The United States is stepping up its push for small modular reactors (SMRs) in the Philippines. In mid-February 2026, the U.S. Trade and Development Agency (USTDA) announced $2.7 million in technical assistance for Meralco PowerGen Corp. (MGEN). The work will review advanced U.S. SMR designs and create an implementation roadmap for what could become the country’s first SMR nuclear power plant.

USTDA framed the project as “vendor-neutral” evaluation support that can help the Philippines compare options and plan the steps needed to move from concept to construction. The goal is to speed early planning, such as technical screening and sequencing, before major capital decisions.

This is not a power plant approval. It is a funded study and planning effort. Still, it signals stronger U.S. backing for nuclear cooperation at a time when the Philippines is looking for more reliable, low-carbon power sources.

Meralco Chairman Manuel Pangilinan remarked:

“Through the generosity of the US government, we are laying the groundwork for the responsible integration of nuclear into our energy mix through small modular reactors. This offers a safe and responsible pathway towards energy security for generations to come.”

Coal Dependence and Rising Demand Drive the Debate

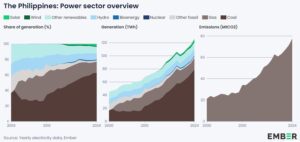

The Philippines still relies heavily on fossil fuels for electricity. Official DOE data show that in 2024, total power generation reached 126,941 GWh. Coal produced 79,359 GWh, which is about 62.5% of the country’s electricity that year.

- Natural gas produced 18,047 GWh (about 14%). Renewable energy produced 28,193 GWh (about 22%). Oil produced 1,342 GWh (about 1%).

On the capacity side, the DOE reported 29,706 MW of total installed generating capacity in 2024, with the following breakdown:

- Coal capacity was 13,006 MW (about 44%);

- Renewable energy capacity was 9,520 MW (about 32%);

- Natural gas was 3,732 MW (more than 12%); and

- Oil was 3,448 MW (almost 12%).

Demand growth also shapes this debate. In the DOE’s power planning materials, the country’s peak demand is projected to rise from 16,596 MW in 2022 to 68,483 MW by 2050, which the DOE notes equals an average annual growth rate of 5%.

These numbers help explain why policymakers and utilities are reviewing many options at once. They include grid upgrades, energy efficiency, renewables, storage, gas, and now nuclear.

SMRs Explained: Smaller Reactors, Big Expectations

An SMR is a nuclear reactor designed to be smaller than traditional large reactors. The International Atomic Energy Agency (IAEA) defines SMRs as reactors with a capacity of up to 300 MW(e) per unit. That is roughly one-third of the size of many conventional reactors.

The image is an example of an SMR design by NuScale Power, an American SMR company.

Supporters point to three practical features. First, SMRs aim for modular construction. Developers may build parts in factories and assemble them on site. Second, SMRs can be scaled by adding modules over time. Third, SMRs can provide steady output that does not depend on weather, which can help a grid manage variability from wind and solar.

At the same time, SMRs do not remove hard requirements. Any nuclear project still needs a strong regulator, safe site selection, trained staff, emergency planning, fuel and waste plans, and long-term financing. These items often drive timelines and costs, especially for a first plant in a country that is new to commercial nuclear power.

Small Reactors, Big Global Ambitions

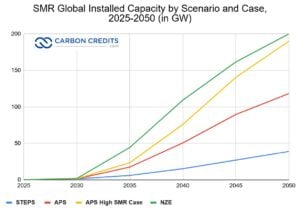

Around the world, interest in small modular reactors is growing fast. Designers have created more than 120 SMR designs in recent years, with dozens in early review or licensing stages.

The global market for SMRs is also expanding. Analysts estimate the value of SMR markets at several billion U.S. dollars today, and rising over the next decade. Some forecasts show markets increasing to roughly double or more by the early 2030s, around $10–16 billion.

Installed SMR capacity is also expected to rise. Industry reports project several hundred megawatts of capacity by 2030, with further growth as more designs reach construction, up to 2.0 GW per IEA forecast.

Countries in North America, Europe, and the Asia Pacific are leading deployment and planning. Many governments see SMRs as a way to add reliable, low-carbon power alongside renewables.

Global forecasts to 2050 show SMRs could play a bigger role in clean energy systems, especially under scenarios that aim for low emissions and stable power. However, real deployment depends on licensing, investment, and supply chain development.

The 123 Agreement: Legal Groundwork for Nuclear Cooperation

A key reason U.S. firms can offer nuclear technology is the U.S.–Philippines Agreement for Cooperation in the Peaceful Uses of Nuclear Energy, often called a “123 Agreement.” The U.S. State Department said the agreement entered into force on July 2, 2024. It sets the legal framework for civil nuclear cooperation and can support exports of nuclear material, equipment, and components under U.S. rules.

In practice, this type of agreement is one building block. It does not select a reactor design and does not guarantee financing. It does create the conditions for deeper technical engagement, training, and potential commercial activity, as long as both sides meet non-proliferation and regulatory requirements.

From Planning to Licensing: Mapping the Nuclear Timeline

The Philippines began its nuclear journey after the 1973 oil crisis. It built the 621 MWe Bataan Nuclear Power Plant in 1984 at a cost of USD460 million. However, safety and financial concerns stopped it from operating. The plant was never fueled but has been maintained.

The DOE has publicly set nuclear targets in its 2022 planning. Reporting around the Philippine Energy Plan has cited a pathway that aims for at least 1,200 MW of nuclear capacity by 2032, rising to 2,400 MW by 2035, and 4,800 MW by 2050.

The DOE has also discussed regulatory readiness. In a November 2025 media release, the DOE said the Philippines aims to begin accepting nuclear power plant license applications by 2026, linked to the creation of the country’s nuclear safety regulator under Republic Act No. 12305.

International reviews add more context. In December 2024, the IAEA reported that the Philippines was making progress on nuclear infrastructure development, while still working through the many steps needed for a full nuclear power program.

Against that timeline, the USTDA-MGEN work looks like an “early stage” accelerator. It helps narrow design choices and map steps. It does not replace the national licensing process.

Geothermal’s Role in a Future Nuclear Mix

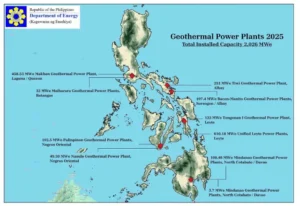

The Philippines already has a major source of steady renewable power: geothermal energy. DOE statistics list 1,952 MW of geothermal installed generating capacity in 2024. Geothermal generation reached 10,789 GWh in 2024.

This matters for the SMR discussion because many people describe nuclear as “baseload,” meaning it can run day and night. In the Philippines, geothermal already provides a similar kind of steady output in many areas. The challenge is that geothermal expansion depends on location, drilling success, and up-front exploration risk.

This is why planners often look at a mix. They can expand renewables like geothermal, hydro, wind, and solar, while adding storage and grid upgrades. They can also evaluate nuclear for future reliability needs, especially if coal plants retire over time.

For the U.S. side, the near-term goal is clear. It wants U.S. designs and services to be part of the shortlist. For the Philippines, the task is also clear. It must match any technology choice to national needs, grid limits, safety rules, and long-term affordability.