Why do companies have to consider carbon credit accounting along with their climate goals?

This question has been bouncing around the corporate world for several years. But its urgency began to kick in when the Securities and Exchange Commission released its initial GHG emissions disclosure rule.

The proposed regulation requires public firms, particularly the big ones, to report emissions. This includes Scopes 1 and 2 as well as Scope 3 emissions if found material.

And a big change the rule will cause is how companies will account for emissions transactions in their financial reports.

This guide will help address this concern. It will help you know how to weigh the effects of top net zero initiatives on financial reporting.

It will also provide guidance on how carbon credit or allowance items will be accounted for with some illustrative examples.

Carbon Credit Accounting and Achieving Net Zero

Investors, consumers, and regulators worldwide are making emissions reporting imperative for businesses.

Hence, the concept of net zero emerged. It’s a balancing act between the amount of emissions produced and the offsets and emissions reduced/removed from the air.

A simple yet profound quote “reduce what you can, offset what you can’t” has never been more vital to hit net zero.

There’s no single approach that works for any business, big or small, to account for its climate goals. Be it a net zero, carbon neutral, or carbon negative target.

The most effective strategy toward net zero is a combination of various actions. These include:

- Emissions reduction across the value chain (Scopes 1, 2, and 3 emissions)

- Removal of unavoidable emissions (with corresponding carbon removal credits)

- Offsetting emissions via carbon credit investments in green / carbon / sustainable projects

A carbon credit is a tradable permit given to an entity that represents the amount of CO2 it’s allowed to emit.

So, accounting for each carbon credit that a company has is important in its journey to net zero.

Despite some confusion surrounding the three actions above, corporate net zero pledges are ramping up. Many Fortune 500 companies have pledged to reduce their Scope 1 or direct emissions.

Firms that haven’t considered cutting their indirect emissions (Scopes 2 and 3) may be in a disadvantaged position. Their business partners may look for others with clear CO2 reduction targets, for instance.

Or worse, they could be placing themselves at reputational risk or even a lower market cap. In this sense, knowing how to create and execute a net zero plan is crucial to do away with the risks involved.

And a sure-fire way to that is understanding the common net zero initiatives and how they affect financial accounting.

Common Net Zero Initiatives and Their Impact on Financial Reporting

Developing a good approach to getting net zero needs consideration of various means.

For instance, a company has to recognize what current technology is out there or what’s underway. It also has to know what others in the firm’s ecosystem are doing that may cause Scope 3 emissions.

Most important is that the costs of each selected strategy has to be accounted for.

The major accounting guideline for some net zero initiatives in the U.S. is the Generally Accepted Accounting Principles (GAAP). And the GAAP mostly reflects the key international accounting principles of the International Accounting Standards Board (IASB).

So, a company may use the IASB accounting guidelines which most firms do. Or it may be necessary for a firm to make its own accounting policies based on certain transactions.

Here are the 3 common net zero strategies businesses are using today and their impact on financial reporting.

