As the global demand for cleaner technologies rises, nickel’s role becomes increasingly vital. However, the market remains volatile, influenced by geopolitical strategies, supply chain dynamics, and fluctuating prices. Understanding these forces is key to navigating nickel’s future in a rapidly changing energy landscape.

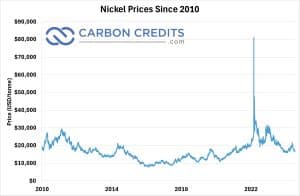

In August 2024, the London Metal Exchange (LME) three-month nickel price surged to a six-week high. This rise was primarily driven by short covering from speculators who responded to better-than-expected U.S. economic data.

Short Covering Sparks Price Surge: A Temporary High?

The improved economic outlook eased fears of an impending U.S. recession, thereby encouraging investors to close their short positions in nickel. Despite this temporary boost, the price retreated due to an increase in LME nickel stocks.

LME nickel inventories saw a significant increase, climbing from 109,950 metric tons in July to 116,616 metric tons by August. This increase reflects a substantial rise in available stock, contributing to the subsequent price decline.

In July, the LME recorded its largest monthly increase in open tonnage for the year, with a 12,942 metric ton rise. This boost was attributed to higher refined class 1 nickel inflows from China.

This increase in Chinese stock was notably due to refined nickel from Indonesia entering the LME system for the first time, following the approval of Indonesia’s first nickel brand, DX-zwdx, by the LME in May 2024.

China’s Nickel Influx and Indonesia’s Strategic Moves

Indonesia, a major player in the nickel market, is actively working to reduce Chinese ownership in new nickel projects. The Asian country’s goal is to qualify for tax credits under the U.S. Inflation Reduction Act of 2022.

The Act offers a $7,500 tax credit for electric vehicles, but companies with at least 25% ownership by a “covered nation,” including China, are ineligible. This regulation has prompted Indonesia to seek new investment structures, with China-based companies potentially being limited to minority stakes.

The Indonesian government’s efforts also reflect its broader strategy to diversify its investments and appeal to other foreign investors. However, significant barriers remain. Reports indicate that major European companies, such as BASF and Eramet, have decided against investing in Indonesian nickel projects due to concerns over environmental, social, and governance (ESG) issues.

Additionally, Indonesia’s recent policy shifts, including a proposed moratorium on new nickel pig iron plants, could further deter non-Chinese investment.

The rapid growth of Indonesia’s nickel industry has caused an oversupply in the market, leading to a significant decline in prices from the peaks seen in 2022 and 2023. This surplus has put downward pressure on nickel prices as supply outstrips demand, affecting the broader market dynamics.

Why 2024’s Nickel Prices May Stay Low Despite the Hype

Looking ahead, despite potential short-term gains from a possible U.S. interest rate cut in September, the nickel market’s overall outlook remains subdued. The prevailing weak fundamentals in the global primary nickel market suggest that current price gains may not be sustainable.

Experts predict a decline from the 2023 average price, reflecting ongoing challenges in the market.

In terms of investment trends and market projections, China’s dominance in Indonesia’s nickel sector is expected to continue. The continuing influence of Chinese investments underscores the strategic importance of Indonesia in the global nickel supply chain.

The nickel market is currently experiencing a short-term slump due to oversupply, with prices expected to remain low throughout 2024. Analysts further predict that primary nickel stocks will reach a four-year high, limiting any significant price recovery this year.

However, the long-term outlook is more positive, driven by growing demand from the electric vehicle and renewable energy sectors. Despite the current challenges, nickel’s critical role in the energy transition suggests that demand and prices will strengthen in the future.