Tungsten, a critical mineral with unmatched heat resistance and strength, is gaining global attention. It’s dense, brittle, and grayish-white, with the highest melting point and tensile strength of any pure metal. These traits make it vital for high-performance applications. and industries needing extreme durability.

With China controlling most of the supply, the U.S. and allies are racing to secure domestic sources and diversify supply chains. Let’s deep dive into the complete outlook of the tungsten market below:

Demand Drivers: Why Tungsten Keeps Rising in Importance

The tungsten market expanded from USD 6.04 billion in 2024 to USD 6.50 billion in 2025. It is projected to grow at a CAGR of 7.95%, reaching USD 11.16 billion by 2032.

Its demand is rising due to industrial and defense needs. Key drivers include:

- Electronics & Semiconductors: Vital for high-performance chips and circuits.

- Defense & Aerospace: Used in rocket nozzles and armor-piercing ammunition. It also strengthens steel alloys for aerospace and defense.

- Tungsten is used in turbine blades and as a lead substitute in ammunition.

- Industrial Tools: Crucial for cutting and drilling in mining, construction, lighting, welding, and manufacturing.

- Green technology and electrification: Increasing use of tungsten in electric vehicle batteries, energy storage, and renewable energy technologies

Industry experts are indicating that global tungsten demand is expected to rise in 2025 and the next few years. With geopolitical tensions increasing, the U.S. and allies anticipate further growth as supply diversification becomes essential.

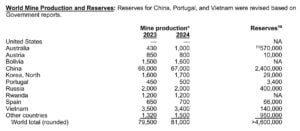

China’s Tight Grip on Tungsten Supply

Tungsten is found worldwide, but most supply comes from China. It produces over 80% of global tungsten and holds more than half of the known reserves. Vietnam and Russia follow, contributing only a small share. Other producers like Spain, Austria, Bolivia, and Rwanda account for just 1% to 2% each.

Interestingly, other countries own about 35% of global reserves but produce only 1%. This gap shows growth potential but highlights challenges like high costs and long permitting times.

China also controls production. In late 2024, Beijing introduced new export licensing rules for tungsten, tightening supply further. Analysts view these controls as part of China’s strategy in global trade.

Global Push for Supply Chain Resilience

China’s dominance has raised concerns. Countries are diversifying their tungsten supply chains. New projects in Australia, South Korea, Canada, and Africa show promise, but scaling up will take years.

Vietnam, Russia, and Spain are boosting production. Smaller nations like Rwanda are gaining attention for their resources. However, these efforts face high costs and technical challenges.

China’s market control is expected to last until the early 2030s, but momentum is shifting toward more resilient supply options.

U.S. Tungsten Dependence: A Strategic Risk for Defense

As per the U.S. Geological Survey, the U.S. has not mined/ tungsten since 2015. It relies mostly on imports, especially from China. Notably, in 2023 U.S. imported over 10,000 metric tons of tungsten.

Most U.S. tungsten is used in cemented carbide parts for construction, mining, and drilling. The rest goes to specialty steels, defense alloys, electronics, and chemicals.

This dependence poses serious risks as tungsten is vital for defense applications, including armor-piercing munitions and missile systems. Thus, supply disruptions could threaten U.S. military readiness and high-tech industries.

DoD’s Big Investments and New Rules

The U.S. Department of Defense (DoD) is boosting efforts to secure tungsten, a critical metal for defense systems. Since last year, it has directed millions toward U.S. and allied projects.

In July 2025, it awarded $6.2 million under the Defense Production Act to Golden Metal Resources for the Pilot Mountain project in Nevada, the largest undeveloped tungsten deposit in the U.S.

The project aims to restore domestic production, reduce reliance on China’s 80% market share, and prepare for the 2027 ban on China- and Russia-sourced tungsten in defense contracts.

Procurement Rules

A new U.S. law prevents the Pentagon from sourcing tungsten, magnets, and other critical materials from adversarial nations like China, Russia, Iran, and North Korea. By January 2027, these rules will also cover the mining stage. This means tungsten mined in these countries can’t enter U.S. defense supply chains.

Thus, the U.S. Department of Defense now views tungsten as a national security issue. In summary, its strategy focuses on:

- Diversifying supply chains beyond China.

- Funding domestic exploration and allied projects.

