Nickel has moved from being a niche industrial metal to a critical pillar of the global energy transition, along with copper, lithium, and uranium.

Once primarily used in stainless steel, nickel is now critical for high-energy-density batteries, electric vehicles (EVs), grid storage, aerospace alloys, and emerging hydrogen infrastructure.

Essentially, it’s now another mineral on that list, albeit one that seems to have largely flown under most investors’ radars thus far. However, it’s understandable why that’s been the case – after all, the primary use for mined nickel has long been industrial, with over three-quarters of global nickel demand being for things like alloy production or electroplating.

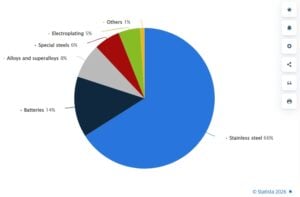

Distribution of primary nickel consumption worldwide in 2024, by industry

Nickel Basics: Types, Grades, and Industrial Uses

Nickel is a silvery-white transition metal with high corrosion resistance, ductility, and thermal stability. Its unique properties make it indispensable in alloys and electrochemical applications.

Nickel is generally classified into two main categories:

- Class 1 nickel: High-purity nickel metal, powders, briquettes, and salts such as nickel sulfate. These are essential for battery cathodes, advanced alloys, and aerospace applications.

- Class 2 nickel: Ferronickel and nickel pig iron (NPI), primarily used in stainless steel production.

Historically, stainless steel accounted for roughly two-thirds of nickel consumption, providing a stable demand base. However, batteries have emerged as the fastest-growing segment, particularly for nickel-rich cathode chemistries such as NMC (nickel-manganese-cobalt) and NCA (nickel-cobalt-aluminum).

Aerospace, defense, and superalloys also rely heavily on nickel for high-temperature and corrosion-resistant applications.

This dual-market nature—spanning bulk industrial use and high-tech energy transition applications—makes nickel one of the most structurally complex metals in the critical minerals ecosystem.

Nickel Processing Technologies: The Backbone of the EV and Steel Boom

Not all nickel is equal, and processing technology determines where it ends up. Nickel processing is the set of industrial methods used to extract nickel from its ores and turn it into usable forms for various industries, including stainless steel, batteries, and alloys. Essentially, it’s how raw nickel in rocks becomes the high-purity metal or chemical compounds needed for manufacturing.

Nickel is mined mainly from two types of ores:

- Sulfide ores – Found deep underground, easier to process, high purity.

- Laterite ores – Found near the surface, lower nickel content, more challenging to process.

The Case Of Battery Grade Nickel

In order to be used in an electric vehicle, nickel must first be refined to extremely high purities, creating what’s known as “battery grade” nickel. Following this, it then needs to be dissolved in sulphuric acid to create nickel sulphate, which can then be used to produce battery cathodes.

Nickel’s high energy density, which allows it to hold more charge for less weight, makes high-nickel battery chemistries more desirable in EV batteries. While the first iterations of the lithium-ion battery used equal proportions of nickel, manganese, and cobalt, modern ones use as much nickel as manganese and cobalt combined.

And as technology continues to progress, it’s expected that the ratio will rise to as much as 80% nickel, or even more.

Now here’s a simple breakdown of the processing technologies:

Pyrometallurgy Still Dominates Stainless Steel

High-temperature smelting remains the most common route for nickel extraction. Rotary kiln–electric furnace (RKEF) and flash smelting convert sulfide and laterite ores into ferronickel or nickel pig iron (NPI). These products suit stainless steel, but they consume large amounts of energy and emit significant CO₂.

Notably, NPI and ferronickel continue to anchor global supply.

Hydrometallurgy Powers Battery-Grade Nickel

Hydrometallurgical routes, especially high-pressure acid leaching (HPAL), are becoming critical for EV batteries. HPAL converts laterite ores into mixed hydroxide precipitate (MHP) and then into nickel sulfate for cathodes.

