The recently released “State of the Voluntary Carbon Markets 2023” report by Ecosystem Marketplace (EM) reveals a significant trend shift within the VCM. It identifies a concentration of demand toward high-integrity and high-quality voluntary carbon credits, despite their higher price, that offer co-benefits beyond mitigating greenhouse gas emissions.

Analysis of transaction data indicates a substantial 82% surge in average carbon credit prices from 2021 to 2022, accompanied by a decline in overall transaction volumes. These findings imply a market consolidation among smaller yet dedicated purchasers willing to pay more for credits of superior quality.

Notably, there’s a high demand for nature-based credits that hold certifications for co-benefits and align with Sustainable Development Goals (SDGs).

Here are the key points to particularly note from EM’s research.

5 Key Takeaways From the Report:

-

Prices are at their peak, volume is down

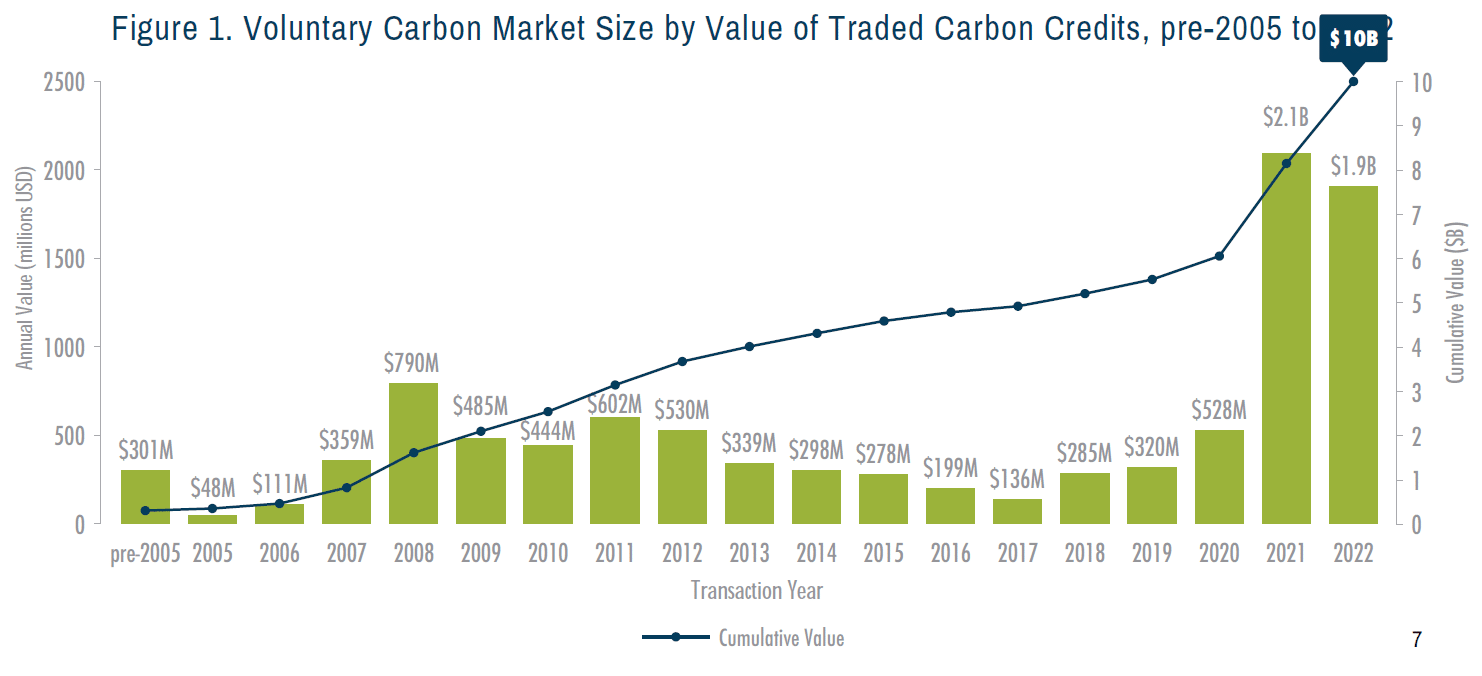

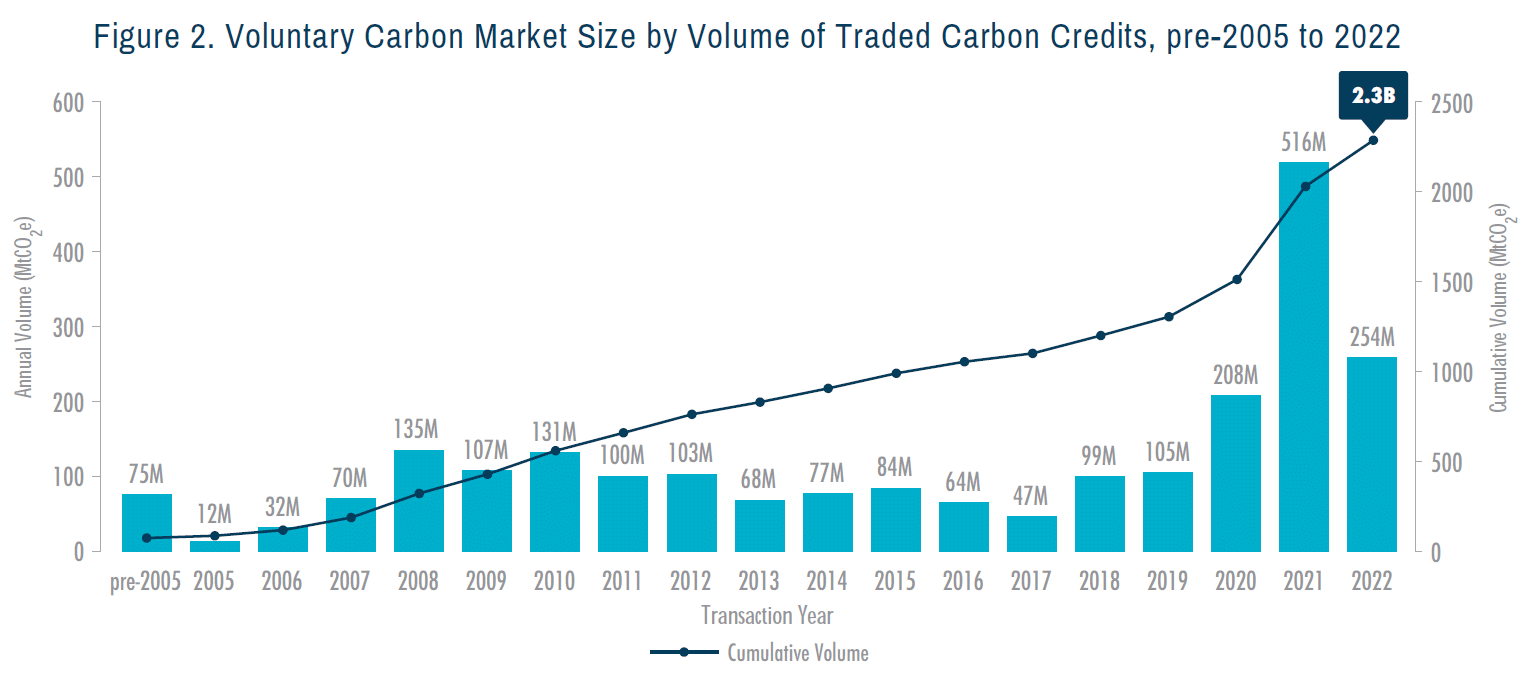

The average prices of voluntary carbon credits have reached their highest point in 15 years, while the overall trade volumes have declined from the peak seen in 2021. Even though the volume of voluntary carbon credits traded fell by 51%, the average price per credit surged significantly by 82%. It jumped from $4.04 per ton in 2021 to $7.37 in 2022, which hasn’t been seen since 2008.

Despite the drop in trade volume and value, this price increase allowed the VCM to remain relatively stable in 2022. In fact, despite dropping ~$0.40/ton, average prices to date in 2023 are still higher than in 15 years.

