Disseminated on behalf of Alaska Energy Metals Corporation.

The global nickel market enters 2026 after a bruising and uneven year. In 2025, macroeconomic stress, trade disruptions, and deep supply imbalances reshaped pricing and sentiment. Although short-term rallies have returned, the underlying structure of the market remains fragile. As a result, 2026 is shaping up to be a year defined by volatility rather than a sustained recovery.

A Challenging Backdrop from 2025

To understand where nickel is headed, it helps to revisit the environment it emerged from. In 2025, global trade flows came under pressure after the US implemented new tariff policies. These measures disrupted supply chains and dampened confidence across industrial commodities. At the same time, global manufacturing growth slowed, weighing heavily on the broader nonferrous metals complex.

SMM reported highlighted some significant points. Adding to the uncertainty, the US Federal Reserve sent mixed signals throughout the year. Expectations around interest rate cuts shifted repeatedly. Each change altered risk appetite and triggered sharp moves across commodity markets. Nickel, already vulnerable due to oversupply, struggled to attract sustained buying interest.

China attempted to offset some of these pressures. Policymakers rolled out proactive fiscal measures and maintained a moderately accommodative monetary policy. They also focused on boosting domestic demand and diversifying export routes to reduce exposure to trade frictions. In July, China introduced its “anti-involution” policy, aimed at curbing destructive price competition across industries.

Even so, nickel underperformed. While other nonferrous metals showed mixed results, nickel remained constrained by a clear mismatch between supply and demand. Prices trended lower for most of the year. LME nickel opened near $15,365 per tonne and slid to lows around $13,865 per tonne, marking a sharp reset in the price center.

2026 Nickel Price Outlook: A Volatile Start to the New Cycle

Momentum shifted suddenly toward the end of the year. From mid-December, nickel prices began climbing rapidly.

- By early January, LME prices had surged past $18,000 per tonne, the first time in more than a year. In just 12 trading sessions, prices jumped nearly 20%, catching many traders off guard.

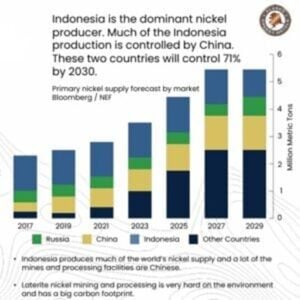

Several factors fueled this rebound. Demand signals from China improved modestly, particularly from stainless steel mills and EV battery producers. At the same time, speculative positioning adjusted as supply risks from Indonesia returned to the spotlight.

Trading Economics analysis stated that Indonesia, the world’s largest nickel producer, hinted at a potential 34% reduction in output for this year. Meanwhile, Vale temporarily halted operations at its Pomalaa and Bahodopi mines while waiting for regulatory approvals. Although its flagship Sorowako mine continued operating, these pauses added to market caution.

Still, the rally faced clear limits. Inventory levels remained elevated. Combined LME registered and off-warrant stocks jumped nearly 58% last year, reaching more than 367,000 tonnes. In addition, large shadow inventories in Singapore and Kaohsiung continued to hang over the market. As a result, every price spike met resistance.

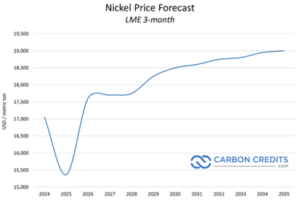

Price Expectations Remain Capped

Most analysts expect nickel prices to settle into a narrow band rather than trend sharply higher. Forecasts largely cluster between $15,000 and $16,000 per tonne. Several major institutions attribute the restrained outlook to ongoing surpluses.

- The World Bank’s 2026 nickel price outlook also revealed nickel prices to stay around US$15,500, rising to US$16,000 in 2027.

- Trading Economics data indicated that nickel futures moved back up to nearly $17,800 per tonne, reversing last week’s steep decline as buyers stepped back into the market.

Analysts consider that the differences in price forecasts primarily reflect contrasting views on how strictly Indonesia will enforce production limits and how quickly global manufacturing activity is expected to recover.

- CHECK: LIVE NICKEL PRICES

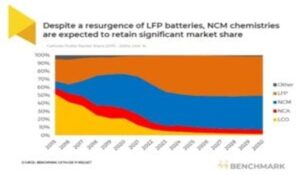

Nickel Demand Drivers Show Modest Growth

- Stainless steel: remains the dominant driver, accounting for about 70% of total demand. Consumption may rise to roughly 2.45 to 2.5 million tonnes. China’s production recovery offers support, while infrastructure projects in emerging markets add incremental demand. Still, no major surge is expected.

- Battery and EV application: They make up roughly 13% to 15% of demand. Nickel use in this segment could reach up to 500,000 tonnes. High-nickel cathodes continue to support premium EV models.

According to Benchmark Mineral Intelligence, demand for battery-grade nickel is expected to surge, tripling by 2030. This growth will largely be due to mid- and high-performance EVs in Western markets.

Other uses, including alloying, plating, aerospace, and electronics, provide steady but smaller contributions. A broader manufacturing recovery and net-zero investments could lift demand slightly, while faster EV adoption remains the main upside risk.

