Lithium has become one of the most critical resources for the global energy transition. As demand for electric vehicles (EVs) and renewable energy storage grows, countries are racing to secure stable supplies of this lightweight metal.

In the United States, the Department of Energy (DOE) has just announced a new era for lithium production. At the same time, investor interest in lithium has surged, reflected by the strong monthly close of the Global X Lithium & Battery Tech ETF (LIT). These changes show that the lithium market is reaching an important stage. This stage is shaped by policy, technology, and financial momentum.

U.S. DOE Takes a Stake in Lithium Americas

The DOE recently confirmed it will take equity stakes in Lithium Americas and its Thacker Pass mine in Nevada. This move marks the first time the U.S. government has directly invested in a lithium project rather than providing loans or guarantees.

Thacker Pass is one of the biggest lithium deposits in North America. It could greatly decrease U.S. dependence on foreign sources.

Becoming a shareholder sends a clear message: lithium production is vital for both business and national security. China controls over 60% of global lithium refining. So, the U.S. wants to boost its own supply chains.

The government aims to support projects that ensure long-term stability. The government’s role lowers risk for private investors. This could lead to more funding and partnerships.

Thacker Pass: America’s White Gold Standard

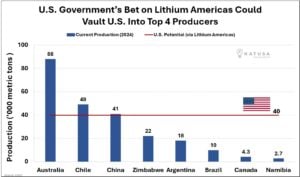

Thacker Pass, located in northern Nevada, is set to produce lithium carbonate. This will provide enough for batteries in up to one million EVs each year when fully operational. Construction is underway, and production is expected later this decade. The mine could make the U.S. one of the top four global producers, alongside Chile and Australia.

Thacker Pass has not been without controversy, facing environmental opposition and legal challenges. However, federal and state support has kept the project moving forward. If successful, it could reshape the balance of supply in the Western Hemisphere and reduce reliance on imports from Asia.

A Global Tug-of-War for Lithium Supply

While the U.S. builds its domestic base, other regions are also reconfiguring supply chains.

- Chile and Argentina hold about 60% of the world’s lithium reserves. They are rethinking their royalty rules and partnerships to bring in more foreign investment.

- Australia, currently the largest producer, continues to expand mining output but faces bottlenecks in refining. Much of its raw spodumene is shipped to China for processing.

- China, a leader in refining and cathode production, is boosting investments in Africa and South America. This helps it maintain its top position.

This global tug-of-war reflects a broader reality: lithium is not only an industrial commodity but also a strategic resource. Countries are ensuring access by using different methods. They invest directly, make long-term supply agreements, and innovate with technology.

EVs and Energy Storage: The Demand Engine

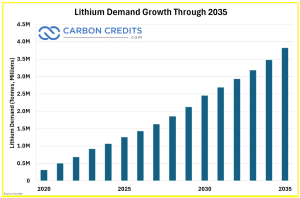

Lithium demand will likely surge in the next ten years. This rise is due to more people using EVs and increasing grid-scale energy storage. BloombergNEF forecasts lithium-ion battery demand reaching multiple terawatt-hours annually by 2035. EVs will likely make up over 70% of this total.

In the U.S., new federal incentives under the Inflation Reduction Act are pushing automakers to source more domestically produced materials. Ford, General Motors, and Tesla have all made deals for lithium. They expect the market to get tighter.

Meanwhile, utilities are using large battery storage systems. These help balance renewable energy from sources like wind and solar. This shift is increasing demand even more.

New Frontiers: Direct Extraction and Recycling

Meeting future demand will not only depend on mining new deposits but also on deploying new technologies. Direct lithium extraction (DLE) methods can boost recovery rates. They also lower environmental impact compared to old evaporation ponds. Companies in the U.S. and South America are piloting these systems, and if successful, DLE could accelerate supply growth.

Recycling also represents a growing opportunity. As the first wave of EV batteries reaches the end of life, recycling firms are stepping in to recover valuable metals. This secondary supply could become increasingly important in balancing markets and reducing dependence on mining.

Price Trends and Market Volatility

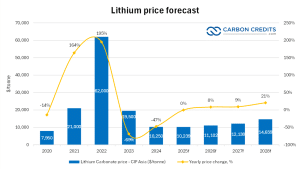

Lithium prices have seen dramatic swings in recent years. After hitting record highs in 2022, prices corrected in 2023 and 2024 as supply temporarily outpaced demand.

However, analysts warn that volatility is likely to persist. Benchmark Mineral Intelligence says lithium carbonate prices steadied in 2025. However, rising demand from EV makers could trigger another price surge in the late 2020s.

This volatility underscores the challenges for both producers and investors. Companies should balance long-term supply contracts with the risk of falling prices. Investors need to consider cyclical downturns alongside the bigger growth picture.

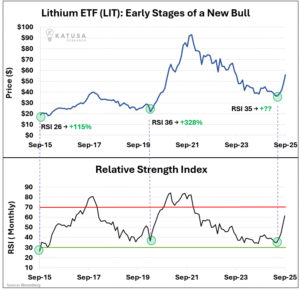

LIT ETF’s Rally Sparks Renewed Optimism

One sign of renewed optimism in the sector is the recent performance of the Global X Lithium & Battery Tech ETF (LIT). The ETF, which tracks a broad portfolio of lithium miners, battery producers, and EV companies, just posted its strongest monthly close in over a year, as seen in the Katusa Research chart below.

This performance reflects investor belief that the worst of the price downturn may be over and that long-term fundamentals remain intact. Stronger government backing, such as the DOE’s investment, adds further support to the outlook.

For many investors, ETFs like LIT offer diversified exposure to a sector known for both opportunity and volatility.

Investment Playbook: Choosing Exposure Wisely

For investors, the lithium sector presents both risks and rewards. On one hand, rising demand for EVs and energy storage supports a strong long-term growth story. On the other hand, price volatility, environmental concerns, and geopolitical risks remain significant.

Investors generally face three approaches:

- Major producers like Albemarle, SQM, and Ganfeng provide scale and stability.

- Emerging juniors, such as Lithium Americas, offer high growth potential but higher risks.

- ETFs like LIT provide diversified exposure, spreading risk across multiple companies and regions.

Each option carries different risk-reward profiles, making diversification a key strategy.

A Defining Decade for Lithium

The lithium industry is entering a transformative period. The DOE’s investment in Thacker Pass shows how vital it is to secure supply chains. Moreover, the strong close of the LIT ETF reflects rising investor confidence in this sector’s future. Globally, shifts in supply, demand, and technology are reshaping the landscape.

As EV adoption accelerates and renewable energy expands, lithium will remain a cornerstone of the energy transition. For governments, it is a matter of security and independence. For companies, it is a race to innovate and scale. And for investors, it represents both opportunity and volatility.

The next decade will likely define how lithium shapes the clean energy future, making today’s developments critical signals of what lies ahead.