Base Carbon Inc., operating through its wholly-owned subsidiary Base Carbon Capital Partners Corp., announced the receipt of an initial transfer of 717,558 carbon credits from its Rwanda cookstoves project. These carbon credits, designated by Verra with an “Article 6 Authorized” label, mark a significant milestone for Base Carbon.

It signifies the transition of its second project from the development stage to active carbon credit generation. Notably, this also represents an industry milestone being the first Article 6 Authorized labeled carbon credits issued by Verra.

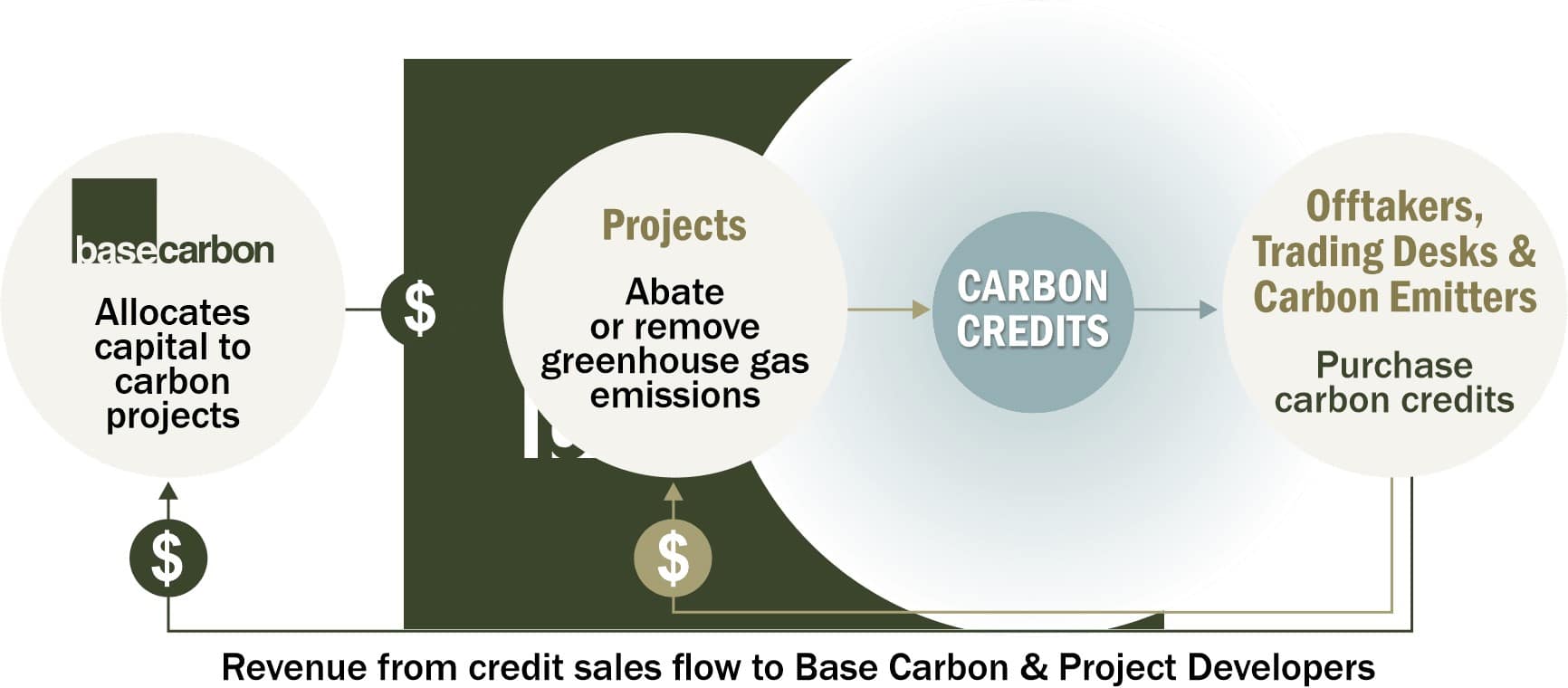

Base Carbon is a leading financier of projects in the global voluntary carbon markets. The company supports carbon removal and abatement projects worldwide by providing capital and management resources. It also aims to enhance efficiencies, commercial credibility, and trading transparency by leveraging technologies within the evolving environmental industries.

The company provides upfront capital to carbon projects, earning revenues from the credits they generate.

What is Article 6 Carbon Credit?

Article 6 of the Paris Agreement talks about how countries can work together and trade mitigation outcomes, also known as carbon credits, with each other to help meet their climate targets (NDCs).

In November last year, the Supervisory Body overseeing Article 6 of the Paris Agreement published a draft document detailing proposed methodologies for carbon reduction projects.

The methodologies help ensure a cautious approach in calculating a project’s emission reductions or removals. This is crucial for ensuring the credibility of the credits and promoting greater ambition in global emission reduction efforts.

Base Carbon Pioneers Article 6 Authorized Carbon Credits

The Rwanda cookstoves project received a letter of authorization (LOA) from the Government of Rwanda in December 2023. This leads to Verra applying its Article 6 Authorized label to the project.

This designation marks the first time Verra applied such recognition to a carbon project registered in its Verified Carbon Standard (VCS) Program.

