National Atomic Company Kazatomprom JSC, the world’s largest uranium producer, has moved closer to sealing a massive long-term supply deal with India. The Kazakh state miner announced that it plans to sell a significant portion of its natural uranium concentrates to India’s Department of Atomic Energy (DAE).

However, the transaction is so large that it requires shareholder approval under Kazakhstan’s Joint Stock Companies law. As a result, the company has called an Extraordinary General Meeting (EGM) at the initiative of its Board of Directors.

If approved, the agreement could tighten an already strained global uranium market.

A Deal That Could Reshape Uranium Supply

The proposed contract signed with the Directorate of Purchase & Stores (DPS) under India’s DAE, covers the long-term sale of natural uranium concentrates (U₃O₈) for physical delivery to India.

The value of the transaction equals or exceeds 50% of Kazatomprom’s total book asset value. Under Kazakh law, such a major transaction must go before shareholders for approval.

While pricing, volumes, and delivery schedules remain confidential due to commercial sensitivity, the scale alone signals its strategic weight.

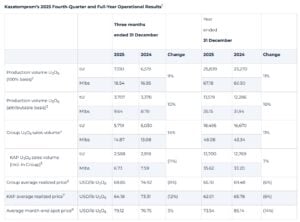

Kazatomprom’s Q4 2025 Fourth-Quarter Uranium Output

Kazatomprom currently accounts for about 20% of global uranium production. In 2025, it produced 25,839 tonnes of uranium (around 67.2 million pounds U₃O₈) on a 100% basis. That marked a 10–11% increase from 2024, driven largely by ramp-up at JV Budenovskoye.

- Meanwhile, spot transactions increased sharply. Spot volumes rose 50% year-over-year to 55.3 million pounds U₃O₈ (around 21,270 tonnes), with an average price of $72.75 per pound.

- Group sales volumes reached 5,719 tonnes (14.87 million pounds U₃O₈), up 14% from the previous year.

At the same time, global uranium mine production for 2025 was projected at 62.2 kilotonnes (ktU), according to industry estimates. Reactor demand stands higher at 68.9 ktU. This gap highlights a persistent supply deficit. Therefore, removing a sizeable share of Kazakh output under long-term contracts with India could tighten spot availability even further.

Fueling India’s Nuclear Ambitions: Why Uranium Imports Matter

India’s nuclear expansion explains the urgency behind this deal.

The country’s domestic uranium production currently meets only about 36% of its needs. Between 2025 and 2033, imports were projected to reach roughly 9,000 tonnes of uranium (tU) to support new reactor capacity.

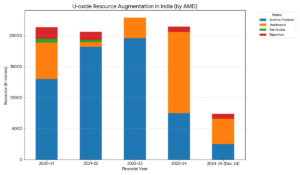

India holds recoverable reserves estimated at 252,500 tU below $260/kgU. In addition, the Atomic Minerals Directorate for Exploration and Research (AMD), a unit of the Department of Atomic Energy, has identified 433,800 tonnes of in-situ U₃O₈ resources across 47 deposits in states including Andhra Pradesh, Jharkhand, Rajasthan, and Telangana.

Mining at Jaduguda began in 1967 under Uranium Corporation of India Limited (UCIL). Recently, AMD discovered 26,437 tonnes of additional in-situ uranium oxide resources at the Jaduguda North–Baglasai–Mechua deposit in Jharkhand. This discovery is expected to extend the mine’s life significantly.

Still, domestic output alone cannot support India’s long-term reactor fleet expansion. Hence, securing a stable overseas supply has become a strategic priority.

The DPS, which handles procurement and inventory for India’s nuclear industry, accepted Kazatomprom’s commercial offer within its validity period. That move now awaits shareholder approval in Kazakhstan.

Uranium Supply in a Shifting Geopolitical Landscape

The uranium market remains highly concentrated in 2025, and this proposed deal reflects a broader shift in global nuclear geopolitics.

- Looking ahead, Kazatomprom’s 2026 production guidance stands at 27,500–29,000 tonnes on a 100% basis, slightly below nominal capacity due to sulphuric acid supply constraints. Group sales are expected at 19,500–20,500 tonnes.

If the India contract absorbs a major portion of future output, the free market could feel the impact quickly, especially given the structural supply gap.

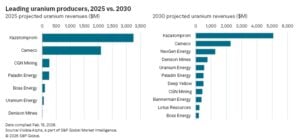

Reports say that by 2050, Kazakhstan and Canada are expected to dominate uranium exports. And in this market, uranium giants like Kazatomprom and Canada’s Cameco Corp. will dominate global revenue and production. Yet pricing trends have shown volatility. As demand for nuclear energy grows, countries are likely to form tighter supply alliances to secure fuel.

Balancing Strategy and Market Risk

At present, we can perceive that political tensions and energy security concerns are reshaping trade routes in oil and gas. And uranium may follow a similar path. Significantly, the IAEA has repeatedly noted that primary mining will remain the main source of uranium supply. Secondary sources, such as stockpiles and recycled materials, can only play a limited role.

Therefore, policymakers must rethink production and export strategies. Uranium-rich nations may reassess how much supply they allocate to long-term bilateral deals versus the open market.

For importing nations like India, long-term contracts provide stability. They reduce exposure to spot price volatility. They also strengthen diplomatic and economic ties. However, for the broader market, such agreements may reduce liquidity and amplify price swings during supply shocks.