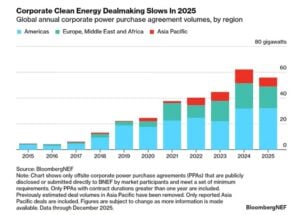

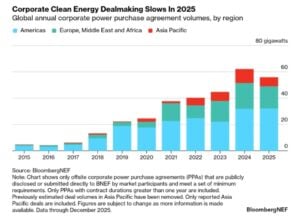

For nearly a decade, global companies have been racing to buy clean energy from wind farms, solar parks, and other green power projects. But 2025 marked the first decline in this trend in almost ten years — a surprising shift that signals a changing landscape for corporate sustainability.

The latest report from BloombergNEF (BNEF) shows that corporate clean energy purchasing dropped about 10% in 2025, falling from roughly 62.2 gigawatts (GW) in 2024 to 55.9 GW last year.

Let’s break down why this happened, what it means, and how the market could evolve in the coming years.

Clean Energy Buying: The Big Picture

Corporate clean energy buying usually happens through power purchase agreements (PPAs). They are long-term contracts where companies agree to buy electricity directly from renewable energy projects, often wind or solar farms.

For years, this was one of the fastest-growing parts of the clean energy market. Companies like Google, Amazon, Meta, and Microsoft drove most of the demand, helping build huge amounts of renewable capacity. But 2025 interrupted that streak.

Even though 55.9 GW is still one of the largest annual totals ever, the fact that it is lower than the year before shows a real shift in how companies approach renewable energy deals.

Why Corporate Clean Energy Buying Fell

There are several reasons why corporate clean energy buying slowed in 2025:

Corporate buyers are sensitive to electricity market rules and government policies. In many regions, uncertain policy environments made it harder to finalize long-term clean energy contracts. In the United States, for example, uncertainty about future clean energy incentives and carbon accounting standards caused many smaller corporations to hold off on signing new deals.

In some power markets, especially in parts of Europe, there were long hours of negative electricity prices. This happens when supply exceeds demand and power becomes so cheap that producers pay buyers to take it.

These price swings make standalone solar and wind contracts less attractive, especially for companies that want predictable, long-term value from their clean energy purchases.

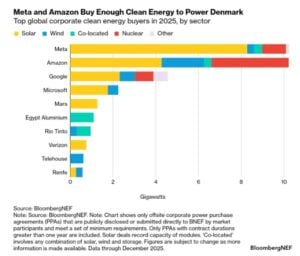

Dominance of Big Tech

Another key point in the BloombergNEF findings is that the market is becoming more concentrated. As said before, four major tech firms, like Meta, Amazon, Google, and Microsoft, signed nearly half of all clean energy deals in 2025.

Meta and Amazon alone contracted over 20 GW of clean power last year, including deals that cover not just solar or wind, but also nuclear power — something unusual in past corporate PPA markets.

While this heavy concentration helps maintain volume, it also means that smaller companies are scaling back, which lowers the total number of buyers and contributes to the overall slowdown.

- READ MORE: Clean Energy Investment Hits Record $2.3T in 2025 Says BloombergNEF: What Leads the Surge?

Regional Differences: Where Things Slowed and Where They Didn’t

Corporate clean energy markets didn’t all move in the same direction last year. Bloomberg’s data shows clear regional patterns:

United States

The U.S. remained the largest single market for corporate clean energy deals, signing a record 29.5 GW of commitments. Much of this came from major technology companies looking to match their growing electricity needs with zero-carbon power sources.

Yet despite these high numbers, the number of unique corporate buyers in the U.S. dropped by about 51%, as many smaller firms pulled back from signing new PPAs.

Europe, Middle East & Africa (EMEA)

In the EMEA region, corporate PPAs fell around 13% in 2025, slipping back to levels closer to 2023. In Europe, in particular, rising negative prices and unstable policy conditions discouraged many new deals.