- Expanding metallurgical testing and engineering studies.

- Tightening procurement rules to phase out adversarial tungsten by 2027.

This effort demonstrates a strong commitment to boosting domestic tungsten production for new defense systems and advanced manufacturing. Additionally, it also aims to build secure supply partnerships with allies.

Top Tungsten Stocks Gaining Investor Attention

In 2025, tungsten stocks are attracting attention as the metal becomes essential across industries. Rising demand and tight supply make these stocks appealing. Investors value tungsten for its strategic role in technology and its relatively stable prices compared to other critical minerals.

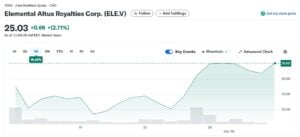

Elemental Altus Royalties Corp. (ELE.V) Rises on Strong Momentum

Canada-based Elemental Altus trades around $15.76 USD (OTC) and CAD 24.37 (TSX Venture) as of October 2025. Its shares climbed nearly 47% in six months, outperforming peers, with a market cap of $388 million USD. Analysts set the TSX target price at CAD 25.92, signaling upside potential.

In September 2025, it merged with EMX Royalty to form Elemental Royalty Corp. Tether Investments backed the deal with $100 million USD to buy 75 million shares at CAD 1.84 each. The capital fuels growth, acquisitions, and expansion in tungsten, rare earths, and other critical minerals.

Elemental Altus leads in the critical minerals’ royalty space, with strong stock momentum and strategic investments positioning it for growth.

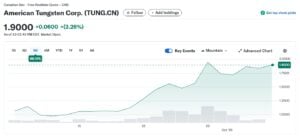

American Tungsten (TUNG) Fuels U.S. Supply Revival

American Tungsten Corp. (TUNG) is gaining attention as a pure-play tungsten stock. In February 2025, it hit an all-time high of CA$2.37, reflecting strong investor confidence in the company’s efforts to develop domestic tungsten resources.

Currently, it is trading at around CAD 1.84 per share. Analysts forecast the stock to rise through the rest of 2025 and into 2026.

With a market capitalization of roughly CAD 25.72 million, the stock has experienced some volatility. This was influenced by critical minerals sector trends and tungsten market dynamics.

However, the company’s performance remains closely tied to progress in U.S. tungsten projects, government support, and global supply-demand trends.

In March, the company announced that its application to join the U.S. Defense Industrial Base Consortium (DIBC) had been approved. The consortium, managed by Advanced Technology International (ATI) for the Department of Defense (DoD), connects private-sector companies with the U.S. Government to strengthen the defense supply chain.

Another key development is the IMA Mine Project in Lemhi County, Idaho, a major step in restoring U.S. tungsten production. This critical mineral supports tank armor, hypersonic weapons, submarine hulls, and semiconductors.

The Rise of Tungsten Juniors

However, this year, several junior mining companies focusing on tungsten in the U.S. are also gaining attention, particularly those developing critical mineral resources to strengthen domestic supply chains.

One such example is Patriot Critical Minerals. It owns100% of the MEGA Deposit in Elko County, Nevada, a strategically located resource that could help close the domestic tungsten supply gap.

The deposit contains approximately 19 million tonnes of mineralized material, with about 32,300 tonnes of contained tungsten trioxide.

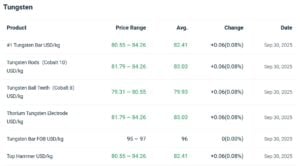

Tungsten Prices Stay High Amid Tight Supply

In September 2025, tungsten bar FOB prices held steady at USD 95–97 per kg. Meanwhile, tungsten concentrates (scheelite and wolframite) traded at RMB 284,000 per ton. This marked a 1.1% drop from peak levels but doubled the price from early 2025, showing strong market volatility.

However, global prices continue to fluctuate due to Chinese export restrictions, production issues, and rising demand in defense, aerospace, and electronics. At the same time, supply-demand gaps, geopolitical tensions, and stockpiling keep prices elevated.

In conclusion, rising demand, tight global supply, and national security concerns make tungsten a strategic mineral. Consequently, U.S. projects and companies like Elemental Altus, American Tungsten, and Patriot Critical Minerals are actively reducing reliance on China.

As production ramps up, tungsten will play an increasingly vital role in defense, technology, and industrial applications.