driven by speculative activities and immediate market conditions, the long-term outlook for nickel remains positive, primarily due to its critical role in the energy transition.

Increasing demand from the electric vehicle (EV) sector, renewable energy technologies, and energy storage solutions will drive long-term demand growth for nickel. However, for the rest of 2024, the oversupply and high stock levels will cap price gains.

Key Nickel Insights to Digest:

- Supply Dynamics. Global nickel production is expected to continue growing, driven by expansions in major producing countries and increased output from new projects. However, the pace of growth may vary depending on geopolitical developments, regulatory changes, and technological advancements in nickel extraction and processing.

- Demand Trends. Demand for nickel is projected to rise, particularly from the EV and energy storage sectors. Nickel’s role as a critical component in lithium-ion batteries positions it as a key beneficiary of the global shift towards electrification and renewable energy.

- Price Projections. While prices may remain subdued in the short term due to oversupply, the medium to long-term outlook suggests potential price recovery as demand catches up with supply. Market participants will closely monitor factors such as technological advancements in battery chemistry, policy support for clean energy, and macroeconomic conditions.

Nickel prices have recently declined due to market recalibrations and strategic decisions by key global players. Stakeholders should brace for continued market volatility with limited immediate price recovery.