Carbon capture and storage (CCS) companies in Europe face several roadblocks in getting their projects up and running on a commercial scale and that’s despite record carbon prices in the region.

Interest in CCS now spans several countries in the region. These include Italy, Germany, Greece, Belgium, Iceland, Sweden, Poland, and Denmark, following first movers Norway, the Netherlands, and the UK.

Costs of Carbon Capture & Storage in Europe

The complex nature of CCS projects calls for a high initial investment which restricts product adoption. But forecasts show promising growth for the sector.

In 2022, the industry is valued at over $6 billion and is projected to grow to over $35 billion by 2032.

Carbon prices cover some part of the costs of the carbon capture and storage process in the EU.

Last month, carbon prices in the EU ETS – Emissions Trading System – surged over 100 Euros per metric tonne for the first time. It has remained at high levels since then and didn’t go below 95 Euros, so far.

Still, CCS developers said that they need government support to make their projects alive.

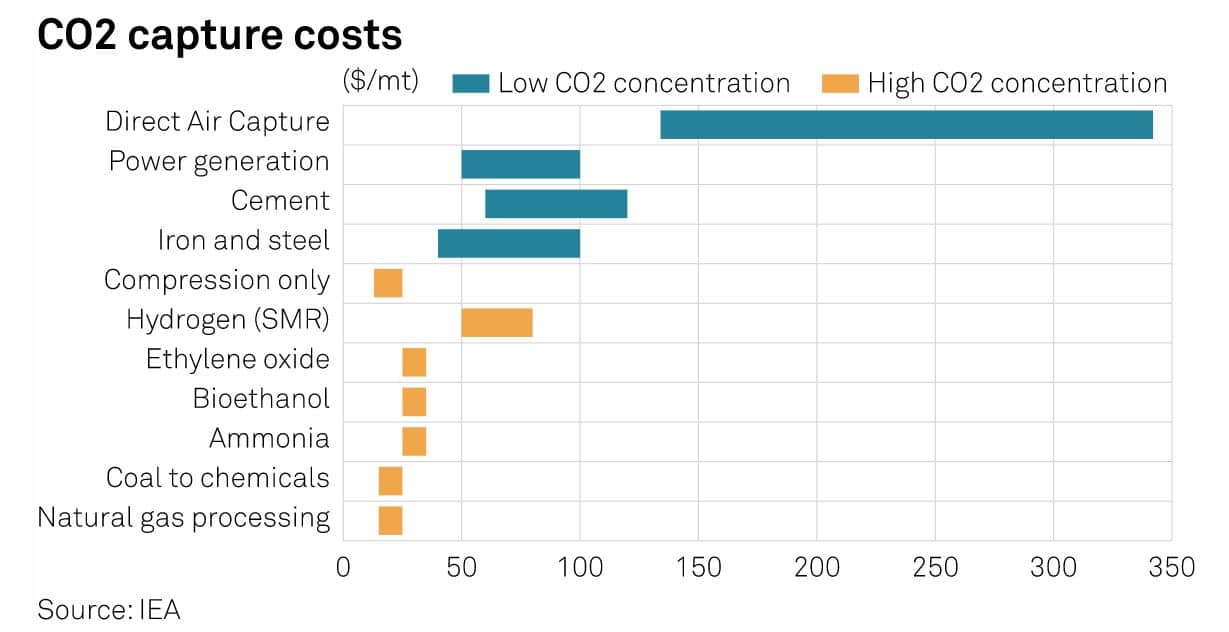

When it comes to actual costs, carbon capture costs in the EU vary a lot, depending on the specific sector. For carbon storage and transport, the costs range between 9 to 19 Euros/mt or US$10 to $20/mt.

For some CCS developers, the costs of capturing carbon are around $30-$40/mt. But for industries with lower carbon emission concentration, the costs are higher as per the International Energy Agency estimates.

As seen in the chart, direct air capture (DAC) systems cost highly expensive, ranging from about $130 to $340/mt.

Though EU carbon prices seem to cover the CCS costs, there are still some things that make commercial scale-up challenging.

