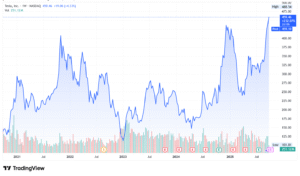

Stock Rises Over $450, Hits Record Market Value of $1.5T as Q3 Delivery Test Looms")

Tesla has once again made headlines after its stock climbed above $450 per share, lifting its market value past $1.5 trillion. This milestone places Tesla among the most valuable companies in the world, alongside tech giants.

The market jump reflects strong investor belief in Tesla’s role as a leader in electric vehicles (EVs) and clean energy. It also shows rising expectations ahead of the company’s upcoming third-quarter delivery results.

While the stock’s performance has impressed many, Tesla now faces new challenges that could affect future demand. One of those challenges has already started to take shape in the U.S. market: leasing costs.

Leasing Gets Pricier as Tax Credit Expires

At the beginning of October, Tesla raised lease prices across most of its American lineup. This change came after a $7,500 federal EV tax credit for leased vehicles expired. The EV giant had previously used the credit to lower monthly lease payments for customers. With the incentive gone, leasing now costs more.

For example, the Model Y saw its monthly lease rate climb by about $50 to $70. The Model 3 also rose by around $80 on some versions. Purchase prices, however, did not change.

This means that buying a Tesla outright still costs the same, but leasing has become less affordable. Leasing has been a popular way for many first-time EV owners to enter the market, so higher rates may slow demand in that segment.

Still, Tesla benefits from the adjustment because it helps protect profit margins at a time when incentives are shifting. This change also ties closely to Tesla’s delivery expectations for the third quarter.

All Eyes on Q3: Can Tesla Deliver Half a Million Cars?

Tesla will soon report how many cars it delivered in the third quarter. Analysts are watching closely, and estimates have been rising. Projections range from 442,000 to more than 500,000 vehicles.

Some firms expect Tesla to deliver around 480,000 units, which would be stronger than expected earlier in the year. Others even believe Tesla could pass the half-million mark, thanks to a last-minute rush of buyers who wanted to take advantage of cheaper leasing before the credit expired.

This boost in sales, however, may create uneven demand. If customers rushed to buy in Q3, the following quarters might see weaker numbers. That possibility has some analysts cautious, even as they raise their short-term forecasts.

Regardless of the exact total, the delivery report will act as a test of Tesla’s ability to keep growing at scale while facing new market pressures.

Investors Fuel Tesla’s $1.5 Trillion Market Cap Surge

The recent stock surge to $459 highlights how much investors believe Tesla can continue to deliver. Moving into the $1.5 trillion market cap club has made Tesla one of the most closely watched companies worldwide.

The optimism is clear: if Tesla reports strong Q3 deliveries, the stock could climb even higher. But expectations are also very high. Any sign of weakness, either in deliveries or future guidance, could push the stock lower.

This tension between confidence and caution explains why Tesla’s stock is so volatile. Every update on sales, pricing, or government policy has the potential to shift the company’s market value by billions in a single day.

Moreover, Tesla’s latest surge is fueled by a proposed $1 trillion compensation plan for Elon Musk, linking his pay to bold targets. These include lifting Tesla’s value from $1 trillion to $8.5 trillion by 2035.

The company is betting big on AI, with robotaxi services using Model Y cars set for Austin in mid-2025. This is followed by Cybercab production in 2026. Tesla also plans to launch Full Self-Driving software version 14 and deploy thousands of Optimus humanoid robots in factories by year-end.

Still, critics caution that Tesla’s high valuation—around 180 times forward earnings—rests heavily on unproven AI ambitions.

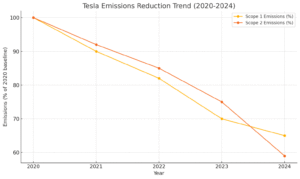

Amid all these, one thing remains: the EV leader’s sustainability and emission reduction drive.

Tesla Balances Emissions Cuts with Supply Chain Challenges

Tesla emphasizes reducing emissions across its operations and product life cycle. In 2024, the company reported a total carbon footprint of about 56 million metric tons CO₂e, combining its own operations and supply chain emissions.

Tesla also notes that in 2023, its customers avoided over 20 million metric tons of CO₂e by driving electric vehicles instead of fossil-fuel cars.

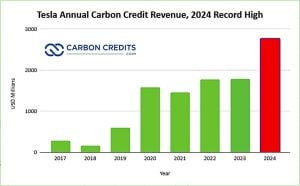

Regulatory credits are another pillar. In 2024, Tesla generated $2.76 billion from selling regulatory carbon credits. This is a 54% increase compared to $1.79 billion in 2023. This revenue comes from providing greenhouse gas (GHG) credits to other automakers that need to meet emissions regulations in the U.S., Europe, and China.

Tesla’s carbon credit sales in 2024 accounted for nearly 39% of its net income for the year, making it a dominant player in the emissions credit market.

To support its goals, Tesla operates its Supercharger network with 100% renewable energy, and its Berlin Gigafactory has run on fully renewable power for the past two years. However, the company still faces its biggest challenge in Scope 3 emissions—those tied to its supply chain and the use of its vehicles.

Opportunities and Obstacles on Tesla’s Road Ahead

Tesla’s path forward is full of both opportunities and risks. The company continues to expand globally, invest in new technologies, and explore new business areas such as energy storage and software. At the same time, it must handle challenges like shifting policies, rising competition, and customer affordability.

On the opportunity side, strong U.S. demand could carry Tesla through short-term changes in subsidies. Growth in markets like China and Europe also offers new revenue streams. Tesla’s work in batteries, charging infrastructure, and AI features may help it build a broader ecosystem beyond cars.

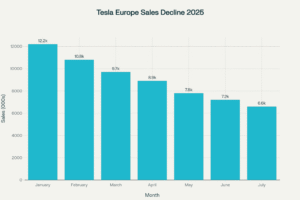

But risks are just as clear. Without the leasing credit, some U.S. customers may wait longer or choose competitors. Supply chain costs could rise, cutting into margins. And with global EV competition heating up, especially from Chinese automakers, Tesla’s share of the market may come under pressure. This has been the case in its European sales.

Managing these factors will decide whether Tesla’s $1.5 trillion valuation remains justified. Investors are already reacting based on how Tesla balances growth with these headwinds.

Tesla’s Future: Growth Under Pressure

Tesla enters the last part of the year in a strong but demanding position. The company has reached a market value that few automakers in history could have imagined. Yet with that success comes more pressure to deliver not just cars, but also consistent growth and profits.

The rise in leasing costs shows how quickly policies can change the market. The Q3 delivery report will test whether Tesla can handle those changes while keeping demand strong. If results meet or beat forecasts, Tesla may strengthen its image as the EV leader. If results fall short, the stock could face new doubts.

Either way, Tesla’s next moves will be closely watched not only by investors but also by the wider auto industry. As the world transitions to electric transport, Tesla’s performance will continue to serve as a signal of how fast and how strong that shift can be.