ExxonMobil closed 2025 with strong profits, robust cash generation, and massive shareholder payouts. However, weaker crude prices and soft chemical margins weighed on earnings. The company still reinforced its narrative of being a leaner, more technology-driven oil major with growing exposure to lower-carbon opportunities.

For the full year, ExxonMobil reported $28.8 billion in earnings, down from $33.7 billion in 2024. Despite the decline, the company distributed $37.2 billion to shareholders, highlighting its commitment to capital returns. The results underline Exxon’s strategy: maximize cash from advantaged assets while gradually scaling low-carbon investments.

CEO Darren Woods said the company is structurally stronger than a few years ago, with disciplined capital allocation and resilient earnings power. He also emphasized a long runway of profitable growth through 2030 and beyond.

Exxon’s Financial Performance: Lower Earnings, Strong Cash Flow

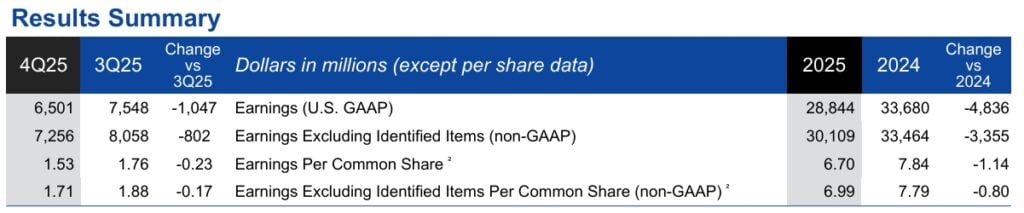

ExxonMobil delivered fourth-quarter 2025 earnings of $6.5 billion, or $1.53 per share. Excluding special items, earnings rose to $7.3 billion, or $1.71 per share. The company generated $12.7 billion in operating cash flow and $5.6 billion in free cash flow during the quarter.

For the full year, cash flow from operations reached $52.0 billion, while free cash flow totaled $26.1 billion. ExxonMobil said its operating cash flow has grown at roughly 10% annually since 2019, outperforming many peers.

However, earnings declined due to weaker oil prices, softer chemical margins, higher depreciation, and rising growth-related expenses. Lower interest income also affected results. These headwinds were partly offset by higher production, structural cost savings, and strong refining margins.

Capital Efficiency Drive Competitive Edge

Cash capital expenditures reached $29.0 billion in 2025, including acquisitions. Exxon expects to spend $27–$29 billion in 2026, signaling continued investment in upstream growth and energy infrastructure.

As per analysts, Exxon Mobil (XOM) is a strong dividend stock with steady cash flow and high oil production. The company returned billions to shareholders through dividends and buybacks, making it attractive to income investors.

However, XOM stock depends heavily on oil prices and faces long-term risks from climate policies and weaker chemical margins. Overall, Exxon is a stable value stock, but not a high-growth play.

Upstream: Record Production and Advantaged Assets

ExxonMobil’s upstream segment generated $21.4 billion in earnings in 2025, down from $25.4 billion in 2024. Lower oil prices and reduced volumes from divestments weighed on performance. Higher depreciation also impacted earnings.

However, the company achieved its highest production in more than 40 years, reaching 4.7 million oil-equivalent barrels per day. Production surged to 5.0 million oil-equivalent barrels per day, with the Permian reaching 1.8 million and Guyana nearing 875,000 barrels per day.

Additionally, it also advanced several major projects.

- The Yellowtail project in Guyana started early and under budget.

- The Bacalhau offshore Brazil project launched in the fourth quarter.

- Golden Pass LNG completed mechanical work, with first cargoes expected in early 2026.

Energy Products: Refining Margins Boost Profits

The Energy Products segment earned $7.4 billion in 2025, up $3.4 billion from 2024. Higher refining margins, cost savings, and asset sales drove the growth. However, the refining business remained resilient.

Chemicals: Weak Margins and Impairments

The Chemical Products segment struggled, with earnings falling to $800 million, down $1.8 billion from 2024. Weak margins, impairment charges, and higher spending weighed on results.

The China Chemical Complex ramp-up added costs, though high-value product sales hit records. Q4 saw a $281 million loss. Despite challenges, Exxon expanded chemical capacity and launched two advanced recycling facilities, processing over 250 million pounds of plastic waste annually.

- PREVIOUSLY: ExxonMobil (XOM) Q3 Earnings Beat: Will AI and Innovation Secure Dividends in a Climate-Conscious Era?

$30 Billion Low-Carbon Strategy: CCS, Hydrogen, and New Materials

ExxonMobil continues to position itself as a major player in carbon capture, hydrogen, and lower-emission fuels. The company plans to invest up to $30 billion in lower-emission technologies between 2025 and 2030.

Management said rising carbon prices would make these investments more attractive and could significantly boost cash flow in the Low Carbon Solutions business. Exxon aims to scale projects in hydrogen, CO₂ storage, and industrial clusters to become a partner of choice for large emitters.

The company also emphasized its core strengths in subsurface engineering, large-scale project execution, and existing infrastructure as competitive advantages in the energy transition.

Methane and Air Emissions: Progress with Economic Logic

ExxonMobil reported significant progress on methane and air emissions. The company has reduced methane intensity by more than 60% since 2016 and targets 70–80% reductions by 2030.

Management framed methane reduction as both an environmental and economic opportunity. Keeping methane in the system increases gas sales and reduces losses. Exxon also noted methane’s high warming potential compared to CO₂, reinforcing the need for tighter controls.

Total reportable air emissions (VOCs, SOx, NOx) dropped about 25% from 2016 to 2024, even as throughput increased to record levels.

Long-Term Outlook: Oil Cash Funds the Transition

ExxonMobil believes demand for decarbonization solutions will rise significantly through 2050. The company expects carbon pricing and net-zero policies to drive capital toward carbon capture and hydrogen over time.

However, Exxon’s strategy remains pragmatic. The company will continue to maximize returns from oil, gas, and refining while gradually scaling low-carbon businesses. Management argues that each update to global net-zero scenarios increases the importance of lower-carbon solutions but does not change its core assessment of energy demand.

All in all, ExxonMobil’s 2025 results show a company balancing two worlds. On one hand, it remains a cash-generating oil and gas powerhouse with record production and industry-leading shareholder returns. On the other hand, it is cautiously expanding into low-carbon technologies without sacrificing profitability.