BCCPC and the DelAgua Group, the project developer, have been in discussions regarding the implementation of the LOA. As per the LOA, a portion of the issued Article 6 Authorized labeled carbon credits will be immediately retired to offset global emissions.

Additionally, a percentage of the carbon credits will be transferred to the Government of Rwanda for its emission reduction targets. Then a portion of the revenues from the remaining credits will go to the United Nations’ Global Adaptation Fund.

The Clean Cooking Project is a voluntary initiative focused on distributing fuel-efficient improved cookstoves (ICS) to households. DelAgua will distribute these technologies to individual households and communities, following the VCS Methodology from Sectoral Scope 3 – VMR0006 “Methodology for Installation of High-Efficiency Firewood Cookstoves,” version 1.1 for emissions reduction calculations.

Before the project, households primarily used 3-stone fire and traditional stoves. These cookstoves have low thermal efficiency and require a higher amount of firewood for cooking.

By adopting DelAgua stoves, people can save time spent on cooking and collecting fuel, while also conserving fuel itself. The main benefit of these cookstoves is the significant reduction in health risks associated with smoke emitted by traditional stoves.

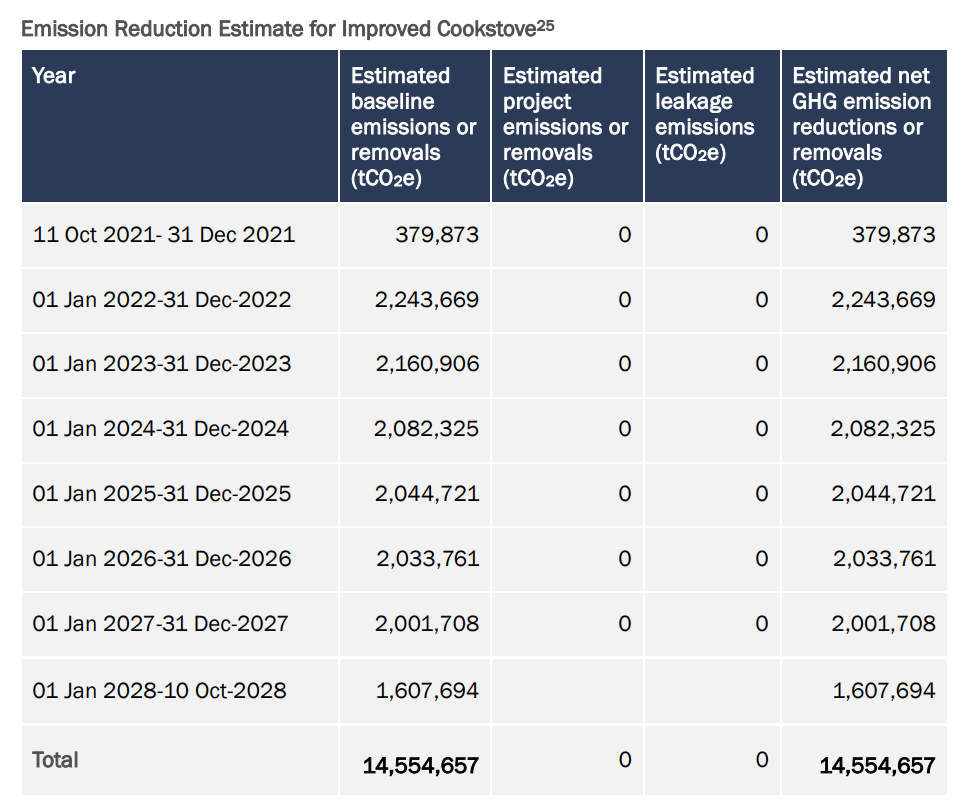

Plus, it also avoids the release of planet-warming emissions. The project is estimated to achieve an average annual and total emission reduction of 1,819,332 and 14,554,657 tCO2e, respectively, over the first 7-year crediting period.

More details can be found on Verra’s website under project ID 4150.

Enhancing Article 6 Carbon Credits Implementation for Greater Impact

BCCPC and DelAgua have recently signed an amended and restated project agreement to facilitate the implementation of the LOA.

Under their revised agreement, BCCPC and DelAgua will split the 5% GAF remittance attributable to Article 6 carbon credits sold. This would be based on each party’s pro rata share of sales proceeds outlined in a revenue-sharing arrangement.

- Base Carbon anticipates its GAF remittance to be around $0.20 per credit for the first 1,925,000 Article 6 Authorized labeled carbon credits received.

Under the revised agreement of BCCPC and DelAgua, Article 6 Authorized labeled carbon credits from the Rwanda cookstoves project will be adjusted for the 12% volume reduction specified in the Government of Rwanda LOA. Thus, a new aggregate minimum of 6.6 million carbon credits would be subject to BCCPC and DelAgua’s revenue-sharing arrangement.

Base Carbon is currently exploring various sales options for the initial 717,558 carbon credits. They expect the potential pricing upside of adjusted carbon credits will offset any volume reductions due to the LOA’s implementation.

Base Carbon’s receipt of the first-ever Article 6 Authorized carbon credits signifies a monumental leap in environmental stewardship. Through innovative financing and strategic partnerships, this milestone underscores the potential for carbon markets to facilitate meaningful change and pave the way for a greener, more sustainable future.

Source: OFFSEL.net

Source: OFFSEL.net