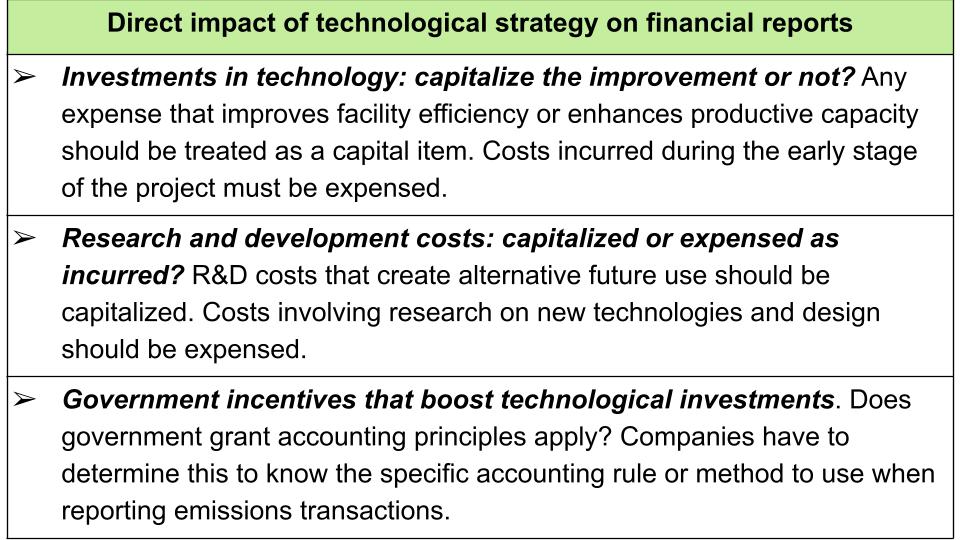

Technology and its impact on financial statements:

Technological solutions are a major path taken by many companies toward net zero. They invest in capital projects that improve efficiencies of operations while reducing emissions.

Most common examples are electrification and making buildings or infrastructures greener (green certifications).

Others are focusing on research and development (R&D) to improve technology to both reduce and remove carbon. Examples include Direct Air Capture (DAC), carbon mineralization, and growing algae in deserts.

Here are major accounting considerations to make when exploring this carbon reduction initiative.

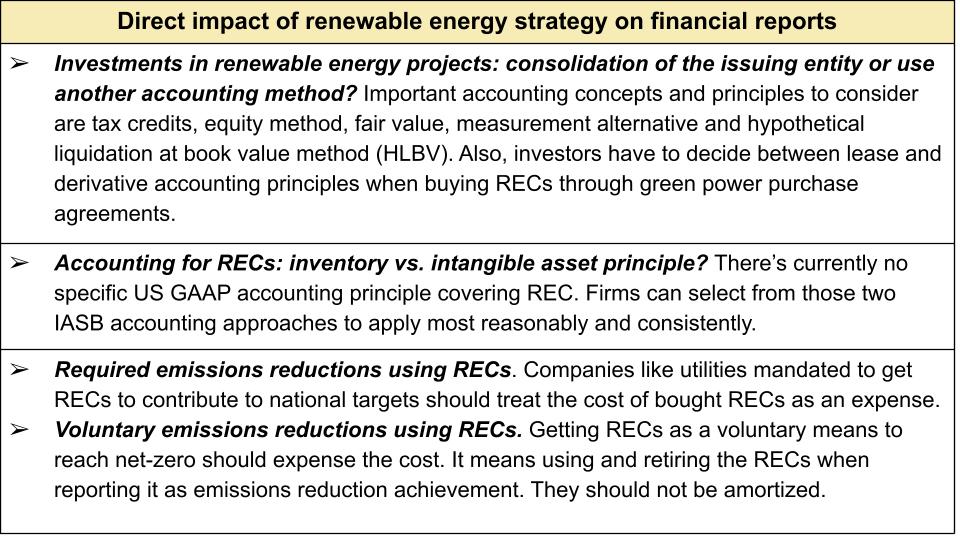

Renewable energy and its impact on financial statements:

A lot of companies and countries are investing in renewable sources (wind, solar, hydro). This net zero strategy generates the REC or Renewable Energy Credit. Each megawatt-hour of electricity produced from a renewable resource creates one REC.

A state or jurisdiction or an agency certifies REC. It can also be tradable between firms similar to carbon credits. A company may invest directly in renewable projects to earn RECs. It can also buy it from power generators or move to a greener facility to claim RECs.

REC holders can use the credits to offset power used from other sources and account for the reduced emissions into net zero goals. Accounting for these carbon credit alternatives is a bit more complex.

