At the recent Carbon Markets Summit, research firm Sylvera along with Pachama convened a global assembly of thought leaders to delve into the present complexities and future potential of the carbon market.

This comprehensive guide, a collaborative effort between Sylvera and Pachama, sums up the ten most significant trends that these experts foresee shaping the carbon market landscape in 2023 and beyond.

One of the key areas where this is happening is in the carbon credit market. It is where accurate and in-depth ratings and analytics are essential for effective decision-making.

Click here to download your copy of the report.

Five Key Points from the Pachama and Sylvera Report

Delving into the report, five key points emerge that summarize the current state and future trajectory of this critical sector.

- Market in Flux: The voluntary carbon market is undergoing significant changes due to new climate disclosure regulations, guidance from market bodies, and increased media attention. This has caused some confusion and hesitation among potential buyers. Still, the need for carbon project funding is more critical than ever.

- Flight to Quality: Corporate buyers are participating in a ‘flight to quality‘. They are becoming involved earlier in projects and focusing on contribution over ‘offsetting’. This trend will continue in 2023 and beyond.

- Technology and High-Quality Projects: Technology is unlocking greater supplies of high-quality projects. Companies like Sylvera and Pachama are using data and artificial intelligence to help companies invest confidently in high-quality carbon credits.

- Carbon Credits – ‘Last, but not Later’: The mitigation hierarchy encourages emission reductions first and carbon credits last. However, ‘last’ does not have to mean ‘later’. Companies can purchase carbon credits throughout their decarbonization journeys, as long as these purchases do not replace actual emissions reductions across the value chain.

- Voluntary Carbon Market Growth: Despite challenges with legacy credits, limited high-quality supply, and ongoing work on official guidance, the corporate demand for carbon credits is strong. The voluntary carbon market is still growing, and the overall trajectory for the VCM looks positive.

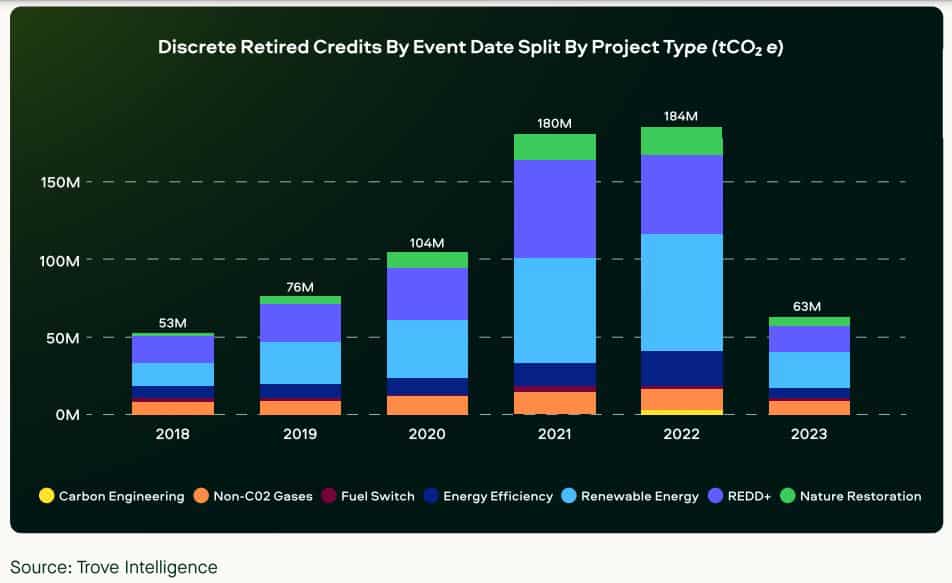

Voluntary credit retirements remained strong in 2022 at 184 million and are on track to beat records in 2023.

These insights paint a vivid picture of the market’s present dynamics and future potential. The report underscores the pivotal role of carbon credits in steering corporate strategies towards decarbonization.

It also champions the cause of investing in high-quality projects, a move that promises both environmental and economic dividends. It also highlights the ongoing growth and evolution of the voluntary carbon market.

A lot of insights on carbon market trend were shared during the summit, but here are the ones that are worth sharing.

3 Meaningful Insights That Stand Out…

1. “Companies leading on climate are demonstrating the difference between hierarchy and chronology: ‘last’ does not have to mean ‘later’.”

While carbon credits are often seen as the last step in a company’s decarbonization journey, they don’t have to be the final action taken. Companies can and should invest in carbon credits throughout their decarbonization process. But as long as these purchases are not used as a substitute for actual emissions reductions.

The report warns that critical carbon sinks, such as the Amazon Rainforest, are reaching a tipping point. Also, the need for funding for conservation and reforestation efforts is critical.

Companies are encouraged to invest in carbon credits as soon as they set science-based targets with clear plans for achieving them, not just once they have reached their decarbonization targets.

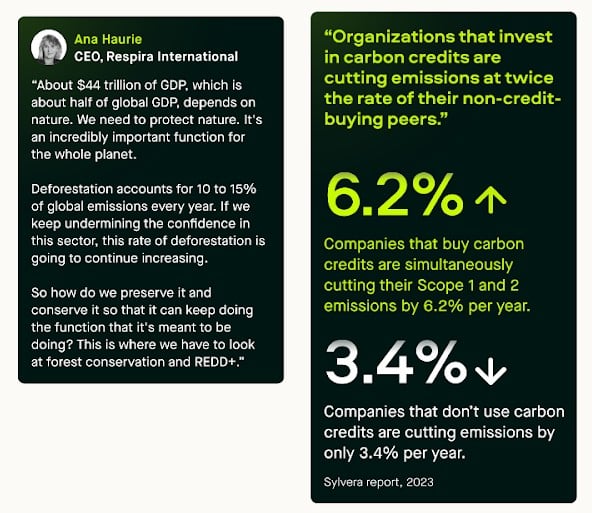

2. “Organizations that invest in carbon credits are cutting emissions at twice the rate of their non-credit-buying peers.”

3. “We’re seeing more and more people move upstream to secure these future optics of quality credits that they can’t find on the spot market today. So really, quality is front of mind, even in the upstream space.”

This highlights a trend in the carbon market where corporate buyers are moving upstream. It means they’re investing in early-stage carbon projects to secure future supplies of high-quality credits.

This shift is driven by the understanding that investing early not only shows commitment to the market but also allows for some control over the project’s development.