Refining and Recycling Gain Momentum

Electrorefining and solvent extraction deliver high-purity Class 1 nickel. Refined products made up around 60% of the nickel market in 2024. Recycling is also rising as a low-carbon supply source.

In short, nickel processing is splitting into two markets: low-cost NPI for steel and high-purity nickel for batteries. This divide is reshaping supply chains, investment flows, and decarbonization strategies across the metals industry.

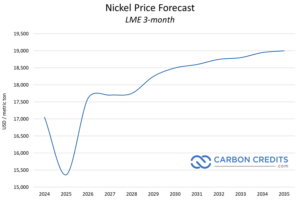

The Volatile Nickel Price Cycle

Unlike lithium, the nickel market is much more complex. The metal sits at the crossroads of geopolitics, industrial demand, and changing battery technology. Over the past five years, nickel prices have been highly volatile.

For example, during the 2022 LME squeeze, prices spiked above $100,000 per tonne. Then they dropped sharply to around $13,900 per tonne in early 2025.

- Since then, they have started to recover, reaching about $17,200 per tonne by February 2026.

This volatility shows how sensitive nickel is to supply, demand, and global events. As EV demand grows, the nickel market will continue to face swings.

This volatility reflects a structural mismatch between supply expansion and shifting demand patterns. Massive Indonesian production growth has flooded the market, while battery chemistry trends toward lithium iron phosphate (LFP) have reduced nickel intensity in mass-market EVs. At the same time, premium EVs and aerospace applications continue to rely heavily on Class 1 nickel, creating a bifurcated market structure.

For investors, policymakers, and corporates, nickel represents a critical test case for the energy transition economy. Understanding its supply chain, macro drivers, and long-term price scenarios is essential for navigating the next decade of critical minerals markets.

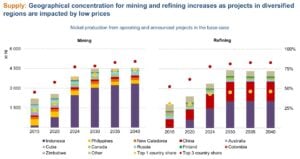

Global Nickel Supply: Indonesia’s Dominance and Market Impact

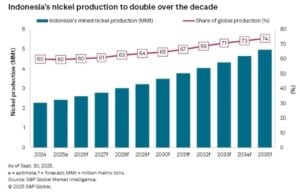

Indonesia has reshaped the global nickel market more than any other country. In 2024, its nickel in mine production was 2.2 million tonnes (mt), an increase of 158% over the previous five years. Its rise was fueled by a combination of raw-ore export bans, massive Chinese-backed investments in downstream processing, and the rapid deployment of high-pressure acid leach (HPAL) facilities for battery-grade nickel.

By consolidating both mining and smelting, Indonesia has established a vertically integrated nickel ecosystem capable of supplying both stainless steel and battery markets at low cost.

Policy Controls and Quota Management

Despite its dominance, Indonesia’s nickel supply faces tightening government controls in 2026. The government sharply reduced the nickel ore production quota (RKAB) to 250–260 million wet metric tonnes (wmt), down from 379 million wmt in 2025 and 298 million wmt initially approved for 2025—a cut of roughly 34%.

The move aims to align ore output with domestic smelter capacity, curb oversupply, and support prices. Following the announcement, LME nickel prices surged past $18,000/t before stabilizing near $17,200/t in February 2026.

Delays in RKAB approvals have already halted operations at mines such as PT Vale Indonesia, signaling enforcement risks for the policy. Meanwhile, demand growth is tempered by slower stainless steel uptake and the structural shift toward LFP batteries, which has helped sustain a global surplus forecast of 261–288 kt in 2026 despite production cuts.

Indonesia’s strategic approach—resource nationalism, controlled expansion, and downstream integration—has fundamentally altered global nickel pricing. Low production costs and government-backed industrial policy allow Indonesian producers to remain profitable even during periods of weak prices.

- However, S&P Global noted that, “Indonesia is still projected to more than double its production over the next decade to an estimated 4.97 MMt by 2035.”