-

Nature-based credits take the biggest market share

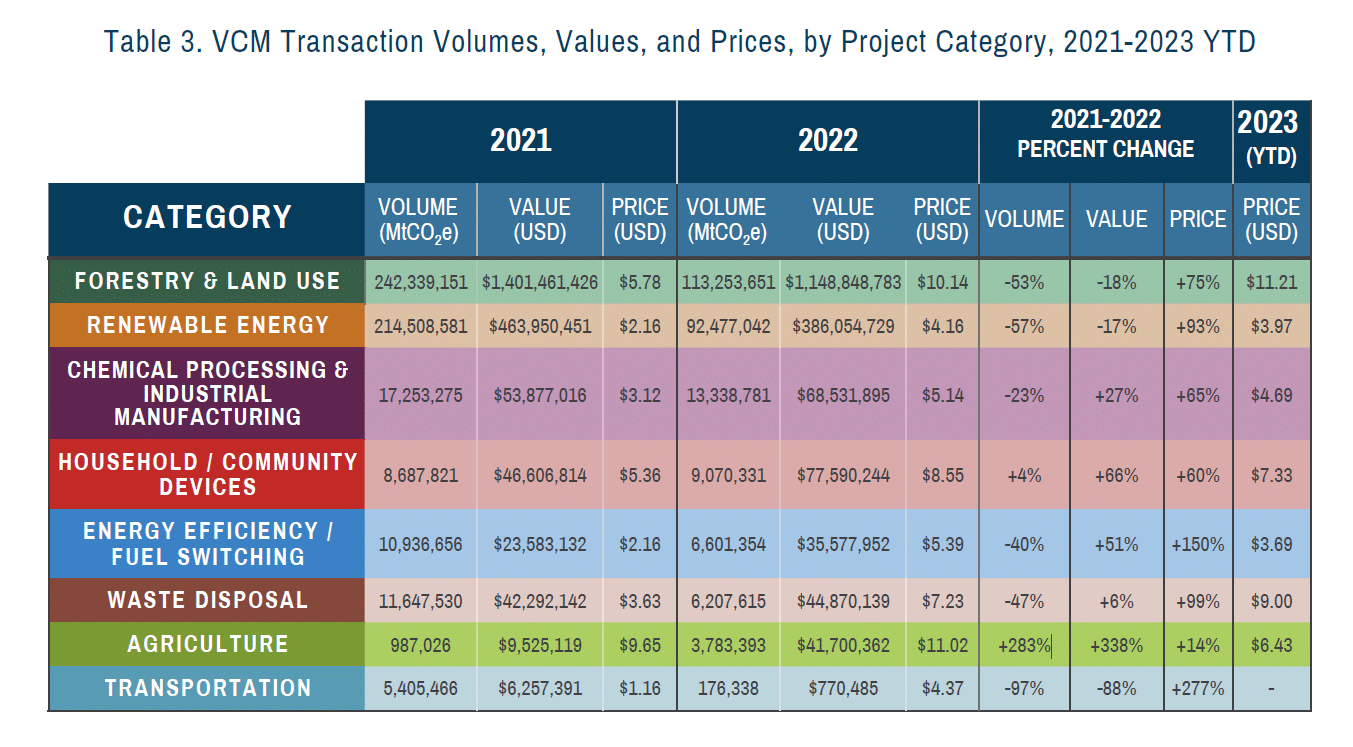

Nature-based solutions (NBS) were a primary contributor to the high market value, constituting nearly half of the market share – 46%. NBS credit prices were more than doubled in 2021 and 2022. EM is also seeing more premium for these credits in preliminary 2023 VCM data.

The average price of credits from nature-based projects, including forestry, land-use, and agriculture projects, witnessed an increase of 75% and 14%, respectively, from 2021 to 2022.

REDD+ projects dominate the NBS credits, but also include other projects in the Agriculture and Forestry and Land Use categories. These include Sustainable Agriculture Land Management Afforestation/Reforestation/Revegetation (ARR), Agroforestry, Improved Forest Management (IFM), and Blue Carbon (mangroves, seagrasses).

REDD+ projects dominate the NBS credits, but also include other projects in the Agriculture and Forestry and Land Use categories. These include Sustainable Agriculture Land Management Afforestation/Reforestation/Revegetation (ARR), Agroforestry, Improved Forest Management (IFM), and Blue Carbon (mangroves, seagrasses).

Agriculture project credits, also called agricultural carbon credits, also experienced a substantial surge in volume, rising by 283%.

