The lithium market is at the center of the energy transition, driven by the soaring demand for electric vehicles (EVs). However, the journey to meet this demand is fraught with challenges. This article explores the future of lithium supply, demand, and price trends, highlighting critical investment needs and market dynamics.

The Great Raw Material Disconnect: Why Lithium Supply Trails EV Demand

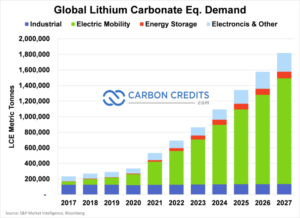

Forecasts indicate a looming lithium deficit that could significantly impact the EV market. Per Benchmark, the lithium market could face a shortfall of 572,000 tonnes by 2034—7x larger than current surpluses.

- While over one million tonnes of mined lithium are expected in 2024, this output must grow to 2.7 million tonnes by 2030 to meet rising demand, particularly from the EV sector.

The disparity between raw material supply and demand—termed the “great raw material disconnect”—is worsened by the lengthy timeline for developing lithium mines. Mines can take 5 to 25 years to become operational, while midstream and downstream facilities require less than five years. This misalignment presents a significant bottleneck for the battery industry.

Investment Needs

Benchmark analysis reveals a staggering $514 billion investment required by 2030 to meet battery demand. Of this, $220 billion will be for upstream projects while $51 billion must be invested in lithium production.

However, Western countries face higher costs and stricter environmental regulations compared to China, making investment a more complex challenge. Governments aiming to derisk supply chains from Chinese dominance may further inflate the required investment figure.

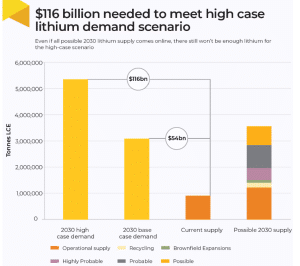

In another analysis, Benchmark estimated that the industry must secure $116 billion in investments by 2030 to meet EV targets. This “high case” scenario reflects growing EV adoption driven by government decarbonization policies and automaker commitments.

However, even with all planned lithium projects coming online, a 1.8-million-tonne shortfall remains. This speaks of the need for new mines, refineries, and expanded production. Automakers, aware of lithium’s critical role, are proactively investing upstream to secure supply.

General Motors and Tesla are making significant moves, with GM investing $650 million in Lithium Americas for its Nevada mine and Tesla building a $1 billion lithium refinery in Texas. Other players like BYD and CATL are establishing lithium facilities and joint ventures to boost production.

Automaker targets are ambitious: Tesla plans 20 million EVs annually by 2030, while General Motors and Mercedes-Benz aim for fully electric lineups by 2035 and 2030, respectively.

However, without accelerated lithium investments, these goals risk falling short, highlighting lithium as a bottleneck in the EV revolution.

Lithium Prices in Flux: Short-Term and Long-Term Outlook

Lithium prices have been subject to volatility, influenced by market dynamics and global supply-demand imbalances. Forecasting long-term prices is particularly challenging due to the lack of futures markets, with most trading occurring in spot markets.

Short-Term Price Trends

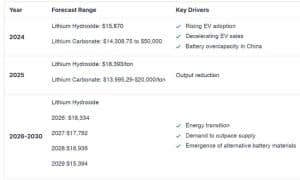

The Australian Government’s Office of the Chief Economist predicts a brief recovery for lithium hydroxide prices before a decline by 2026.

Medium- to Long-Term Price Outlook

In the medium term, analysts foresee lithium prices recovering to the marginal cost of production, estimated at $15,000–$20,000 per metric ton. Sustained structural deficits are expected to emerge, driving prices toward this range and potentially higher.

By the fourth quarter of 2024, some experts anticipate prices reaching the low $20s per kilogram. While prices may not revisit the highs of $40,000–$50,000 per tonne, a stable pricing environment is anticipated.

Market Adjustments and Structural Deficits

To balance the market, producers are implementing measures such as supply cuts, project delays, and stockpiling. Companies like Albemarle are reducing supply to address the current oversupply, while high-cost operations, such as Arcadium Lithium’s Mt. Cattlin project in Australia, are being placed into care and maintenance.

As prices stabilize and demand continues to grow, these structural deficits will likely drive further investment and price recovery. Moreover, strong demand will likely push the lithium prices higher in 2025 and beyond.

Navigating Risks and Opportunities in the Lithium Boom

The lithium market is exposed to risks, including volatile energy prices and geopolitical tensions. The reliance on lengthy mine development timelines poses a critical challenge, potentially delaying the supply chain’s ability to meet rising EV demand.

However, the market also offers substantial opportunities. Decarbonization efforts and the global shift to renewable energy sources are creating efficiencies and new markets for low-emissions products. Stable lithium prices and sustained investment could unlock significant growth potential for companies operating in the sector.

The lithium market is at a crossroads. On one hand, rising EV demand and decarbonization goals are driving unprecedented growth opportunities. On the other, supply chain challenges and volatile prices present significant hurdles. Addressing the “great raw material disconnect” through timely investment and strategic planning will be critical to meeting future demand.

Governments and other stakeholders must act decisively to bridge the gap between supply and demand, ensuring the lithium market can support the global energy transition.