Rio Tinto delivered a mixed but resilient performance in the full-year 2025. While weaker iron ore prices weighed on profits, strong copper growth and disciplined cost control helped the mining giant keep earnings stable and maintain its dividend.

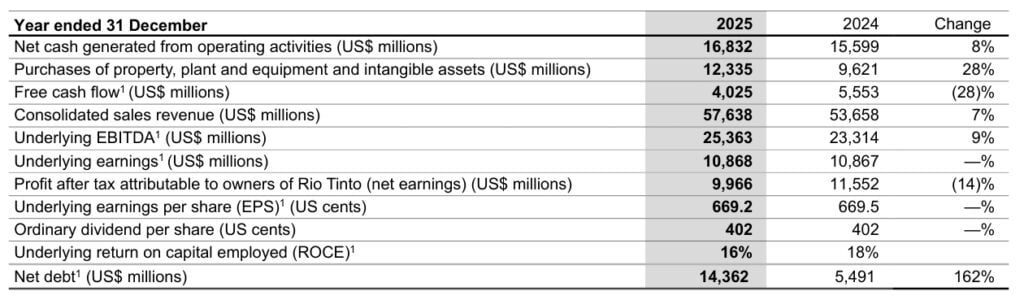

The world’s largest iron ore producer reported underlying earnings of $10.87 billion for the year ended December 31, unchanged from 2024. However, net profit fell 14% to $9.97 billion, compared to $11.55 billion a year earlier.

Despite the profit decline, Rio Tinto kept its shareholder payout steady. It declared an ordinary dividend of $6.5 billion, maintaining a 60% payout ratio. This marked the tenth straight year the company paid at the top end of its target range.

Iron Ore Softens, Copper and Aluminium Step Up

Lower iron ore prices hurt earnings. As the backbone of Rio Tinto’s business, iron ore remains critical. However, copper and aluminium delivered strong support.

Copper production rose 11% year over year. The key driver was the ramp-up of the Oyu Tolgoi underground project in Mongolia, where output surged 61%. This project is now complete and will play a major role in future copper growth.

Aluminium also performed well across the value chain. The company achieved record annual bauxite production of 62.4 million tonnes. As a result of higher volumes and better productivity, Rio Tinto reduced operating unit costs by 5% in real terms during 2025.

Operational cash flow strengthened. Net cash from operating activities rose 8% to $16.8 billion. Meanwhile, underlying EBITDA climbed 9% to $25.4 billion. These gains reflected operational discipline and tighter cost management.

Looking ahead, the company aims to deliver a 4% compound annual unit cost improvement through 2030. It also expects productivity initiatives to generate $650 million in annual benefits by early 2026.

Big Projects Drive Future Growth

Rio Tinto made significant progress across its global project pipeline in 2025. The major milestones are explained below:

Simandou Iron Ore Project

The Simandou project in Guinea reached a major milestone. The company shipped its first high-grade iron ore in December. This project is expected to strengthen long-term supply and improve product quality.

Pilbara Replacement Mines

In Western Australia’s Pilbara region, the Western Range replacement mine opened on time and on budget. Additionally, construction began at three more brownfield iron ore mines. Four of the five major replacement projects are now either ramping up or under construction.

Copper Expansion

The Oyu Tolgoi underground development is complete. Rio Tinto also achieved first production of Nuton copper at the Johnson Camp mine. The company remains on track to deliver 3% compound annual growth in copper-equivalent production through 2030.

Lithium Growth

In March, Rio Tinto closed its acquisition of Arcadium ahead of schedule. The focus now shifts to advancing lithium projects in Argentina and Canada. The company targets 200,000 tonnes per year of lithium carbonate equivalent capacity by 2028.

Together, these projects strengthen Rio Tinto’s position in future-facing commodities like copper and lithium, which are essential for electrification and the energy transition.

Strong Balance Sheet and Capital Discipline

Despite profits falling, Rio Tinto’s financial position remains solid. Its strong cash flow supports consistent dividends and future investment. The company plans to unlock between $5 billion and $10 billion from its asset base. It is currently reviewing options for its borates and titanium dioxide (TiO₂) businesses and considering infrastructure monetization.

Management also streamlined operations. It reduced its structure from four product groups to three core divisions, i.e., iron ore, aluminium & lithium, and copper

Additionally, the company reduced contractor numbers and discretionary spending. It also placed the Jadar project into care and maintenance and stopped non-core studies. These steps sharpened its focus on value-generating assets.

Climate Action: Progress with Challenges

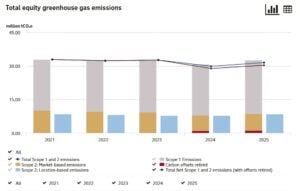

Sustainability remains an important part of Rio Tinto’s long-term strategy. The company spent $612 million on decarbonization initiatives in 2025, up from $589 million in 2024

In 2025:

- Gross Scope 1 and 2 emissions were 31.5 million tonnes of CO₂ equivalent, down 14% from the 2018 baseline of 36.7 million tonnes.

- Scope 3 emissions, which include customer use of products, reached 575.7 million tonnes of CO₂ equivalent. These emissions represent the largest share of its climate footprint. After applying high-quality carbon offsets, net emissions were 17% below baseline.

However, progress slowed compared to prior years. Emissions fell by just 0.2 million tonnes from 2024 levels. Increased production in iron ore and copper partly offset reductions.

Renewable Energy Contracts and Carbon Credits

The mining giant relies on renewable energy contracts and renewable diesel use, especially at its Kennecott site. It also retired about 1.01 million Australian Carbon Credit Units (ACCUs) to meet regulatory requirements.

Still, the path to its 2030 target of a 50% reduction in Scope 1 and 2 emissions depends on third-party renewable projects and successful commercial agreements. These factors remain outside the company’s direct control.

Around 7% of its electricity came from renewable sources, slightly lower than 78% in 2024 due to accounting adjustments in reported figures.

Environmental and Water Management

Air quality indicators such as NOx, SOx, and fluoride levels remained relatively stable over five years. However, PM10 levels increased slightly over the past three years. To reduce emissions at the source, Rio Tinto continues to upgrade equipment with best-available technologies. It also expands air monitoring networks around its operations.

Water management improved in 2025. Total operational water withdrawals declined to 1,147 gigalitres, down from 1,250 gigalitres in 2024. Freshwater withdrawals also fell slightly to 386 gigalitres.

Water recycling increased to 374 gigalitres, showing better reuse practices. Meanwhile, total water discharges dropped to 626 gigalitres.

The company advanced several community-focused water initiatives, including implementing a new water strategy at QIT Madagascar Minerals. It also increased transparency by publishing detailed water performance data.

The Bigger Picture

Overall, Rio Tinto delivered steady underlying earnings in a challenging pricing environment. Iron ore weakness pressured profits, yet copper and aluminium provided strong support.

At the same time, disciplined capital allocation, operational efficiency, and large-scale project execution strengthened its long-term outlook.

Looking forward, growth will rely heavily on copper and lithium. These metals sit at the heart of global electrification and decarbonization trends. If Rio Tinto delivers on its cost improvements and project milestones, margins and cash flow could improve further.

However, climate targets remain ambitious. Achieving deeper emissions cuts will require faster renewable energy deployment and broader collaboration across its value chain.

In short, 2025 showed resilience rather than rapid growth. Rio Tinto balanced shareholder returns, project expansion, and sustainability progress. Now, its future depends on executing its copper-led strategy while navigating commodity cycles and climate commitments.