Disseminated on behalf of Surge Battery Metals Inc.

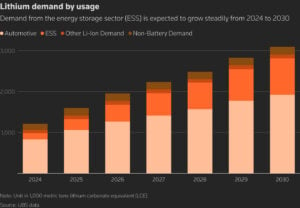

Electric vehicles (EVs) are central to the global shift away from fossil fuels. EV sales continue to rise each year. Analysts estimate that global lithium demand may grow to over 2.8 million tonnes of lithium carbonate equivalent (LCE) by 2030 as EVs and grid storage expand.

Battery energy storage systems (BESS) are another major source of demand. Shipments of stationary storage batteries are forecast to grow around 50% in 2025, driven by renewable energy and grid needs.

Growth in both EVs and energy storage is pushing demand for lithium and other battery minerals higher. Many forecasts suggest lithium demand could more than triple by 2030 versus today’s levels.

These trends are visible in price movements. Lithium prices have risen sharply in recent years. They might hit high levels if demand keeps exceeding supply growth.

Despite some volatility in the market, long-term demand remains robust because EVs and BESS use large amounts of lithium per unit. Cell chemistries like lithium-iron-phosphate (LFP) are expanding, further increasing lithium use across applications.

Tight Supply, Rising Risk: The Global Lithium Bottleneck

Global lithium supply is strained by rapid growth in demand. Supply forecasts have shifted from a modest surplus in 2024 to potential deficits as early as the mid-2020s.

BESS is a key factor. It could account for 30–36% of total lithium demand by 2030, according to major banking forecasts.

At the same time, much of the world’s lithium refining and battery production capacity remains concentrated outside the U.S., especially in China. This concentration raises supply chain risks for North American manufacturers and automakers.

Domestic supply development has not kept pace with demand. Historically, the U.S. produced only a small fraction of the total lithium supply, even though it sits on large known lithium resources.

These factors have pushed companies and governments to speed up new projects and improve local production skills.

Federal Strategy: Building a Domestic Supply Chain

The U.S. government has passed several policies to strengthen the EV supply chain and domestic critical minerals base. Key federal actions include incentives, regulations, and strategic planning. These efforts involve several agencies, like the Department of Energy (DOE) and the Department of Defense (DoD).

Programs like the Inflation Reduction Act (IRA) provide tax incentives for EV manufacturing and battery production. These incentives emphasize sourcing from the U.S. and allied countries to reduce reliance on foreign supply chains. The DOE also funds energy storage research, materials processing, and efforts to scale domestic industrial capacity.

The FY26 National Defense Authorization Act (NDAA) includes provisions that support critical materials production and supply chain resilience in the defense sector. It broadens the Defense Industrial Base Fund’s authority. Now, it includes support for domestic production and modernization projects, including batteries and related infrastructure.

The law sets rules on buying certain key minerals and advanced batteries from non-allied foreign sources. Over a phased timeline, DoD must avoid sourcing these materials from “foreign entities of concern,” such as those linked to China and other designated countries. They must expedite the qualification of compliant domestic and allied suppliers.

The NDAA also requires the Department of Defense to assess weaknesses in key material supply chains. It promotes programs for stockpiling, recycling, and reuse to reduce reliance on imports. These federal actions support U.S. projects that provide lithium, nickel, and other battery materials. They boost confidence for investors and the industry in the domestic supply chain.

Inside the Battery Metals Economy

Lithium’s role in the EV supply chain is clear: it is a core input for lithium-ion batteries. Long-term demand forecasts for lithium reflect this central position. Some market forecasts project global lithium demand to rise to 3–4 million tonnes LCE by 2030, depending on EV market growth assumptions.

Price forecasts vary but generally reflect tightening supply. Some analysts estimate lithium prices could continue to rise if supply fails to match demand growth. Lithium carbonate spot prices recently jumped to $24,086, a 191%+ increase from July 2025.

Nickel and cobalt remain important for certain battery chemistries, even as some EV makers move toward low-cobalt or cobalt-free chemistries. All these metals are part of the broader battery metals ecosystem that underpins the EV supply chain.

Beyond EVs, electric grid storage, industrial batteries, and portable electronics all contribute to long-term demand. Even conservative estimates show sustained growth in battery-grade materials over the coming decade.