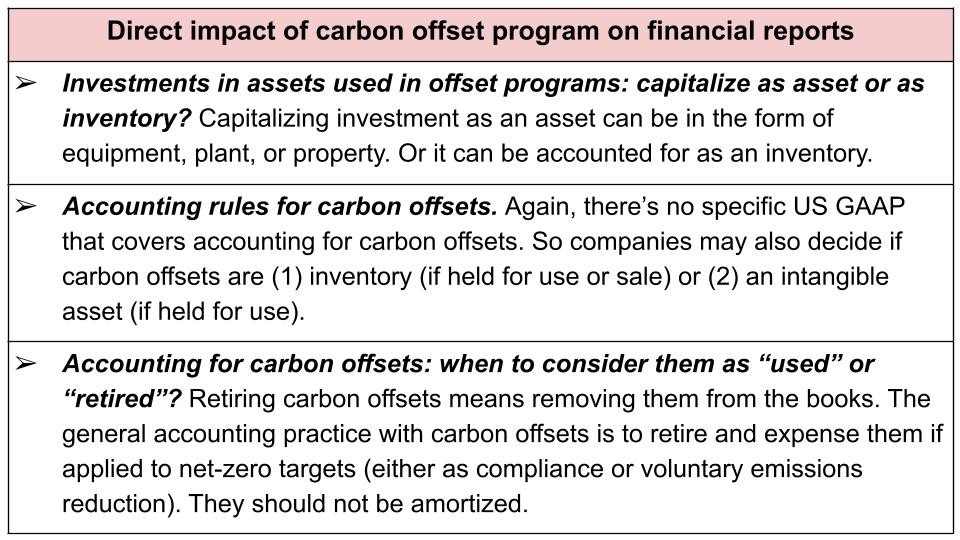

Carbon offset program and its impact on financial statements:

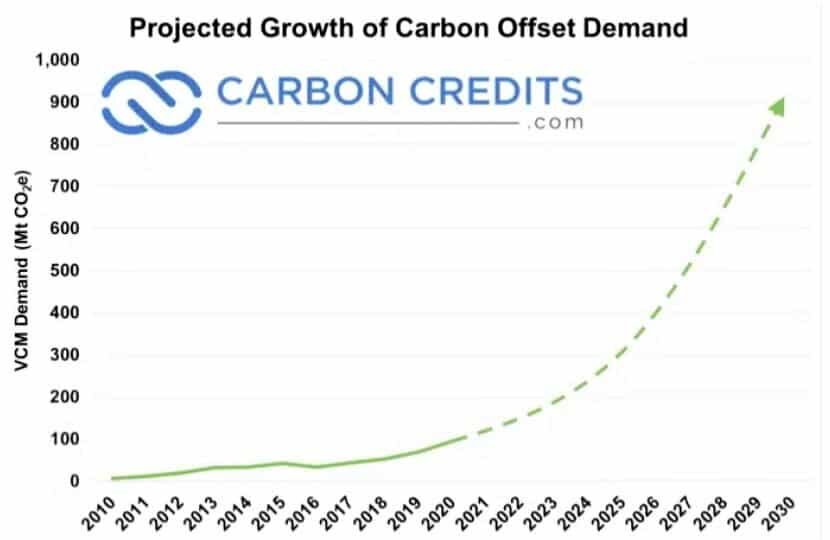

Many emitters are using this net zero initiative to offset emissions they can’t reduce. In fact, the projected growth in demand for carbon offsets in this decade looks very promising as shown in the chart below.

There are plenty of programs that generate carbon offsets. Common ones include reforestation, farming or agriculture management, and carbon capture.

Each project produces a certain amount of carbon offsets, depending on its nature and capacity to reduce or remove CO2 from the air.

Companies have to be diligent in picking the projects to source their carbon offsets. They need to ensure the quality of offsets they buy.

There must also be a credible body that verifies the program and the calculations of emissions reductions are accurate. Here’s our complete guide on how offsets are created, purchased, and used.

How is Accounting Done for Carbon Credit?

Unfortunately, there’s a variety of carbon credit accounting issues due to the lack of mandatory rules until now. So, this section provides some insights on how to tackle this matter.

