The US Department of Energy (DOE) has outlined its research and development (R&D) priorities to achieve the ambitious cost targets for clean hydrogen set by the Biden administration. Renewable hydrogen production and storage, as well as technology for trucking applications, are among the key focus areas identified by the DOE’s Hydrogen and Fuel Cell Technologies Office in its Multiyear Program Plan.

Sunita Satyapal, director of the said Office, stated in a forward to the program plan:

“While the progress in clean hydrogen today is encouraging, it is also clear that more is needed… and the actions taken must be well-planned, deliberate, carefully executed with measurable outcomes, and they must come without delay.”

DOE’s Clean Hydrogen Roadmap

The Inflation Reduction Act, enacted in August 2022, introduced tax credits of up to $3/kg for clean hydrogen producers over the initial decade of a project’s lifespan, depending on its carbon emissions lifecycle. This incentivizes clean or green hydrogen production, positioning it competitively against grey hydrogen from fossil fuels.

The U.S. leads in green hydrogen production due to these tax credits and a $9.5 billion subsidy from the Infrastructure Investment and Jobs Act. The subsidy includes $8 billion to establish at least 4 regional clean hydrogen hubs.

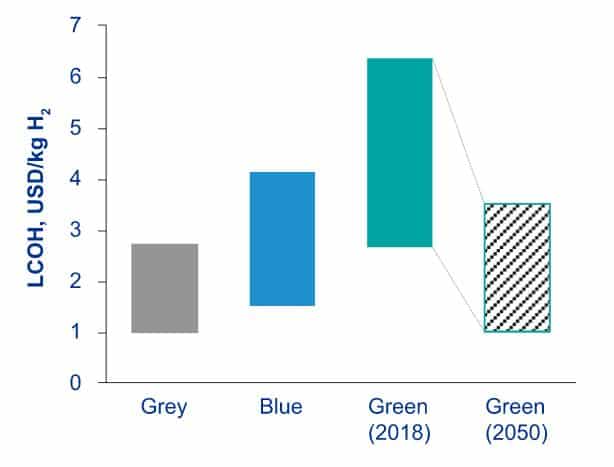

Projections anticipate the cost of green hydrogen to decrease significantly by 2050, signaling its long-term viability, and encouraging further investment.

The DOE aims to significantly reduce the cost of zero-emission hydrogen by targeting a price of $1/kilogram by 2031. This price includes production, delivery, and dispensation at fueling stations. An interim target of $2 per kilogram by 2026 has been set.

The agency’s plan centers around the DOE’s “Hydrogen Shot” objective. It also seeks to decrease the cost of electrolyzer systems to $250-500/kW, lower the cost of fuel cell systems for heavy-duty transportation to $80/kW, and achieve a final dispensed cost of hydrogen fuel below $7/kg.

Currently, hydrogen produced by electrolysis can cost at least $5 per kilogram, or up to $12 per kilogram when accounting for delivery and fueling station costs. Conventional hydrogen production from natural gas costs about $1.50 per kilogram but comes with a significant carbon footprint.