Nevada’s Lithium Anchor: NILI and Its Role in the U.S. Supply Chain

Surge Battery Metals (TSX-V: NILI; OTCQX: NILIF; FRA: DJ5) stands out as a lithium exploration and development company focused on the Nevada North Lithium Project (NNLP).

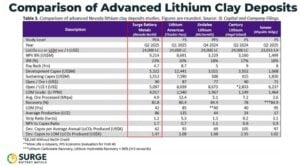

NNLP hosts one of the highest-grade lithium clay resources in the United States. Its inferred resource of approximately 11.2 million tonnes of LCE at an average grade above 3,000 ppm positions it well above many domestic peers.

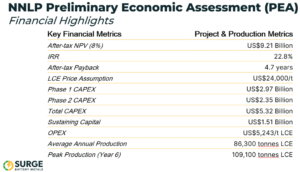

This high quality makes the resource attractive for future development. A Preliminary Economic Assessment (PEA) indicates strong economics. It shows a net present value of about US$9.2 billion and an internal rate of return of over 22%. This reflects the project’s strong potential.

The project’s operating cost metrics are also competitive, with estimated costs significantly lower than those of many North American rivals.

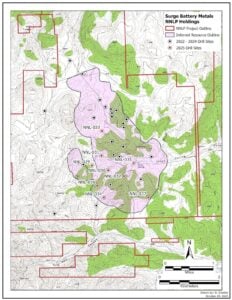

NNLP’s shallow geology and proximity to infrastructure help keep capital and processing costs down. The project sits near power lines, highways, and existing mining hubs in Nevada.

Recent drilling programs continue to show promising results. In 2025, the focus was on infill drilling and core sampling. These efforts aim to upgrade resources and prepare for prefeasibility work. Results show thick lithium clay layers, which boost confidence in the project’s size and consistency.

More recently, Surge reported additional strong drill results from Nevada North. The company announced a 31-meter intercept grading 4,196 ppm lithium from surface in a 640-meter step-out hole to the southeast. This step-out extends mineralization about 640 meters beyond the current resource footprint, confirming the strong continuity of high-grade lithium.

The intercept grade is well above the project’s current average resource grade of about 3,000 ppm lithium. Near-surface mineralization also reduces stripping requirements and supports efficient future development. These results strengthen the project’s scale and reinforce its role as a growing domestic lithium source.

Surge has also secured strategic partnerships. A joint venture with Evolution Mining will speed up exploration and development. This partnership will increase land holdings by over 21,000 acres of promising land.

The company has been recognized for performance in the market, including being named a Top 50 performer on the TSX Venture Exchange in 2024.

Surge Battery Metals plans to improve metallurgical testing for lithium chemicals with over 99% purity. This will help supply battery makers and energy storage companies with high-quality products.

Its management team brings both industry and policy experience, including executives with track records in lithium development and the energy sectors.

Live Nickel Spot Price

The New Energy Reality: Demand, Security, and Strategic Supply

Surge Battery Metals’ project aligns well with broader U.S. efforts to strengthen domestic supply chains for critical battery metals. With rising demand for lithium, NNLP provides a high-quality, near-surface resource. This could greatly benefit the EV and energy storage battery markets.

Domestic projects, such as NNLP, reduce reliance on imports. They can also gain from federal incentives that promote U.S.-based production and processing. This strategic fit makes the project more relevant to policymakers, investors, and supply chain planners.

For policymakers, projects such as NNLP help diversify sources of critical minerals and build resilience against global market disruptions. For investors, strong project economics and top-quality resources offer a way to create value as market demand increases.

The U.S. EV supply chain race centers on securing reliable sources of battery metals. Lithium remains at the heart of this transition, driven by both EV and energy storage demand. Strong long-term demand forecasts and tighter supply show the need for new domestic sources.

The federal strategy backs this shift with policy incentives, funding, and programs. These focus on resilient, locally sourced materials. This environment favors projects that are high quality, well-positioned, and strategically relevant.

Surge Battery Metals and its Nevada North Lithium Project represent one such opportunity within the U.S. critical minerals strategy. NILI has solid resources, low costs, and important partnerships. This enables the company to strengthen the U.S. supply chain for lithium and other battery metals. This alignment shows how market forces and policy priorities shape the future of EVs, energy storage, and clean energy infrastructure.

- READ MORE: Surge Battery Metals Strengthens Nevada North With High-Grade Expansion and Infill Success

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that the information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable, but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.