Global electricity demand is entering a decisive growth phase. IEA’s 2026 electricity report forecasts that over the next five years, power consumption is set to rise faster than at any time in recent decades, marking a structural shift in how the world uses energy. This trend reflects the rapid electrification of industries, transport, buildings, and digital infrastructure, alongside climate-driven demand for cooling and heating.

Unlike previous cycles, electricity demand is no longer simply following economic growth. Instead, power consumption is becoming a leading driver of economic activity. This shift signals the arrival of what analysts increasingly call the “Age of Electricity,” where power is the backbone of modern economies and decarbonization strategies.

Let’s deep dive into IEA’s report here to understand the present and the future of electricity demand.

Electricity Demand Breaks Away from Economic Growth

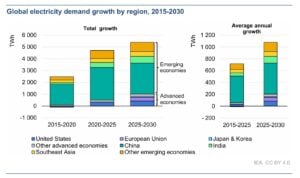

Global electricity demand is projected to grow at an average annual rate of around 3.6% between 2026 and 2030, significantly faster than the growth seen over the past decade. In contrast, total energy demand will rise much more slowly, meaning electricity will expand at least 2.5 times faster than overall energy consumption.

This divergence marks a fundamental change. Historically, electricity consumption closely tracked GDP growth. That relationship is now reversing. In 2024, electricity demand outpaced economic growth globally for the first time in three decades outside of crisis periods, and this trend is expected to continue.

Several structural drivers are accelerating this shift:

- Electrification of transport, especially electric vehicles

- Expansion of data centres and artificial intelligence workloads

- Rising demand for air conditioning due to climate change

- Industrial electrification and reshoring

- Growth in heat pumps and electric heating

Together, these trends are pushing electricity to become the dominant form of final energy consumption.

Emerging economies will remain the main engine of demand growth, accounting for roughly 80% of new electricity consumption through 2030. However, advanced economies are also seeing a resurgence after more than a decade of stagnation, driven by digitalization and electrification.

Global Power Mix: Renewables and Nuclear Take Half the Market

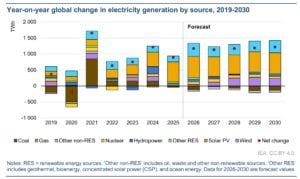

Globally, renewables and nuclear are on track to supply around 50% of electricity generation by 2030. Solar is the fastest-growing source, contributing more than half of annual generation additions.

Renewable generation is expected to grow by about 1,000 TWh per year through 2030, with solar alone adding more than 600 TWh annually. Nuclear power is also gaining momentum, supported by reactor restarts, lifetime extensions, and new builds in emerging economies.

However, coal will likely remain the single largest source of electricity in 2030, even as its share declines. Natural gas generation is also expected to rise, driven by US demand and fuel switching in the Middle East.

Overall, renewables, nuclear, and gas are projected to meet all net new electricity demand globally, displacing coal in aggregate but not eliminating it.

Advanced Economies Re-Enter the Demand Growth Cycle

Electricity demand in advanced economies is rising again after a prolonged period of stagnation. In the United States, demand is projected to grow by around 2% annually through 2030, with data centres accounting for roughly half of the increase.

In the European Union, electricity demand is expected to grow at around 2% per year, though consumption may not return to pre-2021 levels until the late 2020s. Other advanced economies, including Japan, Canada, Korea, and Australia, are also seeing accelerating growth.

This resurgence reflects:

- AI and cloud computing expansion

- Electrification of heating and transport

- Industrial reshoring and new manufacturing facilities

- Climate-driven cooling demand

Electricity is becoming a core input for economic competitiveness in digital and industrial sectors.

Power Sector Emissions: Plateau but Not Yet Declining Fast Enough

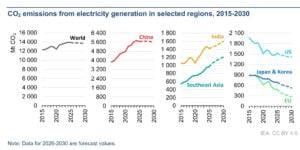

Electricity generation remains the largest source of energy-related carbon dioxide emissions, producing roughly 13.9 billion tonnes of CO₂ per year. After rising between 2022 and 2024, power sector emissions stabilised in 2025.

Looking ahead, emissions are expected to plateau through 2030, rather than decline sharply. This reflects the rapid growth in electricity demand, offsetting gains from clean power deployment.

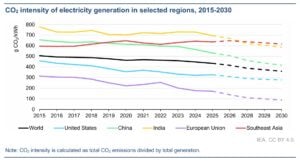

The carbon intensity of electricity has already fallen by around 14% over the past decade, and it is expected to decline faster as low-emission generation expands. This decline is mainly due to more renewable energy and strong nuclear power output.

- The trend is expected to accelerate. CO₂ intensity is forecast to fall by around 3.7% per year, dropping from 435 g CO₂ per kWh in 2025 to about 360 g CO₂ per kWh by 2030.

