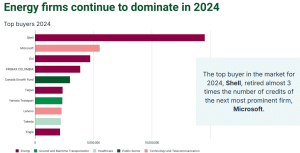

In the race to offset their carbon footprints, two giant companies—Shell and Microsoft—stand out as the largest carbon credit buyers in 2024, according to the Allied Offsets report. Their massive retirements reflect differing strategies and priorities, however, signaling distinct approaches to tackling carbon emissions through carbon markets.

Shell, the world’s largest fossil fuel company, and Microsoft, a technology leader, have been pivotal players in the voluntary carbon market (VCM). However, their activities reveal stark contrasts in how they approach sustainability goals and what projects they support.

Meanwhile, the broader carbon credit market in 2024 showed a growing emphasis on removals and diversification of project types.

Shell: The Emission Offset Leader

Shell retained a massive 14.5 million carbon credits in 2024, taking the top spot for the second consecutive year. This commitment is a significant part of Shell’s strategy to offset its extensive emissions.

Unlike Microsoft, which has heavily invested in carbon removal technologies, Shell’s purchases mainly target projects focused on emissions avoidance.

A large portion of Shell’s credits—9.4 million—came from forestry and land-use initiatives. These projects, focusing on protecting and managing forests to prevent the release of stored carbon, are cost-effective but also face scrutiny over integrity concerns. Interestingly, the energy giant announced plans in November last year to sell part of its nature-based carbon projects.

The company also retired 2.4 million renewable energy credits, a cheaper and more widely accepted option in the market.

Moreover, the price difference between Shell’s credits and Microsoft’s illustrates their contrasting strategies. While Shell paid an average of $4.15 per credit, it remains focused on more affordable projects, including renewable energy and forestry.

Despite criticisms over the quality of some of its projects, Shell continues to be a significant player, aligning its credit purchases with its ongoing goal of achieving net-zero emissions by 2050. To achieve that, the oil major aims to reduce emissions from its operations by 50% by 2030, using 2016 baselines.

Microsoft: A Carbon Removal Champion

In contrast, Microsoft has pursued a more aggressive approach toward carbon removal, setting itself apart with a robust commitment to investing in innovative carbon capture technologies. The company retired 5.5 million credits in 2024, a distant second to Shell. However, the type of credits the tech giant bought tells a different story.

A key focus for Microsoft has been on bioenergy with carbon capture and storage (BECCS). It is an expensive and emerging technology that is capable of delivering carbon-negative results. BECCS works by capturing the carbon dioxide released during the burning of biomass and storing it underground.

Nearly 80% of Microsoft’s 2024 carbon credits came from BECCS projects, with the largest purchase of 3.3 million credits coming from Sweden’s Stockholm Exergi. While this technology is still in its infancy, it plays a critical role in global pathways to achieving net-zero emissions.

Microsoft’s strategy, however, is not without its challenges. BECCS credits are costly, with average prices of $389 per credit—substantially higher than the costs associated with Shell’s projects.

- In 2024, Microsoft’s average credit price was $189, a significant investment considering its aim to neutralize emissions across its operations.

Despite the high costs, Microsoft’s commitment to carbon removal reflects its leadership in the tech industry’s broader sustainability agenda. The major tech company aims to be carbon-negative by 2030.

Microsoft’s strategy to focus on carbon removals seems to be on the right track. The broader carbon market trend reveals the growing interest in carbon removal credits.

Carbon Market Dynamics: Increasing Focus on Quality and Carbon Removal Credits

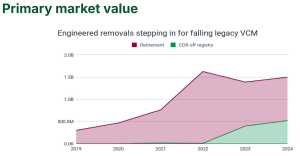

The VCM in 2024 has shown signs of shifting, with a significant uptick in carbon removal credits, per the report. However, overall retirement activity in the VCM plateaued, with 2024 marking the third consecutive year of minimal growth.

The decrease in market growth is not necessarily a negative development, as more buyers have shifted toward high-quality, impactful projects.

While Shell and Microsoft represent the extremes in carbon credit purchasing, other buyers are increasingly exploring removals and non-traditional carbon offset projects. Removals, such as those associated with BECCS, saw a larger share of the market, though they still constitute a small portion overall.

This shift reflects a broader trend toward supporting innovative carbon removal solutions, which can deliver long-term, lasting environmental benefits. Another report by the MSCI also reveals the same trend—demand for carbon removal credits is rising.

The market’s composition is also diversifying. Projects related to renewable energy and forestry still dominate. However, their share in total credit retirements has decreased from 80% in 2020 to 70% in 2024.

At the same time, new entrants into the market are pushing for more varied solutions, including technologies for direct air capture and carbon removal, which add complexity to an already challenging marketplace.

Challenges for Credit Buyers and the Market

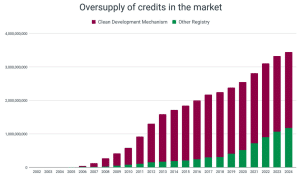

One of the major challenges for buyers is the oversupply of carbon credits in the market, which continues to grow. In 2024, the number of issued but not retired credits increased again, contributing to a potential glut in available credits.

This dynamic is particularly evident in the market for older Clean Development Mechanism (CDM) credits, which have increasingly been criticized for their lack of additionality and impact.

Despite these challenges, the number of active buyers in the VCM continues to grow. In 2024, more than 6,500 companies participated in the market, a slight increase compared to previous years.

The vast majority of carbon credit buyers continue to come from the financial and energy sectors, with Microsoft representing a key player in the tech space. Even though more companies are entering the market, the rate of growth has slowed. This suggests that carbon credits are becoming a more established component of sustainability strategies.

As we move into 2025, the divergent strategies of Shell and Microsoft may serve as a model for others seeking to engage with the VCM. Shell’s focus on affordability and scale contrasts with Microsoft’s commitment to cutting-edge carbon removal technologies.

Yet, both companies are working towards a common goal—neutralizing their emissions and supporting global climate efforts.

As the market continues to evolve, these two companies are likely to remain at the forefront of shaping how businesses approach their carbon footprint and the critical role carbon credits play in the global fight against climate change.