Asia Pacific

Asia had a mixed story. Some markets like Japan and Malaysia continued to attract corporate clean energy buyers, thanks to mature PPA markets and supportive regulations. But slower activity in countries like India and South Korea contributed to a drop in total volumes in the region.

The Rise of Hybrid and Firm Power Deals

One interesting trend that emerged in 2025 is that companies are looking beyond just wind and solar. Because of the limitations with standalone renewable deals, many buyers are now exploring hybrid power contracts that mix renewables with storage, or even nuclear and geothermal sources.

Hybrid deals like solar paired with battery storage give companies more reliable power and help manage price and supply risks. BloombergNEF tracked nearly 6 GW of these hybrid agreements in 2025, and expects this share to grow.

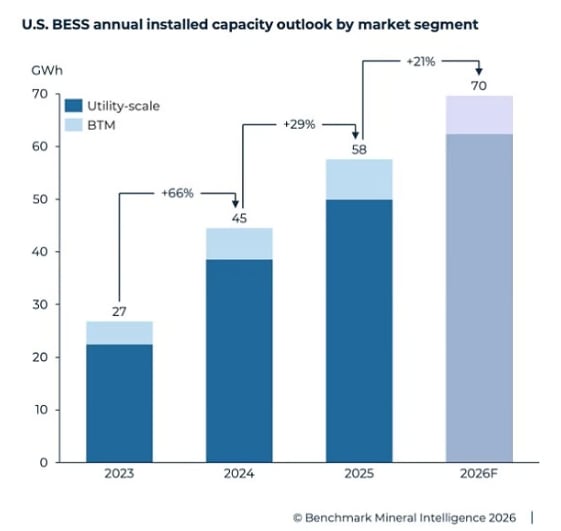

- According to a report by SEIA and Benchmark Mineral Intelligence, the United States added a record 28 gigawatts (GW) / 57 gigawatt-hours (GWh) of battery energy storage systems (BESS) in 2025. It reflected a 29% year-over-year increase.

Cheaper battery costs are part of this trend. Recent data shows that the cost of four-hour battery storage projects fell about 27% in 2025, reaching record lows. This makes storage-based renewable contracts more financially compelling.

Big Companies Still Push the Market

Even with the overall slowdown, corporate clean energy buying remains strong, especially among large technology firms.

In fact, while smaller companies took a step back, the major tech buyers helped keep total volumes near all-time highs. In other words, the market didn’t crash; it just shifted shape.

This becomes even clearer when we look at individual company progress. Microsoft reported recently that it now matches 100% of its global electricity use with renewable energy, an achievement that required decades of energy contracts and partnerships.

The Clean Energy Market Is Resetting, Not Retreating

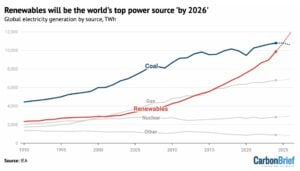

The IEA projects that renewables will provide 36% of global electricity in 2026. This shows that the energy transition is moving forward, even if corporate clean energy purchases dipped in 2025. The slowdown does not signal failure. Instead, it reflects a market that is adapting as companies, technologies, policies, and economics evolve together.

Growth in corporate renewable deals is not always steady. A single year of lower volumes does not erase the gains of the past decade. Instead, it highlights the natural adjustments markets go through as strategies shift and conditions change.

In this transitioning phase, policy and regulation remain critical. Clear rules, incentives, and supportive frameworks encourage smaller companies to participate. Additionally, regions that provide stability, such as parts of the Asia Pacific, are seeing continued growth in corporate clean energy demand.

In conclusion, even with the dip in 2025, corporate renewable energy purchasing is far larger than it was ten years ago. The market is shifting rather than shrinking, and companies continue to find ways to power growth with clean energy. This slowdown may serve as a wake-up call, encouraging smarter, more flexible strategies that can sustain the energy transition for years to come.