According to a new analysis by Calyx Global, a carbon credit ratings platform, the quality in the voluntary carbon market (VCM) shows promising signs of improved integrity. The report combines market trend data with Calyx Global’s ratings of over 500 projects to offer insights into the ongoing efforts to enhance carbon market integrity.

Finding higher-rated carbon credits in the VCM remains challenging due to the dominance of mega-projects, such as REDD (Reducing Emissions from Deforestation and Forest Degradation) and large-scale grid-connected renewable energy projects, which typically do not achieve higher ratings (A and B).

Calyx Global’s co-founder, Donna Lee, emphasizes the need for higher-quality carbon credits to restore confidence in the market.

“We wanted to start tracking quality, recognizing that the voluntary carbon market is starting to mature. The quicker we improve carbon credit quality and restore confidence, the more effective companies can be at addressing climate change.”

The report, “The State of Quality in the Voluntary Carbon Market”, identifies major trends and below are the key findings.

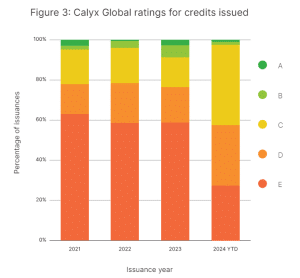

Decrease in Low-Quality Carbon Credits Issued

Since 2021, media scrutiny over the voluntary carbon market has intensified, coinciding with a rise in carbon credit issuances. Both market volume and media criticism peaked in 2023. However, there has been a notable shift in the quality of credit issuances, especially from the beginning of 2024.

Quality in the VCM highly varies, with both poor-quality and high-quality credits in every sector analyzed by Calyx Global. To date, projects in the Manufacturing and Industry sector has the highest GHG integrity.

According to the analysis, which has rated over half of all credits issued in the past 5 years, only about 20% of these credits fall into the top half of their rating scale (C+ and above).

Notably, less than 10% of the rated credits received a B rating or higher. This highlights the difficulty in sourcing high-integrity carbon credits in the current market landscape.

The issuance of low-rated credits (E-rated) has significantly declined, dropping by nearly 50%. This decrease is primarily due to a reduction in credits issued from REDD+ projects. These credits have historically been skewed towards lower ratings.

The decline in REDD+ credits has been partially offset by an increase in issuances from household and community projects, such as cookstove credits. These projects tend to have more credits in the “C” rating range.

Despite the overall improvement in credit quality, high-rated credits (A and B ratings) remain rare. This rarity is due to the smaller number of such projects actively issuing credits in the market today. Additionally, these higher-rated projects tend to be smaller in scale compared to mega-projects like REDD and large-scale renewable energy projects.

Slow Adoption of Quality Updates

Despite recent shifts towards higher quality in the VCM, a clear and consistent trend has yet to emerge.

Over 75% of new listings on major registries—American Carbon Registry (ACR), Climate Action Reserve (CAR), Gold Standard, and Verified Carbon Standard (VCS)—come from the Forest & Land and Household & Community sectors. These sectors show mixed results in Calyx Global’s rating system.

The Forest & Land sector is dominated by improved forest management (IFM) and afforestation/reforestation (AR) projects, which are undergoing methodological changes aimed at enhancing their effectiveness and integrity.

In the Household & Community sector, cookstove projects make up the majority of new listings. And efforts are underway to refine cookstove methodologies to improve their quality and impact.

It may take time for low-quality credits to be completely phased out of the system. Some low-quality credits are still tied up in forward contracts, delaying the full impact of improved quality standards. Although there have been improvements in the rules and requirements for generating carbon credits, these updates still need to be fully integrated into the active market.

A Tradeoff: GHG Integrity vs. SDG Impact

While buyers are attracted to benefits “beyond carbon,” such as social and environmental co-benefits, the primary driver of market trends is the search for higher greenhouse gas (GHG) integrity.

Around 54% of rated projects for GHG integrity have Sustainable Development Goals (SDG) contributions verified by a third party. This trend is especially prevalent among nature-based projects, which often seek additional SDG certification through programs like Verra’s Climate, Community, and Biodiversity (CCB) Standards and the Sustainable Development Verified Impact Standard (SD VISta), resulting in verified SDG contributions.

- READ MORE: Carbon Credits and the Sustainable Development Goals: Aligning Climate Action with Global Priorities

In contrast, waste and renewable energy projects frequently don’t pursue extra SDG certification. Or they are registered under programs that don’t require SDG claims to be verified.

Some argue that the ideal carbon credit should possess both high GHG integrity and significant SDG impact. However, such credits are currently challenging to find, per Calyx Global findings. There appears to be a tradeoff between GHG integrity and SDG impact in the current market.

This tradeoff is partly because many projects that deliver the highest SDG impacts, such as REDD+ and cookstove projects, have issues with over-crediting.

Household-based projects often have verified SDG contributions, largely because of the Gold Standard‘s requirement to report, monitor, and verify at least three SDGs per project. Verra has now introduced a similar requirement.

Calyx Global concludes that the VCM continues to evolve and is moving towards version 2.0. This analysis is crucial for instilling trust in carbon credits and enable them to effectively contribute to climate change mitigation.