China closed 2025 with its largest annual expansion of the energy system on record. Investment surged past a symbolic threshold. Power capacity grew at a pace rarely seen in any major economy. Together, the numbers point to a system still in rapid build-out, with renewables at the center and grids struggling to keep up.

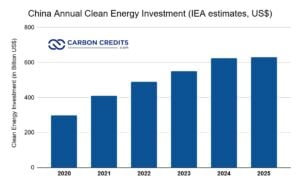

By the end of January 2026, the National Energy Administration (NEA) announced that China’s investment in major energy projects topped 3.5 trillion yuan in 2025, or nearly US$500 billion. This marks an almost 11% rise from the previous year and is the first time China’s annual energy investment has hit that level.

This spending surge coincided with another milestone. By the end of 2025, China’s total installed power generation capacity reached 3.89 terawatts (TW), up 16.1% year on year. No other country added capacity at a comparable scale during the year.

$500B Flows Across the Energy System: Power, Grids, and Security

The NEA described 2025 as a year of broad-based energy investment. Spending increased not only in clean energy but also in grids, coal, and energy security projects.

Renewables absorbed a large share of new capital. China added more than 430 gigawatts (GW) of new wind and solar capacity during the year. This pushed combined installed wind and solar capacity beyond 1.8 TW for the first time. Solar and wind now account for nearly half of China’s total installed power capacity.

Investment in onshore wind rose especially fast. The NEA said spending on key onshore wind projects jumped by almost 50% compared with 2024. Developers focused on large inland bases and projects tied to long-distance transmission lines.

Solar continued to expand at an even faster pace. By the end of 2025, China’s installed solar capacity reached 1.20 TW, up 35.4% from a year earlier. This followed another strong year in 2024 and confirmed China’s position as the world’s largest solar market by a wide margin.

Wind capacity also grew quickly. Total installed wind power reached 640 GW, a 22.9% increase from 2024. Growth came from both onshore projects and steady additions offshore.

At the same time, investment did not shift entirely away from conventional energy. The NEA said spending also increased in coal power, hydropower, and coal mining, reflecting ongoing concerns about power reliability and supply security.

Grid construction remained a priority, particularly projects designed to move electricity from resource-rich western regions to demand centers in the east. Private companies played a larger role in this expansion.

The NEA reported that private-sector investment in major energy projects rose to almost 13% year-on-year. Much of that capital flowed into solar manufacturing, wind development, and coal-related infrastructure.

China’s Capacity Additions in Gigawatt Chunks

China’s investment surge translated into record growth in installed capacity. At the end of 2024, total power capacity stood at about 3.35 TW. One year later, it had risen to 3.89 TW. This implies net additions of roughly 540 GW in a single year.

That figure reflects capacity from all sources, including renewables, coal, gas, nuclear, and hydropower. While the NEA does not publish a single “net additions” number, the difference between year-end totals shows the scale of expansion.

Solar alone accounted for a large share of this growth. Industry data based on official statistics indicate that China added roughly 315 GW of new solar capacity in 2025. Wind additions added another large block, pushing combined wind and solar growth above 430 GW.

This pace of construction is historically unusual. Even during earlier phases of China’s renewable boom, annual additions were far smaller. The 2025 figures show that China is now building new power capacity at a speed measured in hundreds of gigawatts per year, not tens.

By contrast, capacity growth in many other major economies has slowed due to permitting delays, grid constraints, and financing challenges. China’s ability to add large volumes of capacity in a short time reflects its centralized planning, domestic manufacturing base, and strong state-backed financing.

- READ MORE: China’s One Month Lithium Battery Energy Storage Installations Beat America’s One Whole Year

China vs. the United States: A Scale Gap That Keeps Widening

The scale of China’s 2025 build-out becomes clearer when placed in an international context.

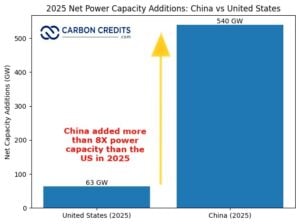

In the United States, the Energy Information Administration (EIA) projected about 63 GW of new utility-scale generating capacity additions for 2025 across all technologies. This includes solar, wind, gas, battery storage, and other sources.

China’s wind and solar additions alone, at more than 430 GW, were roughly six to seven times larger than total expected US utility-scale additions for the year. If total net capacity growth is used instead, China’s increase of about 540 GW would be more than eight times the US figure.

These comparisons depend on definitions and data sources. China’s numbers are based on year-end installed capacity totals, while the US figure is a forward-looking projection of new builds. Even so, the gap in scale remains large under most reasonable comparisons.

What stands out is not only the size of China’s additions, but their composition. Renewables drove most of the growth. Solar capacity in China alone now exceeds the total installed power capacity of many advanced economies.

When Building Faster Than the Grid Can Absorb

Rapid capacity growth has consequences. One clear signal appeared in power plant utilization data.

In 2025, power plants with a capacity of 6,000 kilowatts and above recorded an average utilization of 3,119 hours. This was 312 hours lower than in 2024. Lower utilization suggests that capacity is growing faster than electricity demand or grid flexibility.

Several factors explain this trend. Wind and solar output vary by weather and time of day. Coal and hydropower plants remain in the system to provide stability, even when renewables generate strongly. In addition, grid bottlenecks can prevent power from reaching where it is needed.

The NEA has repeatedly pointed to grid expansion as a priority. In 2025, major investments went into ultra-high-voltage transmission lines, regional interconnections, and grid digitalization. These projects aim to reduce curtailment and improve the system’s ability to absorb renewable power.

Still, the utilization figures show the challenge ahead. As capacity continues to rise, grid management and market reform will play a larger role in determining how efficiently new assets are used.

Growth First, Optimization Next

China’s 2025 energy data tell a consistent story. Investment reached a new high. Capacity expanded at a historic pace. Renewables dominated new additions, but conventional power and grids remained part of the strategy.

The numbers also show a system in transition rather than completion. Record build-out has brought new pressures, especially on utilization and grid integration. These issues are likely to shape energy policy decisions in the years ahead.

For now, what stands out most is scale. With energy investment approaching $500 billion and annual capacity additions measured in hundreds of gigawatts, China continues to expand its power system faster than any other country. The 2025 data confirm that this expansion is no longer an exception, but an established pattern.