China’s Role in the Nickel Supply Chain

China continues to dominate the processing of nickel intermediates and battery materials. Chinese firms have financed and built much of Indonesia’s upstream infrastructure, including HPAL plants and mixed hydroxide precipitate (MHP) facilities.

It is also the single largest consumer of nickel, driven by domestic stainless steel production and battery manufacturing. Policy shifts, stimulus measures, and industrial planning decisions in China have an outsized impact on global nickel markets, influencing both price and supply chain dynamics.

Other Global Producers

Beyond Indonesia and China, major nickel-producing countries include Russia, the Philippines, Canada, Australia, and New Caledonia. However, many high-cost producers have struggled to compete with Indonesia’s integrated, low-cost production model. For example, BHP suspended operations at its Nickel West facility in Western Australia amid persistent low prices, highlighting the competitive pressures faced by high-cost producers.

This dynamic has accelerated consolidation in the global nickel industry, with strategic repositioning focused on securing downstream processing and high-grade nickel for energy transition applications.

Nickel Demand Dynamics: Stainless Steel vs. Batteries

Stainless Steel: The Legacy Anchor

Stainless steel remains the primary driver of nickel demand, accounting for roughly two-thirds of consumption. Demand is closely tied to construction, infrastructure, and manufacturing activity. China, the world’s largest stainless steel producer, remains a key macro driver for nickel demand globally.

Class 1 Nickel: Powering the EV Boom

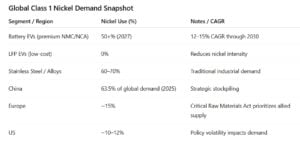

Nickel demand for batteries has grown fast over the past decade. Class 1 nickel, with purity above 99.8%, is key for high-energy NMC and NCA batteries. These batteries power premium EVs, giving longer driving ranges and lighter, more efficient vehicles. Advanced cathodes now contain 60–80% nickel, with some designs targeting 90%+ nickel content.

By 2030, nickel-heavy batteries could reach 1,320 MWh globally, covering about 80% of all EV lithium-ion batteries. Battery demand is expected to use over 50% of Class 1 nickel by 2027, growing at 12–15% per year. The average EV battery now contains 28–30 kg of nickel.

But there are risks:

-

LFP batteries, which contain no nickel, are growing in lower-cost EVs, especially in China. Nickel intensity per vehicle has fallen nearly one-third since 2020.

-

Policy differences affect supply: China held 63.5% of global nickel demand in 2025, Europe prioritizes allied supply, and US policies are less stable.

The Lights Are Green for Nickel

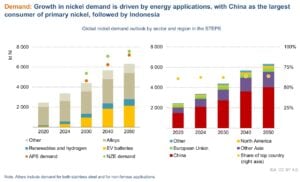

Forecasts from the International Energy Agency (IEA) project nickel demand more than doubling by 2035 under current pledges, potentially tripling in net-zero scenarios driven by EVs and storage.

IEA also projects that nickel use in EV batteries, renewables, and stainless steel is projected to push nickel demand above 5.5 Mt by 2035. As Indonesia tightens output and China dominates downstream processing, Western economies face rising exposure to supply disruptions and geopolitical leverage. Even conservative outlooks show 8-9x EV battery demand growth by 2050, despite late-decade plateaus from chemistry shifts.

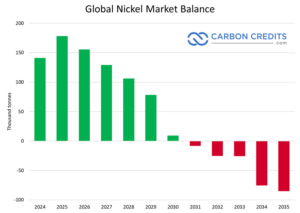

Long-Term Supply Outlook: From Oversupply to Potential Deficit

As per INSG last year, supply vastly outpaced demand, hitting 209-212 kt global surplus. Recently, S&P Global projected a 156,000-tonne surplus in 2026. However, the same analysis also says that today’s surplus will not last forever.

The report projects that global nickel stocks will peak around 2028. After that, inventories will begin to fall as demand improves and supply growth slows. By the early 2030s, the market balance will flip.

