Russia’s increasing influence in African countries and its focus on critical minerals pose significant challenges for the West. In a historic announcement on March 16 this year, Niger declared the immediate termination of its military cooperation with the US. The country nullified a military agreement that permitted US bases on its territory.

Critics argue that Russia’s resource-driven approach may exacerbate existing governance challenges, including corruption, environmental degradation, and social unrest.

As reported by Oregon News, Niger’s military junta and US officials, had a crucial meeting during which the latter conveyed apprehensions regarding Russia’s growing military involvement in the nation. Niger made the “announcement” immediately after the meeting. Additionally, concerns were raised about attempts by the junta to renegotiate mining contracts with potential implications for energy leverage against Western interests.

Let’s learn how Russia’s pursuits for Africa’s critical minerals can impact the country and its global resource acquisition efforts.

Russia’s Quest for African Mineral Resources

One of the focal points of Russia’s interest lies in rare earth elements (REEs), essential components in various high-tech applications, including electronics, renewable energy technologies, and defense systems.

Africa boasts 30% of the world’s mineral reserves, making it an attractive target for resource-hungry nations like Russia.

The Democratic Republic of Congo (DRC) emerges as a prime target in Russia’s mineral quest, given its abundant cobalt reserves, a crucial element in lithium-ion batteries powering EVs and smartphones. Russia’s interest in cobalt aligns with its ambitions to establish a stronger foothold in the rapidly expanding electric vehicle market.

In addition to cobalt, Russia has set its sights on other critical minerals such as lithium, vanadium, and platinum group metals. All these REEs are indispensable to modern industries involved in energy storage, battery and catalytic converters, etc.

Furthermore, Russia had always weighed minerals as a currency. They have intervened in Africa to bolster their control through paramilitary means. By providing security and employing intimidation tactics, Russia grabbed lucrative mining agreements. Furthermore, it offers military support to sustain the weaker regimes.

Russian tactics are in absolute contrast to the Western nations. The country operates ruthlessly without considering human rights, democracy, or legal frameworks.

Russia Intensifies Use of Private Military Companies (PMCs) in Africa

According to media reports, in recent years Russia has increased deployment of private military contractors (PMCs) to put a tight foothold on the continent. PMCs are for-profit organizations that provide combat, security, and logistical services for hire.

Russian PMCs first arrived in Africa under a contract with the Libyan Cement Company in 2017.

One notable example of Russia’s use of PMCs in Africa is its involvement in the Central African Republic (CAR). In 2018, the Russian government signed a military cooperation agreement with the CAR, leading to the deployment of the Wagner Group, the most famous Russian PMC.

Subsequently, the PMCs have swiftly extended their presence into Sub-Saharan Africa. They operate in Sudan, the Central African Republic (CAR), Madagascar, Mozambique, and Libya.

The group trains local armed forces to use Russian-supplied arms, protects Russian-operated gold, uranium, and diamond mines, and acts as bodyguard and advisor to the Central African president.

Africa’s Share of Critical Mineral Wealth

A few years back the World Bank projected that a ~ 500% rise in the production of key minerals and metals like lithium, graphite, and cobalt by 2050 is needed to meet global demand for REEs.

With a focus on revenue within Africa, the McKinsey Group has conducted an evaluation. It states:

- Africa could generate between US $200 million and US $2 billion of additional annual revenue by 2030 and create up to 3.8 million jobs by building a competitive, low-carbon manufacturing sector.

- Additionally, minerals could play a crucial role in meeting African citizens’ huge housing and transport needs by driving the sustainable development of these sectors.

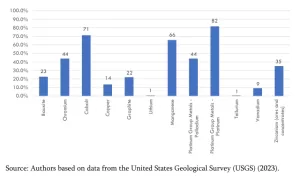

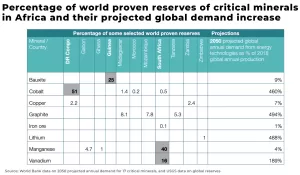

Africa holds 40% of the world’s gold and up to 90% of its chromium and platinum reserves. The continent also possesses the largest cobalt, diamonds, platinum, and uranium globally. Zimbabwe has huge lithium potential while Zambia’s copper reserves are capable of substantial revenue generation.

Despite owning 30% of the world’s mineral reserves, Africa accounts for less than 10% of global mining exploration spending. For instance, untapped raw mineral deposits in the DRC are estimated to be worth more than US$24 trillion.

Therefore, accessing Africa’s abundant resources is imperative to achieve these ambitious goals.

Image: Distribution of Africa’s shares of global production of selected critical minerals.

Russia’s Engagement in Africa: Understanding Strategic Motivations

1. Bypassing sanctions: Gold and diamonds provide Russia with a means to circumvent economic sanctions enforced since the invasion of Ukraine. Africa, boasting 40% of the world’s gold reserves and the largest diamond reserves, serves as a key resource hub.

2. Geopolitical influence: As already explained, Russia has established fresh military and political alliances to reduce Western influence in African nations. Specifically, Russia offers “regime survival packages” in exchange for natural resource extraction rights, bolstering its geopolitical standing. This serves as a huge vantage point for native Africans.

Moreover, Russia’s engagement in African mineral extraction extends beyond traditional mining operations. The Kremlin has forged strategic partnerships and investment deals with African nations, leveraging its resource extraction and infrastructure development. These partnerships often come bundled with political and military agreements, bolstering Russia’s influence in Africa.

A stark example is the Blood Gold Report’s Findings that stated,

“The Kremlin has earned more than US$2.5 billion from trade in African gold since Vladimir Putin launched his full-scale invasion of Ukraine in February 2022.”

Is Russia’s Intervention Loosening the West’s Grip on Africa?

The intensification of Russia’s mineral scramble in Africa has raised concerns among Western powers and regional stakeholders. They anticipate worse implications from the geopolitical dynamics and local governance. Critics argue that Russia’s resource-driven approach may exacerbate existing governance challenges, including corruption, environmental degradation, and social unrest.

Furthermore, Russia’s expanding presence in African mineral extraction poses a potential challenge to Western dominance in resource markets. It prompts calls for increased vigilance and strategic engagement from Western policymakers.

Niger’s Recent Decision: A Threat to the West

Niger, the world’s seventh-largest producer of uranium, supplies France this vital resource for nuclear power generation. Apart from uranium, Niger has abundant natural resources of coal, gold, iron ore, and phosphates.

However, Niger’s recent decision to temporarily halt the issuance of new mining licenses highlights the challenges faced in maintaining stable supply chains.

Niger’s situation exemplifies the broader concern regarding Russia’s increasing influence in African nations.

It poses a looming threat to the West in securing its critical mineral supply chains. The withdrawal of US troops from neighboring Chad is another testament to the burgeoning geopolitical tensions.

Jack Watling, land warfare specialist at the Royal United Services Institute (Rusi) has examined the situation and commented,

“While lithium and gold mines are clearly important, in Niger the Russians are endeavoring to gain a similar set of concessions that would strip French access to the uranium mines in the country.”

Image: Share of Africa’s critical minerals and their global demand projections

As Russia continues to deepen its involvement in Africa’s mineral sector, the geopolitical implications will likely reverberate far beyond its borders. Balancing the economic opportunities with the geopolitical risks inherent in this mineral scramble will be paramount for both African nations and the broader international community.