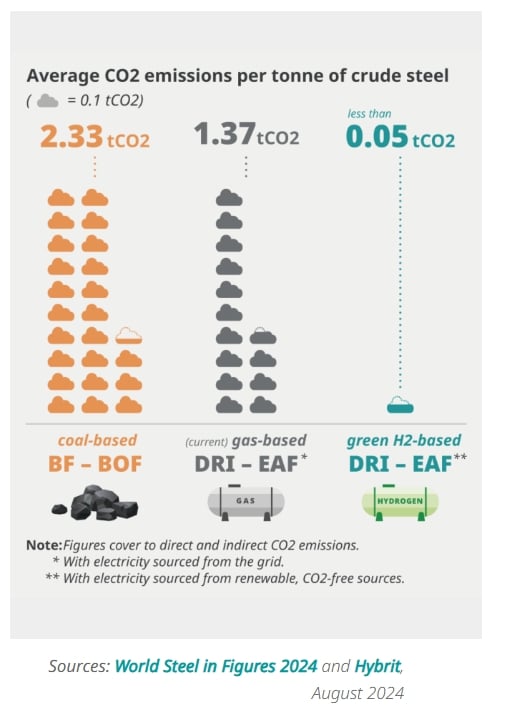

Steel is one of the most carbon-intensive materials on Earth, responsible for around 7% to 9% of global greenhouse gas emissions. The industry produces nearly two billion tonnes of crude steel annually, with average emissions ranging from 1.85 to 2.33 tonnes of CO2 for every tonne of steel. Despite being the backbone of infrastructure, renewable energy, and modern manufacturing, steel remains one of the hardest sectors to decarbonize.

Against this backdrop, ArcelorMittal, the world’s second-largest steelmaker, pledged in 2020 to slash emissions by 25% globally and 35% in Europe by 2030. It also announced a longer-term goal of reaching net zero by 2050. Yet, new findings suggest the company is falling behind, casting doubt on whether it will deliver on its climate promises.

Is ArcelorMittal Falling Short of 2030 Targets

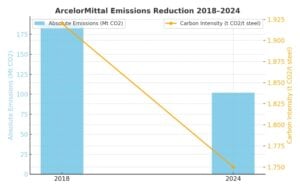

In 2023, ArcelorMittal’s average emissions intensity was 1.92 tonnes of CO2 per tonne of steel, only a slight improvement from 2018 levels.

Experts and analysts have figured out that the company’s 5.4% reduction in carbon intensity since 2018 pales compared to what is needed to align with a 1.5°C climate pathway.

SteelWatch’s report Backtracking on Climate Action analysed that to meet its own 2030 targets, ArcelorMittal would need to cut emissions by around 3% annually. Instead, its progress has been less than 1% per year.

Even though the company often highlights its 46% cut in absolute Scope 1 and 2 emissions since 2018. At first glance, this appears to be major progress.

But a closer look reveals that most of the decline came from producing less steel, not from genuine decarbonization. Between 2018 and 2024, ArcelorMittal’s crude steel output dropped 37%, while its production capacity fell 32%. Emissions went down largely because activity slowed, not because the steel itself became greener.

This distinction matters. Reducing emissions intensity—how much CO2 is released per tonne of steel—is the key indicator of sustainable progress. ArcelorMittal’s modest improvement in intensity shows its operations remain highly carbon-intensive.

Billions for Shareholders, Pennies for Climate

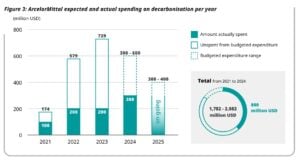

The same SteelWatch report further explained stark imbalances in ArcelorMittal’s spending priorities. Between 2021 and 2024, the company allocated just $800 million to decarbonization projects. That figure represents less than 2.5% of the $32.6 billion it generated in operating cash flow.

Meanwhile, the company rewarded shareholders with $12 billion in dividends and share buybacks during the same period—nearly 15 times what it spent on climate action. Of the $5 billion ArcelorMittal had resolved for its 2030 climate strategy, only 16% has been spent so far. This raises questions about whether climate commitments are truly central to its strategy, or simply secondary to financial returns.

Its joint venture in India, AM/NS, illustrates the scale of this omission. ArcelorMittal’s share of emissions from the venture exceeded 10 million tonnes of CO2 in 2024. By 2026, the JV’s total emissions are expected to surpass 25 million tonnes annually, yet none of these are reflected in ArcelorMittal’s targets.

Delayed and Stalled Green Steel Projects

Reports also indicate that the steel giant received more than $3.5 billion in public subsidies to develop five flagship Direct Reduced Iron (DRI) projects in Europe and Canada. These projects, intended to shift steel production away from coal-based blast furnaces, could significantly reduce emissions. However, by mid-2025, none had reached a final investment decision.