By 2031, S&P Global expects the primary nickel balance to turn negative. EV battery demand will grow as electrification expands. Stainless steel consumption will recover alongside global manufacturing. Significantly, Indonesian supply growth will slow as easy expansions may run out, and regulatory risks can increase.

Once inventories drop below comfortable weeks-of-consumption levels, prices respond quickly. S&P Global points to nickel prices rising toward $25,000 per tonne or higher, especially for Class 1 material.

Policy and Geopolitics: Resource Nationalism and Market Fragmentation

Indonesia exemplifies modern resource nationalism. The government’s export bans, production quotas, and mine suspensions aim to capture downstream value and stabilize prices.

Western governments are responding with critical minerals strategies, including subsidies, domestic mining support, and restrictions on Chinese supply chains. This could fragment the global nickel market into competing blocs, heightening geopolitical risk for downstream industries.

Most importantly, the Trump administration sees developing U.S. nickel supply chains as key to reducing dependence on foreign sources and boosting the domestic industry. Efforts include promoting new mining projects, speeding up permits for critical mineral operations, and exploring tariffs or other trade measures to support local production. One major example is a copper-nickel project in Minnesota, led by a joint venture between Glencore and Teck Resources.

Macro Drivers: Energy Transition, Industrial Demand, and Monetary Policy

Nickel is highly sensitive to macroeconomic and policy conditions. Industrial demand tracks global manufacturing cycles, while battery demand depends on EV adoption rates, subsidies, and consumer behavior.

Interest rates, inflation, and currency fluctuations affect nickel through speculative flows and production financing costs. Meanwhile, energy transition policies, carbon pricing, and ESG mandates are reshaping supply chains, pushing automakers and battery manufacturers to secure long-term nickel supply agreements.

Nickel’s Role in Carbon Markets and Net-Zero Strategies

Nickel’s importance extends beyond industrial use. Battery supply chains are central to decarbonization, embedding nickel demand in national net-zero strategies. Companies increasingly link nickel sourcing to ESG frameworks, carbon disclosure requirements, and sustainability-linked financing.

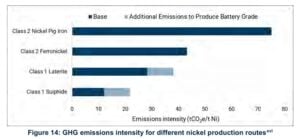

At the same time, nickel production drives greenhouse gas (GHG) emissions. According to a disclosure from the International Finance Corporation (World Bank Group), under a scenario accounting for declining ore grades and cleaner grids, emissions could rise 90% from 2020 to 2050. Additionally, a lack of decarbonization could push emissions to 164%.

Most emissions come from processing rather than mining. Pyrometallurgical routes for Class 2 nickel (used in stainless steel) are coal-intensive, while Class 1 battery-grade nickel has lower emissions. Shifting to EV-focused, Class 1 production can help limit emissions growth.

Thus, cleaner processing, low-carbon production, and recycling could give automakers and battery makers a competitive edge, while decarbonized electricity is key to controlling nickel emissions as production rises.

Top 3 Nickel Producers Signal Tight Supply Heading into 2026

The global nickel market entered 2026 with cautious signals from its largest producers. Industry analysts revealed that mining output stayed broadly flat, disruptions persisted, and companies focused more on battery-grade processing than expanding supply. This reinforced expectations of a structurally tight nickel market.

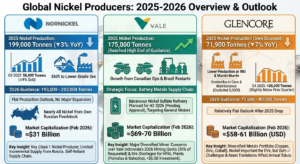

Nornickel

Norilsk Nickel, or Nornickel, reported stable but slightly lower production in 2025. The company produced 199,000 tonnes of nickel, down 3% year-on-year, mainly due to a shift toward lower-grade disseminated ore. Production recovered in the fourth quarter, rising 9% quarter-on-quarter to 58,000 tonnes after scheduled maintenance in Q3. Nearly all nickel came from the company’s own Russian feedstock, highlighting its self-reliant supply chain.

For 2026, Nornickel guided nickel output between 193,000 and 203,000 tonnes, signaling flat production with no major expansion plans. Nornickel’s market capitalization stood at about $31 billion as of February 2026, underscoring its role as a major global supplier despite geopolitical constraints.