However, absolute emissions reductions will be harder to achieve due to rising demand. China’s trajectory is particularly critical. As the world’s largest power market and emitter, its pace of renewable deployment, coal retirement, and grid reform will heavily influence global climate outcomes.

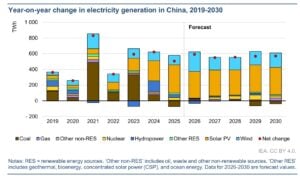

China: The Single Largest Driver of Global Electricity Growth

China will remain the central force shaping global electricity demand over the next decade. Despite slower economic growth and structural shifts toward services, China’s sheer scale means it will contribute close to half of global electricity demand growth through 2030.

Electricity demand in China rose by just over 5% in 2025, down from roughly 7% in 2024. Looking ahead, demand is expected to grow at an average of around 4.9% annually between 2026 and 2030, slower than the past decade but still massive in absolute terms.

The drivers are multifaceted:

- Continued electrification across industry and households

- Expansion of manufacturing, including clean energy supply chains

- Growing services sector electricity use

- Rising cooling demand due to extreme heat events

- Digital infrastructure and smart technologies

China’s power demand growth over the next five years alone is expected to match the current total electricity consumption of the European Union. This highlights the scale of China’s influence on global power markets, fuel demand, and emissions trajectories.

At the same time, efficiency improvements are tempering demand growth. Government policies targeting lower energy intensity and more efficient appliances are helping reduce electricity use per unit of GDP. However, these gains are not enough to offset the scale of electrification and economic activity.

MUST READ:

- China Adds Power 8x More Than the US in 2025, with $500B Energy Build-Out in a Single Year

- How China’s $180B Clean-Tech Investments Transform the Global South

Renewables Surge, But Grid Constraints Loom Large

China’s renewable energy buildout continues at an unprecedented pace. Solar generation jumped by more than 40% in 2025, while wind grew by double digits. The share of variable renewable energy (VRE) in China’s power mix reached around 22%, up sharply from the previous year.

Record capacity additions are transforming the power system. More than 300 GW of solar and over 100 GW of wind were added in a single year, driven partly by developers rushing to complete projects before the end of fixed-price tariffs.

However, this rapid expansion is creating new challenges. Curtailment rates for solar and wind increased, reflecting grid congestion and integration constraints. This highlights a global issue: generation is growing faster than grid infrastructure.

Coal’s Role Is Changing, Not Disappearing

Despite the renewable boom, coal remains a dominant force in China’s power sector. Coal-fired generation declined slightly in 2025, but coal still accounts for the largest share of electricity generation.

China’s coal share is expected to fall from around 55% in 2025 to about 43% by 2030, reflecting the rapid expansion of renewables and nuclear. However, coal capacity continues to grow, driven by projects approved during the 2022–2023 permitting boom.

Rather than serving as baseload power, coal plants are increasingly being used as flexibility and backup resources to support variable renewables. Capacity utilisation is expected to decline, even as installed capacity rises.

This shift illustrates a broader global trend: coal is becoming a reliability asset rather than a growth engine, but its persistence complicates decarbonization efforts.

Grids and Flexibility: The Hidden Bottleneck

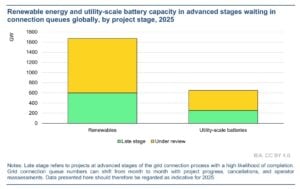

The transition to an electricity-centric energy system depends on grid expansion and flexibility. Investment in grids currently lags far behind generation capacity additions. Worldwide, more than 2,500 GW of projects are stuck in grid connection queues, including renewables, storage, and large industrial loads such as data centres. Without faster grid expansion and smarter system management, power shortages and curtailment risks will rise.

Meeting projected demand will require around 50% higher annual grid investment by 2030, rising from roughly USD 400 billion today. Without this, congestion, curtailment, and reliability risks will increase.

Flexibility solutions are also scaling rapidly. Utility-scale battery deployment is accelerating, especially in regions with high solar and wind penetration. However, conventional power plants still provide most flexibility today.

Policy reforms, grid-enhancing technologies, and non-firm connection agreements could unlock 1,200–1,600 GW of stalled projects, significantly accelerating the transition.

The Global Outlook: A Power-Centric Energy System

The global energy system is undergoing a structural transformation. Electricity is becoming the dominant vector for economic growth, digitalization, and decarbonization. Demand growth is accelerating across emerging and advanced economies, with China playing the most decisive role.

Renewables and nuclear are rapidly expanding, but coal and gas will remain part of the mix for reliability. Emissions are stabilising but not falling fast enough to meet climate targets, highlighting the scale of the challenge ahead.

The next five years will be critical. Grid expansion, flexibility solutions, and policy reforms will determine whether the Age of Electricity delivers a clean, affordable, and resilient energy future—or locks in new infrastructure bottlenecks and emissions risks.