The much-publicized near-zero carbon steel plant in Sestao, Spain, is among those delayed. In contrast, competitors such as SSAB in Sweden and Salzgitter in Germany are moving forward with binding investments in fossil-free steel, placing them on track to align with Paris climate goals. ArcelorMittal’s slow pace highlights a widening gap between ambition and execution.

Shifting Language: “Economic Decarbonization”

ArcelorMittal executives now describe their approach as “economic” or “competitive decarbonization.” In practice, this means they will only pursue climate action when it makes business sense. Critics argue this signals retreat, showing the company prioritizes profit over planetary responsibility. By framing decarbonization as conditional on market conditions, the company risks delaying meaningful change until well past 2030.

ArcelorMittal Says, “Progress Is Real, Despite Challenges”

In November 2024, the company updated its European decarbonisation plans. The company noted that final investment decisions for new DRI-EAF (Direct Reduced Iron – Electric Arc Furnace) projects could not proceed.

Challenges include green hydrogen still being too costly, natural gas-based DRI not being competitive, and carbon capture infrastructure remaining in planning. These hurdles make achieving the 2030 emissions intensity target increasingly unlikely.

Significant Emissions Cuts Already Achieved!

Despite challenges, the company says, progress is real. Its sustainability report shows that in 2024, absolute Scope 1 and 2 emissions dropped to 102 million tonnes—46% lower than the 188 million tonnes recorded in 2018.

The sale of higher-carbon assets helped reduce the average carbon intensity to 1.75 tonnes of CO2 per tonne of crude steel, compared with the global average of 1.92. On a portfolio-adjusted basis, intensity has fallen 5.4% since 2018.

Over the same period, it invested $1 billion in decarbonisation initiatives. Efforts included:

- Transitioning to electric arc furnaces

- Increasing energy efficiency

- Sourcing clean energy

- Securing and diversifying metallic inputs

XCarb®: Meeting Growing Demand for Low-Carbon Steel

ArcelorMittal is responding to customer demand through XCarb®, launched in March 2021 as the world’s first low-carbon steel initiative. The offering includes:

-

XCarb® Steel Certificates – These reflect carbon savings from investments in cleaner steelmaking processes, such as capturing and reusing coke-oven gas or reducing coal use with natural gas. Customers can report Scope 3 emissions reductions alongside their steel purchases.

-

XCarb® Recycled and Renewably Produced (RRP) Steel – Physical steel made in electric arc furnaces powered entirely by renewable electricity, using high levels of recycled steel.

Sales of XCarb® doubled from 0.2 million tonnes in 2023 to 0.4 million tonnes in 2024. However, this is still a small fraction of total shipments (54.3 million tonnes in 2024), and only a limited number of customers are willing to pay a green premium. Regulatory mandates will be vital to scale adoption.

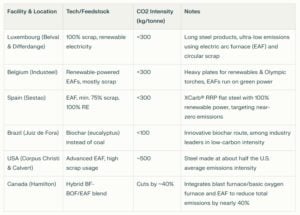

Bright Spots: Where ArcelorMittal Produces Low-Carbon Steel

Despite setbacks, ArcelorMittal does operate some lower-emission facilities:

These facilities show what is possible, but they represent only a fraction of ArcelorMittal’s global production. Scaling such operations remains the real challenge.

Steel Emissions and the Decarbonization Challenge

Over 70% of global steel is still made using coal-based blast furnaces, the most carbon-intensive method. Electric arc furnaces, which rely on scrap and electricity, account for about 28% and emit far less. To meet a 1.5°C pathway, the IEA says steel emissions must fall 50% by 2050, with near-zero technologies deployed at scale by 2030. ArcelorMittal’s global footprint makes its pace of decarbonization critical for the sector.

ArcelorMittal stresses that the steel sector cannot decarbonize alone. Steel is a low-margin, globally traded commodity, and cleaner methods remain uncompetitive without government support.

- Europe’s 2025 focus includes the Clean Industrial Deal, Steel and Metals Action Plan, CBAM review, and safeguard review. These aim to promote low-carbon steel demand, close CBAM loopholes, and tackle high energy costs.

Yet the company warns policies are still insufficient to level the playing field. Hydrogen-based steelmaking and carbon capture remain central to its strategy, but meaningful scale won’t arrive before 2030. Current efforts rely heavily on subsidies and future breakthroughs rather than near-term transformation.

Will ArcelorMittal Lead or Lag in Steel’s Net-Zero Future?

The steel giant has highlighted that emissions reductions and green steel projects come mostly from reduced output, not innovation. As investments lag behind shareholder payouts, major projects are delayed, and Scope 3 emissions remain largely uncounted. Initiatives like XCarb® show potential, but success depends on policy support, energy management, and market demand.

The steel industry is significantly tough to decarbonize, but vital for a net-zero world. With 2030 targets increasingly challenging, ArcelorMittal has cut emissions almost in half since 2018—but will it commit to real transformation this decade? The answer remains lost in the haze.