The lack of growth from one of the world’s key Class 1 nickel producers suggests limited incremental supply from Russia.

Vale

Brazil’s Vale continued to position itself as a strategic player in the battery metals supply chain. The company plans a nickel sulfate refinery in Bécancour, Québec, with deliveries to General Motors targeted for the second half of 2026, pending regulatory approvals. This move highlighted Vale’s push toward high-purity battery materials rather than bulk nickel mining.

Vale’s market capitalization was around $69–70 billion in early 2026, making it one of the largest diversified miners with significant nickel exposure. It produced 175,000 tonnes of nickel in 2025, reaching the high end of its guidance. Growth came from Canadian operations in Sudbury and Long Harbour and restarts in Brazil.

Looking ahead, Vale Indonesia warned its 2026 mining quota won’t meet demand for new nickel smelters. The approved quota is only about 30% of what the company requested, raising concerns that upcoming processing plants could face ore shortages.

Vale and partners are building three HPAL plants for EV battery nickel. The Pomalaa plant, starting in August 2026, will need 21 million tonnes of limonite ore per year, while Bahodopi will require 10.4 million tonnes annually. These projects represent over $6.5 billion in investment and highlight the growing pressure on Indonesia’s nickel supply.

Glencore

Glencore’s 2025 Full‑Year Production Report showed nickel output from its own sources at 71,900 tonnes, down about 7% from 82,300 tonnes in 2024. This decline was driven by lower production at both Integrated Nickel Operations (INO) and the Murrin Murrin operations. The reported figure excludes 5,000 tonnes from the Koniambo project, which is in care and maintenance.

In the fourth quarter of 2025, nickel production (including third‑party feed) was around 35,300 tonnes, slightly below the prior quarter. Glencore also gave 2026 nickel guidance of 70,000–80,000 tonnes, reflecting a relatively flat outlook after the 2025 drop.

Its nickel business is part of a broader diversified metals portfolio, with the company also producing copper, zinc, cobalt, coal, and other commodities. Nickel remains important to its strategy, especially given rising EV battery demand, but output challenges and asset transitions affected annual totals.

As of February 2026, Glencore’s market capitalization is widely reported to be around $58–61 billion (USD) based on its London Stock Exchange listing and share price.

This positions Glencore as a major diversified mining and commodity trading company, though smaller in market value than some of its peers like Rio Tinto or BHP. The company’s valuation reflects its breadth across metals, energy, and marketing operations, and its prospects are often shaped by commodity price swings and operational performance.

Risks and Opportunities for Investors and Policymakers

The top nickel producers showed limited growth in mining output while accelerating investments in battery-grade processing. Ore quality challenges, regulatory delays, and operational disruptions continued to constrain supply. At the same time, electric vehicle demand and energy transition needs kept rising.

The lack of aggressive supply expansion from major producers suggests the nickel market could remain structurally tight through the late 2020s, especially for high-purity Class 1 nickel required in batteries.

This is why nickel stocks present a unique combination of risks and opportunities. Supply concentration, policy interventions, and technological disruption create price volatility. Conversely, long-term demand from electrification, aviation, and hydrogen infrastructure provides structural upside.

Investors must navigate cyclical price swings, while policymakers balance industrial policy with market stability. Strategic supply agreements, diversification, and technology adoption will be crucial for managing risk.

Conclusion: Nickel’s Strategic Decade Ahead

Nickel is entering a decisive decade. The metal is so vital for the global energy transition, but faces structural uncertainty from supply expansion and evolving battery technology.

The next ten years will determine whether nickel becomes a stable metal of clean energy supply chains or a cautionary case study in commodity oversupply and industrial policy missteps. For institutions, understanding nickel’s macro dynamics, supply chains, and policy risks is essential. The metal’s trajectory will shape not only battery markets but also the geopolitics of the global energy transition.