-

Credits with co-benefits are pricier

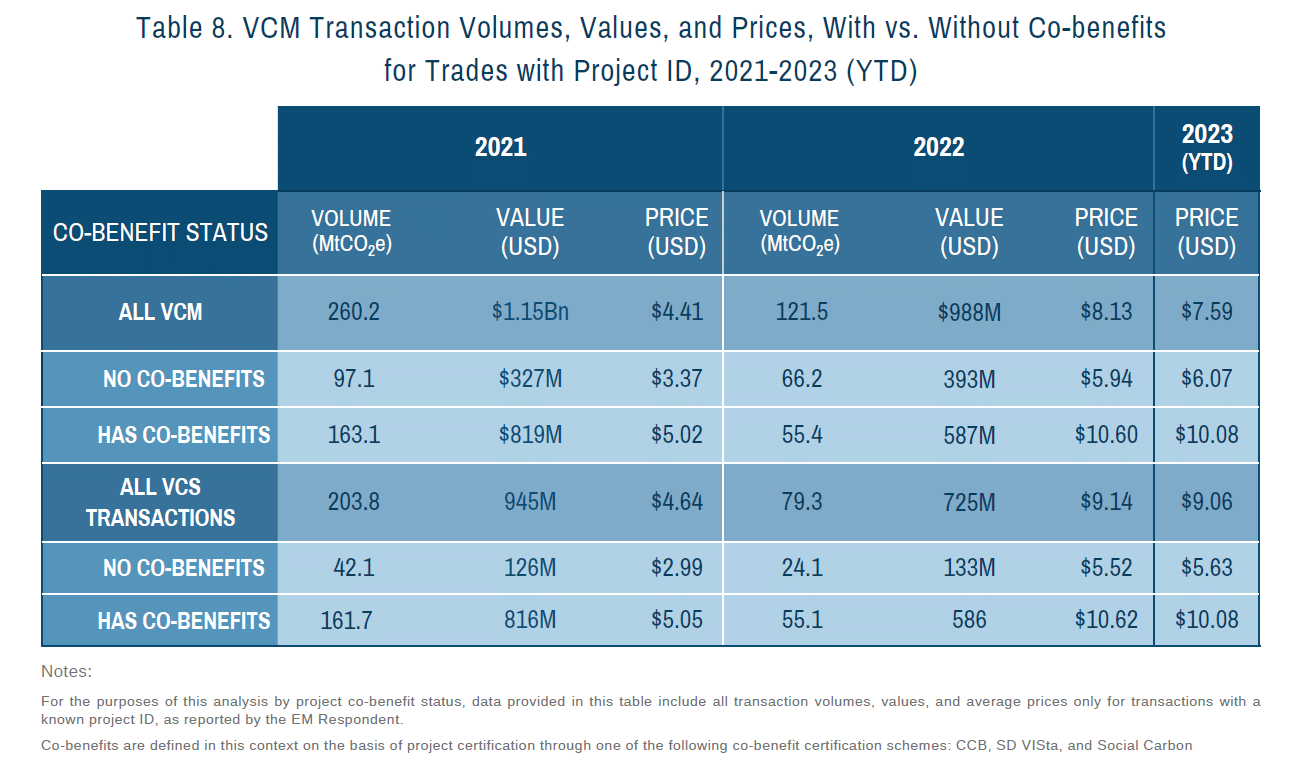

Credits associated with robust environmental and social co-benefits, extending beyond carbon, commanded a significant price premium. Projects with at least one co-benefit certification had a 78% price premium compared to those lacking such certification.

According to experts surveyed by Ecosystem Marketplace, these certifications are becoming increasingly necessary for buyers actively looking for these projects. Moreover, projects aligned with the UN SDGs demonstrated a considerable price premium, 86% higher than projects not linked to SDGs. This indicates a strong buyer preference for credits that contribute more to societal and environmental well-being.

-

Buyers prefer newer credits

Newer carbon credits are commanding a higher price, suggesting that voluntary buyers are inclined towards recent vintages featuring more robust methodologies. EM reporters also suggested that these buyers prefer credits closely aligning with their current emissions years.

In 2022, there was a 57% premium for credits with a more recent vintage, reflecting recent emissions reduction activities, compared to a 38% recency premium observed in 2021. This comparison used a historical 5-year rolling cutoff date from the transaction year.

-

CORSIA-eligible credits surge

Credits eligible under CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) experienced a significant surge in market value, marked by a 126% increase in price. The notable growth of CORSIA in the VCM in 2022 indicates an expanding relationship between compliance markets and the VCM. This is crucial for market participants due to several factors:

- The quality criteria outlined by CORSIA have been adopted by the Voluntary Carbon Markets Integrity Initiative (VCMI) until the Integrity Council’s core carbon principles are fully established.

- CORSIA will enter its inaugural compliance phase in 2024.

- Countries are beginning to implement Paris Agreement’s Article 6, further emphasizing the relevance of CORSIA in broader carbon markets.

A Shift Towards Integrity and Quality

The latest report by Ecosystem Marketplace delves into self-reported transaction data from >160 participants in their annual market survey. These contributors represent credits sourced from 1,530 projects across over 130 project types traded globally.

Typically, respondents encompass project developers, investors, and intermediaries. Moreover, data regarding project registrations, credit issuances, and retirements were collated from project registries, adding depth to the comprehensive analysis presented in the report.

Stephen Donofrio, Managing Director of Ecosystem Marketplace, highlighted the pivotal moment witnessed in the VCM, noting that:

“While the data do not show the same type of growth by volume present in previous reports, our market analysis shows a critical, increased shift in market behavior towards integrity and quality.”

Donofrio further emphasized the evolving sophistication of credit buyers, underscoring their eagerness to understand the actual impact of their investments.

EM’s full report is available for download here.