Investors were used to looking for companies to cut only their operational emissions and indirect emissions from energy purchases. But now they’re focusing on the entire business supply chain, meaning Scope 3 emissions are becoming more significant.

This trend puts emissions from the value chain at the spotlight. But why is it important to account for this type of carbon emissions and why its disclosure is a must?

This article will explain everything you need to know about Scope 3 emissions and the importance of disclosing and accounting for them.

The Importance of Evaluating Scope 3 Emissions

Scope 3 emissions, which include indirect emissions from a company’s value chain, often represent the largest portion of corporate-related emissions. But companies often neglect to disclose these emissions or simply mention them without enough details.

The lack of transparency leaves investors in the dark when assessing the real climate risk exposure of their portfolios.

Good news for investors in the US, the EU, and New Zealand. Regulators in these countries proposed a mandatory Scope 3 emissions reporting for listed companies.

Even the central banks are feeling the weight of this matter as they’re starting to take climate exposure into consideration.

This growing awareness and increasing regulatory interest will likely lead to more Scope 3-related policies in the coming years.

Accounting for Scope 3 emissions is very flexible as they tend to be self-imposed. Yet, it’s still difficult to compare data across companies because of the varying emissions profiles even within sectors.

Unfortunately for investors, companies often omit significant Scope 3 categories without providing transparent reasons for doing so. This is why stricter rules on disclosure are coming up, prompting large companies to start accounting for value chain emissions.

Investors can use value chain emissions as an indicator of transition risk and gauge a company’s true climate ambition.

After all, assessing exposure to carbon-intensive activities in value chains and products is critical for investors. It can help them expect any potential impacts on asset values and operating costs.

So, it’s just reasonable for investors to demand more comprehensive and transparent Scope 3 disclosures and scrutinize them more closely. Doing so will help them better understand overall climate risk and identify potential greenwashing.

Scope 3 Emissions and the Greenhouse Gas Protocol

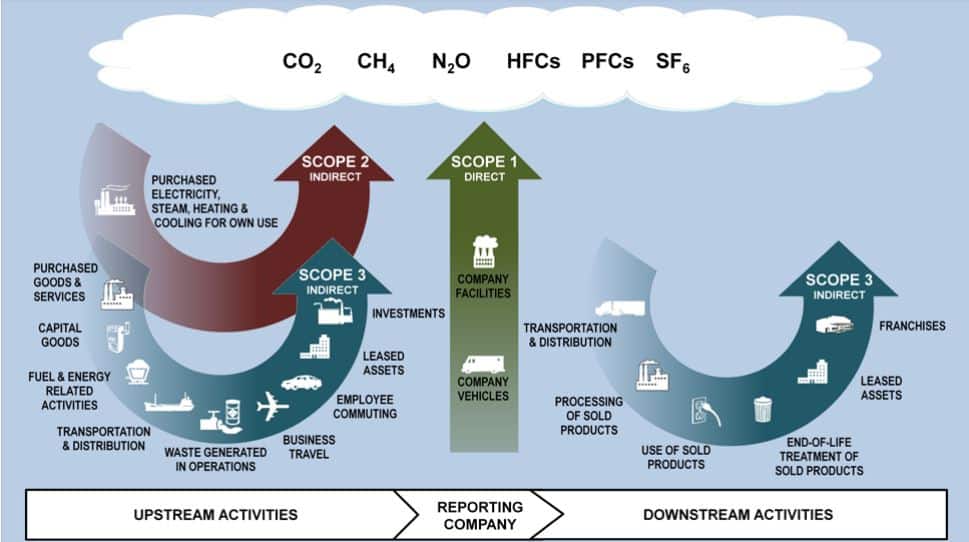

Scope 3 emissions, as defined by the Greenhouse Gas Protocol (GHG Protocol), cover all indirect emissions from a company’s value chain that are not owned or controlled by the company itself. These emissions extend beyond the direct operations (Scope 1) and purchased energy (Scope 2) emissions of a company.

The GHG Protocol is a collaboration between the World Resources Institute and the World Business Council for Sustainable Development. It sets global greenhouse gas accounting and reporting standards, such as The GHG Protocol Corporate Accounting and Reporting Standard and The Corporate Value Chain (Scope 3) Standard. These standards are widely adopted by corporations and regulators.

- In 2016, 92% of Fortune 500 companies responding to the CDP climate questionnaire used GHG Protocol standards either directly or indirectly.

The GHG Protocol breaks down Scope 3 emissions into 15 distinct categories, covering both upstream and downstream activities.