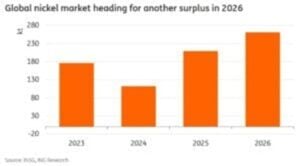

Supply-Demand Balance Stays Uneven

According to SMM, the nickel market will remain oversupplied through the year, remaining between 120,000 and 275,000 tonnes. While short-term rallies may continue, oversupply will remain the dominant force.

On the supply side, Indonesia’s refined nickel output stays high, supported by sunk investments and low operating costs. On the demand side, growth remains steady but unspectacular.

Ewa Manthey, a commodities strategist at London-Based ING Group, explained that the global nickel market is still set to remain oversupplied, with a projected surplus of about 261,000 metric tonnes. As a result, any production cuts would need to be deep and sustained to meaningfully shift market fundamentals.

China’s real estate support policies may provide limited relief for stainless steel consumption. However, a strong housing rebound appears unlikely, and any improvement is expected to be gradual. Similarly, demand from ternary batteries faces structural headwinds. Solid-state batteries remain years away from large-scale commercial use, and near-term battery chemistry trends do not favor a sharp jump in nickel intensity.

As a result, the average price level may drift lower over time. Tightening ore supply could briefly push prices above $16,000 per tonne. However, high inventories and excess capacity will take longer to absorb.

Why Nickel Matters for US Critical Mineral Independence?

Nickel plays a critical role in military-grade alloys, advanced weapons systems, electric vehicle batteries, grid-scale energy storage, and broader clean energy infrastructure. Despite its importance, the United States remains almost entirely dependent on imports for nickel, while China controls much of the global processing and supply chain. This reliance has become a clear strategic risk, one that domestic resources need more exploration.

And this is the reason America’s push to secure its critical mineral supply is gaining real momentum.

Spotlight: Alaska Energy Metals – America’s Nickel Backbone

At the center of this shift is Alaska Energy Metals Corporation (TSX-V: AEMC, OTCQB: AKEMF) and its Eureka deposit, the largest documented nickel resource in the United States. As Washington intensifies efforts to reshore critical supply chains for national security and clean energy goals, AEMC’s Nikolai Project in Alaska is steadily gaining recognition as a strategic domestic asset.

At the same time, the project aligns closely with the Trump administration’s executive orders focused on critical minerals and Alaska resource development. Those directives sought to speed up domestic production, curb reliance on foreign suppliers, and reinforce US security interests.

Against this backdrop, Nikolai stands out as a fully US-based “Sulphide nickel and battery metal project” to meet the country’s metal needs for the energy transition. Significantly, it has two claim blocks: Eureka and Canwell.

Eureka: The Largest Known Nickel Resource in the US

The Eureka deposit is not just large—it is nationally strategic. It hosts nickel alongside copper, cobalt, chromium, iron, and platinum group metals, including platinum and palladium. This metal mix makes Eureka highly relevant for both defense systems and the expanding clean energy economy.

According to the 2025 Mineral Resource Estimate, Eureka contains:

- Indicated Resource of 814 million tonnes grading 0.42% nickel equivalent, representing 5.62 billion pounds of nickel in situ.

- Inferred Resource of 896 million tonnes grading 0.39% nickel equivalent, totaling 9.38 billion pounds of nickel in situ.

Combined, the deposit contains more than 15 billion pounds of nickel, enough to support American demand for decades.

FAST-41 Listing Accelerates the Nikolai Project

A major step forward came when the Nikolai Project was accepted onto the FAST-41 Transparency Dashboard by the Federal Permitting Improvement Steering Council.

- The initial phase focuses on infrastructure upgrades, including rehabilitation and extension of the Rainy Creek Mining Trail, installation of temporary bridges, and development of an on-site camp.

These improvements will lower exploration costs, improve safety, enable better site access, and speed up the transition to advanced exploration and development at Eureka. Just as important, FAST-41 provides transparency, inter-agency coordination, and defined permitting milestones.

Key catalysts ahead

AEMC is entering a phase with several near- and mid-term value drivers. These include a first-pass metallurgical study to assess metal recovery, the potential for a major US Department of Defense grant, completion of a Preliminary Economic Assessment, and continued drilling at the Angliers target. Each step strengthens the investment and strategic case for Eureka.

Nickel Oversupply Overseas, Opportunity in the US

In summary, the nickel market faces another complex year. Structural oversupply, elevated inventories, and cautious demand growth define the landscape. Although policy shifts in Indonesia and short-term demand improvements can trigger sharp rallies, fundamentals continue to cap sustained upside. For now, nickel remains a market driven more by volatility than by balance.

As the US rebuilds its domestic critical mineral supply chain, assets like Eureka are becoming indispensable. With its scale, multi-metal profile, federal permitting support, and alignment with national policy priorities, Alaska Energy Metals Corporation is positioning itself as a key player in America’s push for resource security. In a world increasingly defined by competition for critical metals, Eureka has the potential to become the backbone of the US nickel supply for generations.

READ MORE: Nickel Demand to Triple by 2030: Can the Market Keep Up?