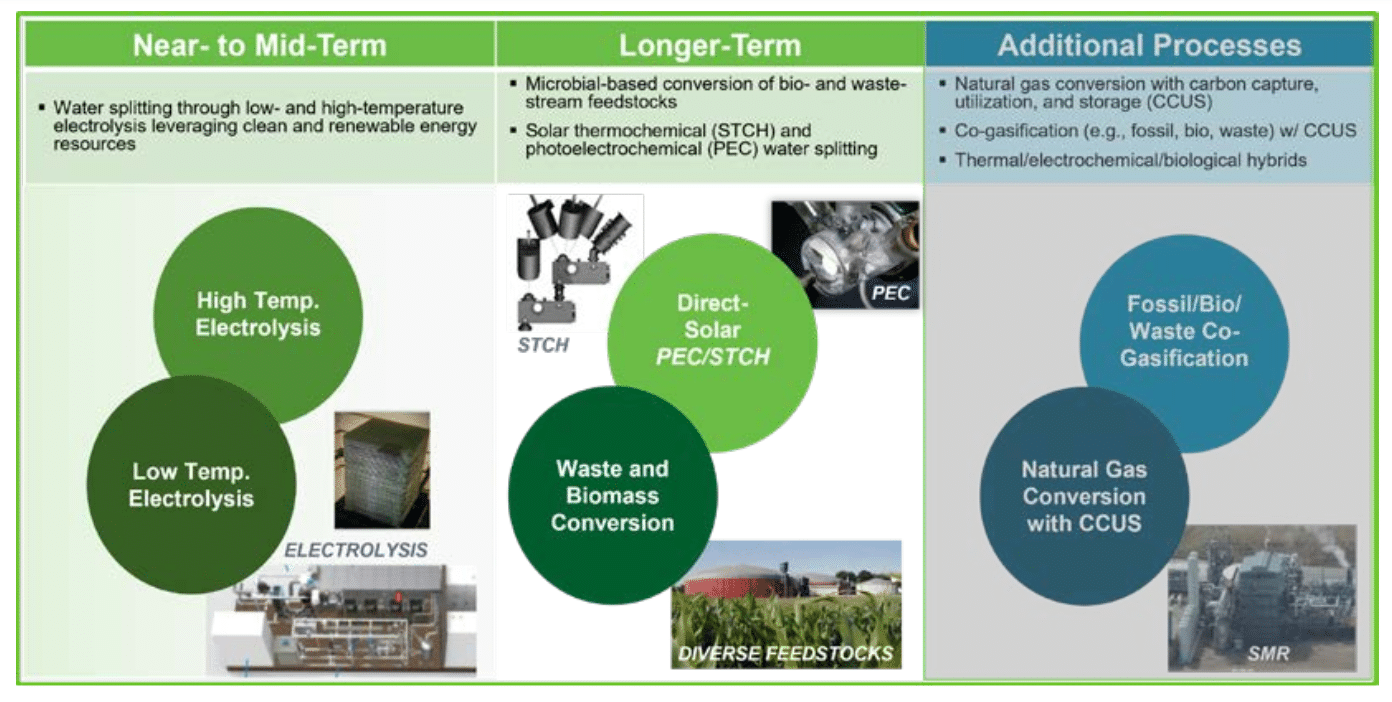

The near-term priorities outlined by the DOE include improving electrolyzer technology to achieve lower systemwide costs and increased durability. Additionally, research and development efforts will focus on hydrogen storage and transportation for heavy-duty vehicle applications, aiming to reduce costs and minimize leakage.

DOE Clean Hydrogen Production Pathways in the RD&D Portfolio

In the long term, the DOE sees opportunities in advanced hydrogen production methods that require minimal or no electricity input. These include solar photoelectrical chemical production and biological conversion. Materials-based hydrogen storage, utilizing absorbents or chemical carriers, is also a focus area for long-term research and development.

Toyota’s Renewable Hydrogen System

Over in California, FuelCell Energy and Toyota Motor North America recently celebrated the inauguration of the groundbreaking “Tri-gen” system at the Port of Long Beach. This innovative system uses biogas to generate renewable electricity, renewable hydrogen, and usable water.

The Tri-gen system was specifically constructed to support the vehicle processing and distribution center for Toyota at Long Beach. The facility is Toyota’s largest in North America, receiving about 200,000 new Toyota and Lexus vehicles annually.

The system showcases scalable hydrogen-based technology that reduces emissions and minimizes reliance on natural resources. Tri-gen’s fuel cell technology converts renewable biogas into electricity, hydrogen, and usable water with high efficiency and minimal pollution.

Moreover, Tri-gen produces up to 1,200 kg/day of hydrogen to fuel Toyota’s incoming light-duty fuel cell electric vehicle (FCEV) Mirai. It also supplies hydrogen to the adjacent heavy-duty hydrogen refueling station, supporting TLS logistics and drayage operations at the port.

California’s Advanced Clean Fleet Regulation mandates zero-emission trucks for newly registered drayage trucks. And Tri-gen is well-positioned to support the transition to zero-emission trucks, including FCEV Class 8 trucks. The system’s hydrogen production can be adjusted based on demand, facilitating the migration to zero-emission vehicles by 2035.

Generating 2.3 megawatts of renewable electricity, Tri-gen also supplies excess electricity to the local utility, Southern California Edison. As such, it will contribute to the renewable energy grid under the California Bioenergy Market Adjustment Tariff (BioMAT) program.

Pioneering Innovative Carbon Reduction Solutions

Overall, Tri-gen is expected to help reduce more than 9,000 tons of CO₂ emissions annually from the power grid. It can also avoid over 6 tons of grid nitrogen oxide emissions, while potentially reducing diesel consumption by 420,000 gallons/year. This aligns with both Toyota’s carbon reduction goals and the Port of Long Beach’s commitment to innovative CO2 reduction solutions.

In summary, the DOE’s plan underscores the importance of continued innovation and investment in clean hydrogen technologies to accelerate the transition toward a low-carbon economy.

The collaboration between FuelCell Energy and Toyota is an example of how innovative and sustainable solutions through hydrogen can help reduce carbon emissions in business operations while promoting renewable energy sources.