Companies determine their own Scope 3 boundaries and report based on the categories’ relevance and materiality to their business. This can result in varying emissions profiles even among companies in the same sector.

The differences in emissions profiles present a significant challenge in addressing this type of emissions. For instance, Alphabet considers emissions from downstream leased assets as “not relevant,” while Microsoft includes them in its emissions disclosure, despite their similar business nature.

In essence, it still depends on a company how it would regard a specific category. It’s up to them if the emission is material or not and relevant or irrelevant. In this case, providing enough disclosure details on emissions sources becomes even more important.

The Need for Improved Disclosure

Scope 3 emissions often represent the majority of corporate GHG emissions.

For example, oil companies’ Scope 1 and 2 emissions are a small fraction of their total emissions, while the consumption and combustion of their products account for most emissions.

In fact, CDP estimates that Scope 3 emissions make up 75% of related GHG emissions across all sectors. In the financial sector, financed emissions can be over 700 times greater than operational emissions.

Undeniably, emissions from the value chains have substantial impact but they are underreported or ignored most of the time. Large polluters simply claim that they have “no influence or control” over them. It is, thus, not surprising that Scope 3 emissions have lower disclosure rates than the other two emissions types.

Big companies like those included in the S&P Global 1200 index face more pressure to disclose their sustainability performance. Despite this, the overall Scope 3 disclosure rate across the wider market is likely much lower.

Add to that the fact that many businesses don’t provide a detailed breakdown of their value chain emissions, preventing investors from understanding the full extent of climate risk exposure along value chains.

The number of reported categories may offer some insight into the completeness of corporate disclosure. But there is still significant room for improvement in both the quantity and quality of Scope 3 disclosures.

Improved reporting will enable investors to better identify sources of emissions and potential solutions, ultimately contributing to a more accurate assessment of climate risks.

Why Net Zero Targets must Include, not Ignore Scope 3

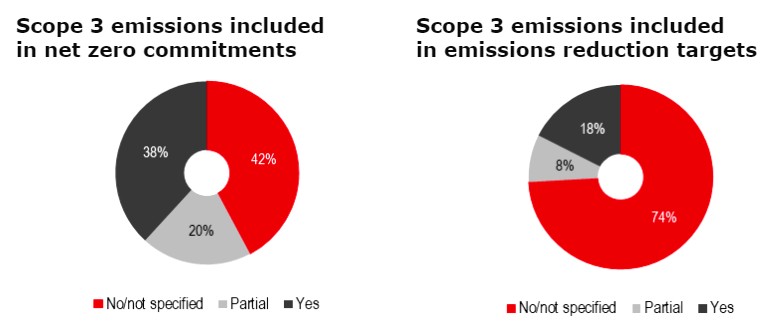

As the momentum for net zero commitments grows at both the national and corporate levels, many companies still fail to address Scope 3 emissions in their climate pledges.

Over 40% of corporate net zero targets do not cover Scope 3 emissions, even if they often represent the largest share of GHG emissions. Only 18% of companies in Net Zero Tracker’s survey of 2000 large, publicly-traded companies have set Scope 3 reduction targets.

The Science Based Target Initiative requires a Scope 3 target if a company’s relevant Scope 3 emissions are 40% or more of related GHG emissions. This is to ensure that corporate emission reduction targets are in line with the latest climate science.

Neglecting Scope 3 emissions in climate commitments not only weakens the overall climate strategy but also raises concerns about greenwashing.

For instance, Exxon Mobil faced criticism for its net zero announcement in January 2022, which included Scope 1 and 2 emissions while excluding Scope 3 emissions.

Similarly, Brazilian meatpacker JBS reported flat emissions over 5 years. But the Institute for Agriculture and Trade Policy disagreed, saying that JBS’ emissions actually increased by 51% during that period. The NGO claimed that JBS ignored its supply chain emissions in its disclosures and commitments, thereby guilty of greenwashing.

Considering the huge impact of these emissions, it is crucial for companies to include them in their net zero targets to effectively address climate risks and avoid greenwashing.

Not to mention the potential legal consequences they may face considering climate policies’ growing focus on value chain emissions.

Including Scope 3 Emissions in Climate Policies

Regulators are increasingly focusing on Scope 3 emissions, with some markets already implementing mandatory disclosure requirements:

US: The SEC requires publicly listed companies to disclose Scope 3 emissions if material or included in their GHG reduction goals. US funds will have to report the GHG footprint of their portfolios.

EU: The EBA plans to require banks to disclose financed Scope 3 emissions starting July 2024. The European Commission proposes all large and listed companies to report in compliance with the European Sustainability Reporting Standards (ESRS), which require Scope 3 emissions disclosure.