Key International Accounting Bodies for Carbon Credits

-

Emerging Issues Task Force (EITF) in 2003

-

International Financial Reporting Interpretations Committee (IFRIC) in 2004

-

International Accounting Standards Board (IASB) with Financial Accounting Standards Board (FASB) in 2007

The IASB Accounting Principles

-

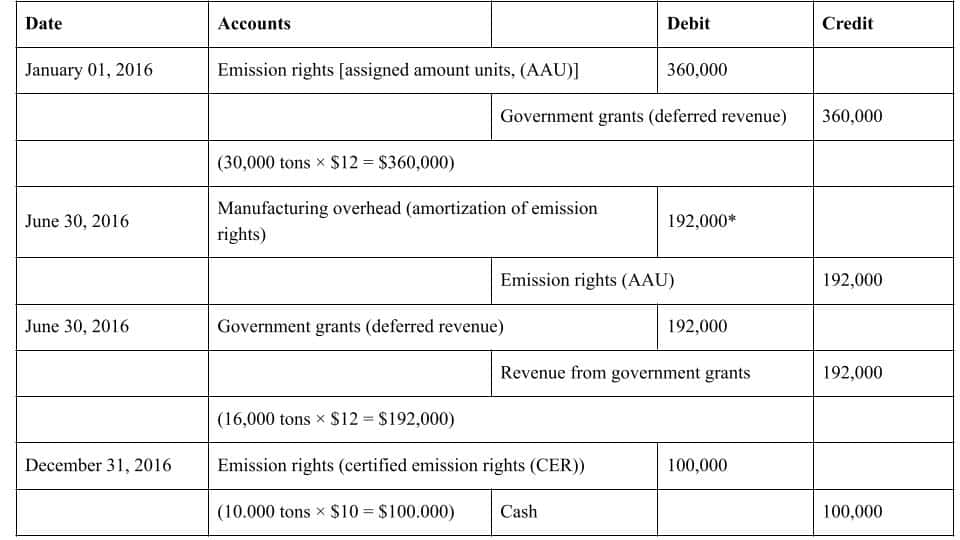

Emission allowances (CER) are intangible assets and measured following IAS 38 Intangible Assets

-

If the CER is from a government, an entity can treat the credits as government grants on initial recognition (IAS 20)

-

As an entity produces emissions, a provision for its obligation is recognized to deliver allowances as per IAS 37

-

IAS 2: an entity must account for inventories at a lower cost and net realizable value

-

Net realizable value: estimated selling price less estimated costs of completion and other costs to make the sale.

-

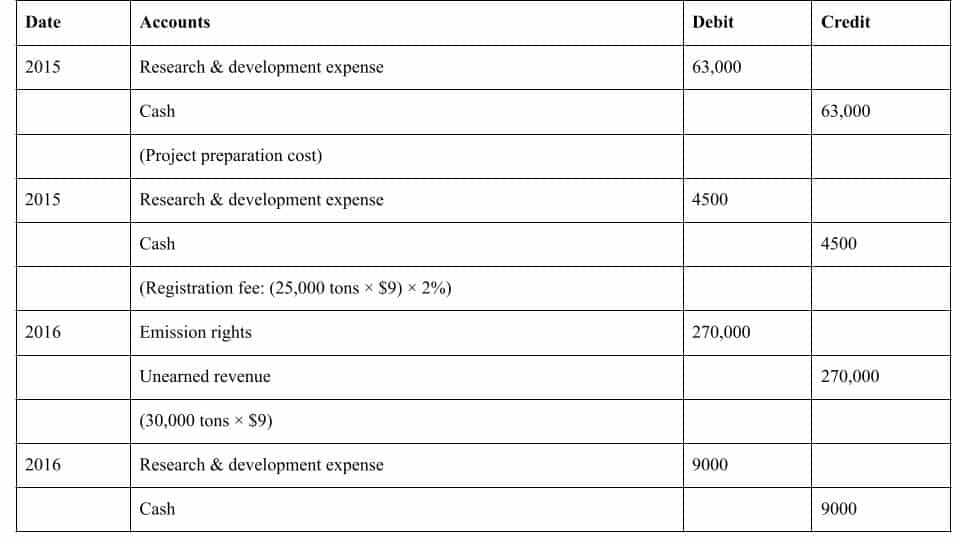

Research costs from exploring measures to reduce emissions

-

Costs incurred in developing the selected alternative measures

-

Cost of preparing the Project Design Documents

-

Registration fees with the United Nations Framework Convention on Climate Change (UNFCCC)

Accounting for Carbon Credits under a Voluntary Market

- But more importantly, these credits created a dominant market mechanism that helps cut emissions. They give companies and countries viable options to reverse climate change effects.