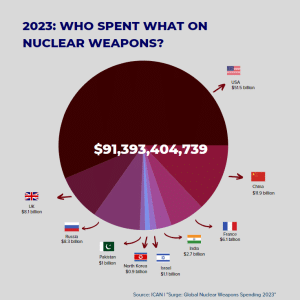

In 2023, the nine nuclear-armed states collectively spent a staggering $91.4 billion on their nuclear arsenals, according to ICAN’s latest report titled “Surge: 2023 Global Nuclear Weapons Spending”.

That amount translates to an astonishing $2,898 per second, underscoring the immense financial commitment to maintaining and modernizing nuclear weapons.

The Billion-Dollar Nuclear Breakdown

Here’s how the spending breaks down among the top four nuclear-armed nations:

- United States: The largest spender by far, allocating $51.5 billion, which accounted for 56% of the total expenditures among all nine nations. This spending also represented 80% of the overall increase in nuclear weapons spending compared to the previous year.

- China: Followed with expenditures totaling $11.8 billion, emphasizing its significant investments in its nuclear capabilities.

- Russia: Spent $8.3 billion, marking its ongoing commitment to maintaining a robust nuclear arsenal.

- United Kingdom: Saw a notable 17% increase in spending, reaching $8.1 billion, reflecting its continued investment in nuclear deterrence capabilities.

The report highlights a troubling trend of escalating spending on nuclear weapons over the past five years, totaling $387 billion. This period has seen a 34% increase in annual expenditures, illustrating a global push by these nations to modernize and expand their nuclear capabilities despite international efforts towards disarmament and non-proliferation.

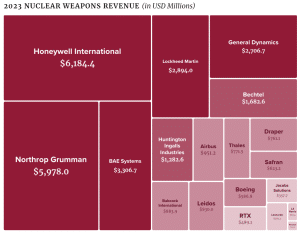

The financial windfall from nuclear weapons production also extends to private entities involved in their manufacture. Companies engaged in producing these weapons secured contracts worth at least $387 billion, some extending through 2040.

In 2023 alone, new contracts added up to nearly $7.9 billion, further fueling profits and incentivizing lobbying efforts. In the US and France alone, firms spent $118 million on lobbying activities aimed at influencing policy and public perception related to nuclear weapons.

The Price of Nuclear Power: What $91B Could Buy Instead

ICAN’s report underscores the opportunity costs associated with such sky-high spending. For instance, the $91.4 billion annual expenditure on nuclear weapons could alternatively provide significant benefits to address pressing global challenges.

This sum could fund renewable energy initiatives to power 12+ million homes with wind energy, cover a substantial portion of the funding gap (27%) needed to combat climate change, or even plant 1 million trees every minute.

Or that money could have been spent on purchasing uranium to fuel one of the cleanest energy sources – nuclear power. Industry reports show that investments in nuclear energy for the clean energy transition have not increased at the same pace as other energy sources like renewables.

Nuclear capacity additions also show the same trend, with nuclear remaining flat over the years and in the coming years.

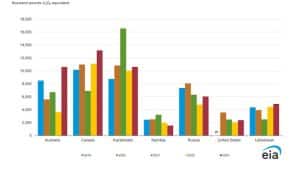

However, US utilities significantly increased their uranium purchases by 27% in 2023 compared to the previous year, according to the latest annual report from the US Energy Information Administration (EIA).

US civilian nuclear power reactors purchased a total of 51.6 million pounds of U3O8 (uranium oxide), equivalent to 19,838 metric tonnes of uranium (tU). The majority of uranium deliveries to the US came from international sources, including Canada, Australia, Kazakhstan, Russia, and Uzbekistan.

Uranium and The Quest for Securing Power Supplies

About 85% of the uranium purchases were made under long-term contracts, with a weighted average price of $42.42 per pound U3O8. The remaining 15% was acquired through spot contracts, at a higher weighted-average price of $51.64 per pound U3O8.

Commercial US inventories of uranium saw a year-on-year increase. It reached 152 million pounds U3O8 by the end of 2023, marking a 6% rise from the previous year.

These inventories include uranium in various stages of the nuclear fuel cycle, including material owned by brokers, converters, enrichers, fabricators, producers, traders, as well as plant owners and operators.

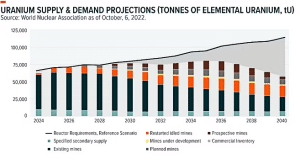

Looking ahead, the EIA forecasts a potential maximum demand of 433 million pounds of U3O8 over the next decade. This is based on existing contracts and unfilled market requirements from 2024 to 2033.

These findings highlight the US nuclear industry’s ongoing reliance on global uranium markets, with significant implications for energy security and international trade dynamics in the nuclear sector.

Kazatomprom, the world’s leading uranium producer, accounting for 40% of U3O8 supply, has not announced further production downgrades. But the company warns of limited sulphuric acid supplies affecting its targets.

Major producers like Cameco also predict supply deficits. Kazatomprom forecasts a shortfall of 21 million pounds by 2030, rising to 147 million pounds by 2040. Data from the World Nuclear Association shows a growing demand with limited supply, creating a significant gap.

Geopolitical factors complicate the outlook, such as the U.S. Senate reviewing a bill to ban enriched Russian uranium imports.

In response to the uncertain nuclear fuel future, countries are securing power supplies. Sweden plans to lift its uranium mining ban, holding 80% of the EU’s uranium deposits, and the Australian Chamber of Commerce and Industry urges reconsideration of its uranium ban.

As the demand for nuclear power remains stable, ensuring a diversified supply chain will be crucial for meeting future energy needs while navigating geopolitical uncertainties.

- SEE MORE: The Atomic Awakening… Fueled by Uranium