New Zealand: The External Reporting Board proposed mandatory Scope 3 disclosure, emphasizing the need to cover the entire value chain.

Singapore: Singapore Exchange requires listed companies to report Scope 1, 2, and 3 emissions when appropriate.

The Disclosure Club and Climate Litigation

More jurisdictions will join the “mandatory disclosure club,” especially as the International Sustainability Standards Board (ISSB) includes Scope 3 emissions in its draft climate-related disclosure requirements. The official standards, expected by the end of 2022, could catalyze wider adoption of reporting standards and policy requirements for Scope 3 emissions.

Moreover, climate stress tests by central banks now include value chain emissions as a climate risk metric. Examples are the European Central Bank (ECB) and the People’s Bank of China (PBoC). Banks with high exposure to climate risks may face higher capital reserve requirements.

Climate change-related litigation is also on the rise, with some cases focusing on Scope 3 emissions. They have been brought into the courts, such as the case with Royal Dutch Shell. The court obliged Shell to reduce emissions relating to its entire energy portfolio, including value chain emissions.

The case makes it even more important for investors to be aware of the legal risks associated with value chain emissions and their significance in climate risk assessments.

Carbon pricing mechanisms rarely apply to Scope 3 emissions; but they can impact the costs of companies with high value chain emissions, such as those in the real estate sector.

Accounting for Scope 3 Emissions

Accounting for Scope 3 emissions becomes even more challenging due to the discretion allowed in selecting relevant categories, data availability, and sector applicability. But understanding of Scope 3 emissions is growing, and a more nuanced approach to disclosures will soon evolve.

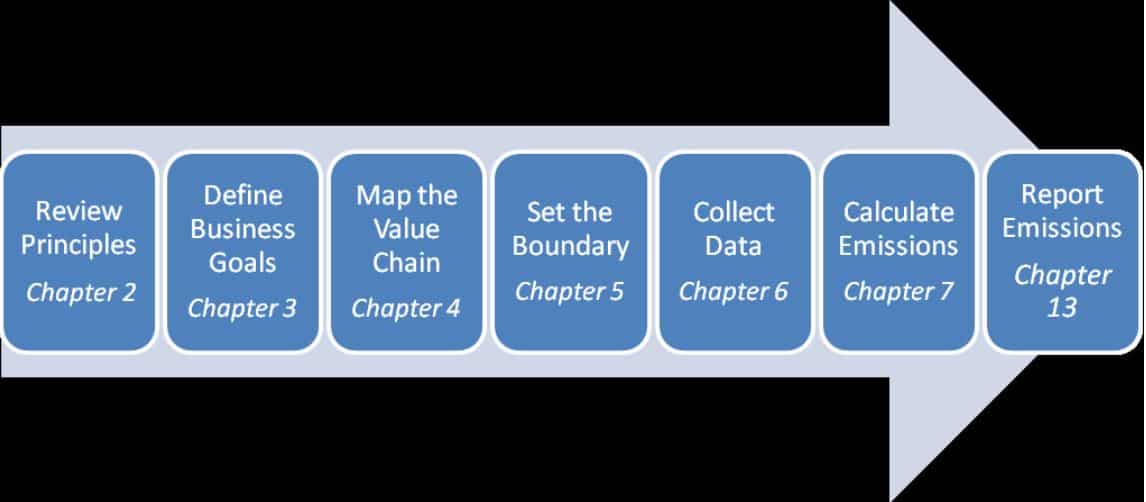

Despite the more challenging accounting for value chain emissions, it shares the same principles as Scope 1 and 2 emissions. The major difference is the identification of relevant activities and boundary setting.

In general, here’s the overview of the steps involved according to GHG Protocol:

Overview of Steps in Scope 3 Accounting & Reporting

Key points when accounting for emissions from value chain:

- Flexibility in selecting relevant categories can make calculations, analysis, and comparisons challenging. Companies may exclude categories that are actually material to their business.

- Timing of emissions adds complexity to Scope 3 accounting, as some emissions occur in the current year, while others may have occurred in the past or are yet to occur.

- Double counting may occur as Scope 1 and 2 emissions for one company can be Scope 3 emissions for another. Aggregating Scope 3 emissions across companies or subsidiaries should be avoided.

- Scope 3 emissions are more relevant to some sectors than others, and disclosure rates can provide an indication of relevance.

Overall, instead of aggregating across several companies, investors and companies should focus on analyzing Scope 3 emissions at an individual company level to determine exposure. This approach will offer a more complete picture of a business’s overall exposure to potential climate risks and impacts.