The U.S. solar industry has seen a rapid expansion since President Joe Biden signed the Inflation Reduction Act (IRA) in August 2022. The act has been instrumental in increasing domestic solar panel production capacity more than fivefold. This is a crucial step in Biden’s goal of building clean energy supply chains within the country.

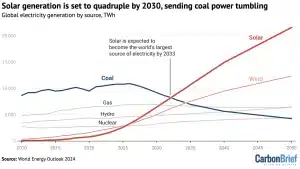

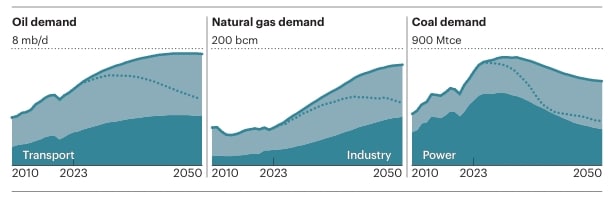

Globally, the International Energy Agency (IEA) recently published its World Energy Outlook 2024 which shows that solar power generation could increase fourfold by 2030. The report suggests that solar energy could be a leading source of electricity by 2033, surpassing nuclear, wind, hydro, and natural gas. It could eventually even overtake coal, positioning itself as the largest electricity source globally.

IRA Fuels Solar Investments but Leaves Gaps

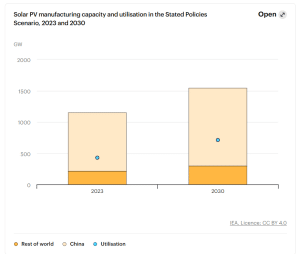

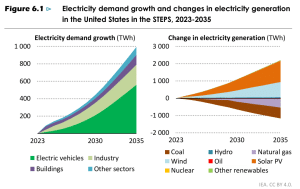

Renewable energy is set to significantly outpace electricity demand growth, per IEA data. In one scenario renewable output is expected to expand by nearly 2,200 TWh by 2035, more than tripling its 2023 level. This increase will boost renewables’ share of electricity generation from 22% to 58%, with solar PV seeing the largest growth.

Key factors of this growth include high-quality renewable resources, established markets with low technology costs, and strong federal and state policy support.

The IRA is a cornerstone of Biden’s clean energy policy. It offers up to $1.2 trillion in tax incentives over 10 years. These incentives aim to boost the production and deployment of clean energy technologies.

One of the IRA’s key elements is the advanced manufacturing tax credit, which has led to over a dozen new or expanded solar module manufacturing plants across the U.S.

- Since the IRA’s passage, solar companies have invested over $34 billion in building new factories.

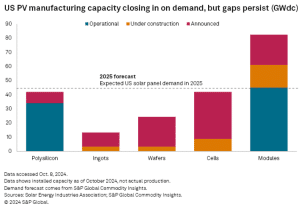

According to federal data, the U.S. now boasts over 45 gigawatts (GWdc) of solar module manufacturing capacity. At maximum production, these facilities could meet most of the U.S. solar demand expected by 2025 as reported by S&P Global Commodity Insights.

However, the solar industry’s expansion has not been uniform. The bulk of investments has gone into the assembly of modules, trackers, inverters, and other downstream components. In contrast, there’s a lack of domestic production for crystalline-silicon ingots, wafers, and cells—key components of the solar supply chain.

Navigating Market Risks and Government Support

Industry leaders see these gaps as a significant hurdle to achieving a fully self-reliant solar industry.

Ray Long, the president and CEO of the American Council on Renewable Energy, describes this surge as a “clean energy manufacturing renaissance.” Despite the positive momentum, Long emphasizes that the rapid growth of solar manufacturing in the U.S. comes with challenges.

For instance, the potential threat from cheaper Asian imports is one challenge. Some U.S. manufacturers seek more federal support to level the playing field, believing that additional measures are necessary to ensure their success.

Moreover, the outcome of the upcoming presidential election could significantly shape future policies. While both political camps support bringing manufacturing back to the U.S., their strategies differ.

Donald Trump, for example, advocates for broader tariffs on imports, which could raise costs for consumers. Kamala Harris, on the other hand, criticizes such tariffs as a “sales tax” on American buyers.

Experts believe that consistent support from the federal government is crucial to sustain the growth of domestic solar production.

Notably, the U.S. Treasury Department is working to enhance support for the solar industry. It recently clarified that solar ingot and wafer manufacturing facilities qualify for a 25% investment tax credit under the 2022 CHIPS and Science Act.

Solar Industry Moves Forward Despite Challenges

Industry leaders are divided on the future direction of U.S. solar manufacturing. Some are optimistic about the role of government support in boosting domestic production.

Steven Zhu, president of Trina Solar (U.S.) Inc., emphasized the importance of diversifying manufacturing locations, including expanding into the U.S., to manage risks from policy changes. Trina Solar is set to open a 5-GW solar module facility in Texas, with plans to expand production in 2025.

Yet, others are skeptical about the sustainability of new U.S. solar plants. T.J. Rodgers, CEO of residential solar company Complete Solar and former chairman of SunPower, argues that most of the new solar factories in the U.S. are unlikely to be profitable without continuous government subsidies. He believes the reliance on taxpayer support to maintain operations could become a long-term challenge for the industry.

These varying perspectives reveal the uncertainty surrounding the U.S. solar manufacturing industry, especially with the presidential election approaching. While both parties agree on the importance of reducing reliance on Chinese solar components, their differing approaches could significantly impact the industry’s trajectory.

Worldwide, the IEA forecast shows that solar and wind energy could transform the global power landscape, potentially contributing nearly 60% of global electricity by 2050. The agency further projects that solar power alone could see a massive expansion. It can go beyond 16,000 gigawatts (GW) by 2050, compared to today’s levels.

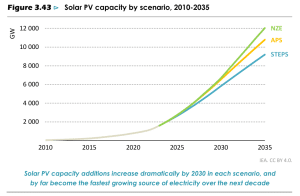

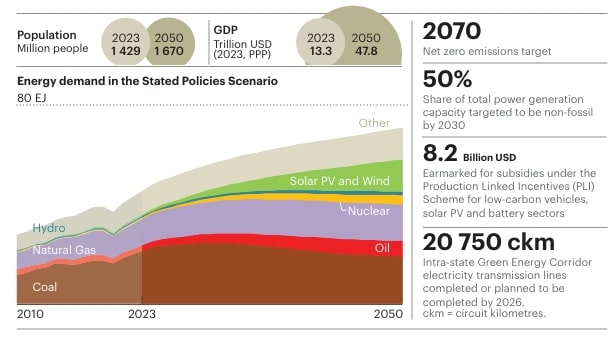

In the U.S., renewable energy sources are on track to grow much faster than the electricity demand. Under one scenario, STEPS (Stated Policies), solar power will see the most significant growth. Together with wind energy, together they could provide 50% of electricity by 2035, up from 15% in 2023.

Ultimately, the U.S. solar manufacturing sector is in a period of rapid growth, driven by strong demand for renewable energy and significant federal incentives. As solar companies push forward with ambitious expansion plans, their success will depend on continued government support and favorable market conditions.

From CDR to carbon credits to

From CDR to carbon credits to