Barring CCS Commercialization

The CCS industry is very nascent with the largest market in North America. Europe has the least market share but it’s also the fastest-growing market for CCS.

One of the hurdles for the entire CCS sector to become established in the EU is the right economic model. After all, the global LNG sector took a very long time to achieve its maturity today. The same might be the case for CCS.

So, without support from the state, building the CCS sector from scratch may take even longer to mature.

Models both for capture and storage

Just like other sectors, CCS also needs to have business models that work for both sides of the market.

On one side, the polluters need some kind of insurance so that the carbon captured from their facilities will have a place to go to. On the other side, the storage facilities also have to know that there’s enough carbon for them to store.

A leader of the UK’s Viking CCS project noted that the system of carbon capture and storage itself doesn’t need funding from the government, but the emitters do.

Located in the Humber, the Viking CCS project aims to create a CO2 capture, transport, and storage network. It targets start-up in 2027 and an emission reduction of 10 million tonnes a year in the UK by 2030.

Harbour Energy, the largest London-listed independent oil and gas company, is leading the Viking CCS project. According to its CEO, “at least part of our project will be regulated in terms of what we can charge”. And so they need to know how that model will work.

What that means is the importance of having a regulatory framework in place indicating the government’s support for liability related to carbon storage. The state has to regulate the polluters within the CCS network.

Bringing forward regulation for CCS projects and delivering the business models they need in legislation is urgently needed. Without acting fast enough and causing project delays will only further increase the cost of developing and commercializing CCS in Europe.

Too early to tell

The CCS sector is at its early stage of market development, which creates another roadblock for growth – technology risk.

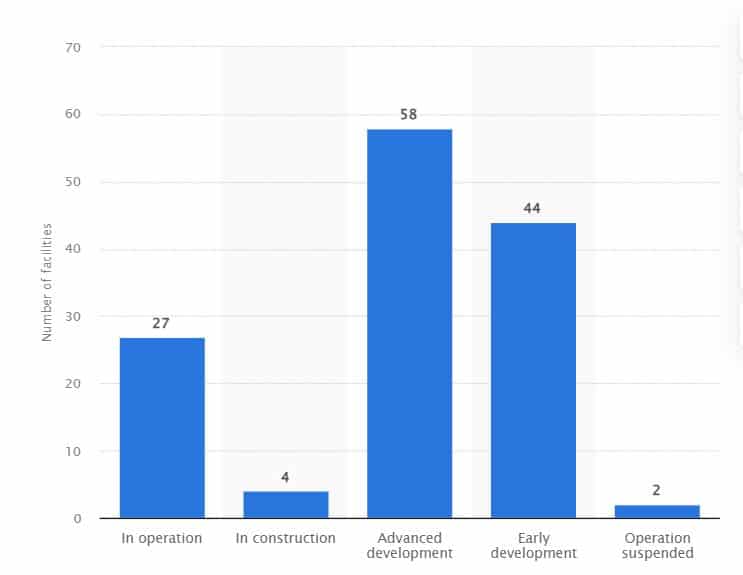

Globally, there are only about 27 large-scale CCS facilities in operation around the world as of 2021.

Number of large-scale CCS facilities as of 2021, by status

One of the largest projects in the world – Gorgon – is run by Chevron in partnership with Shell and Exxon. It’s in Australia linked with Chevron’s LNG facility.

It’s an example of a commercial-scale CCS project that experienced commissioning delays and start-up problems. It didn’t meet its carbon capture targets while putting the energy companies liable for regulatory issues.

These problems are common in a market that’s still in its infancy stage like CCS. This puts project developers in a position where research and surveys, which are time-consuming, don’t always translate to project development.

In a sense, developers are still exploring the space and discovering which systems or technologies are best to invest in.

Attracting Project Financing

Another barrier for carbon capture and storage to take off in Europe is the concern with project financing.

As an investor or financier, one would like to ensure that the money it lends won’t end up in a loss. But more importantly, when financing this kind of project, lenders will give it a go if there’s strong support for the technology.

Meanwhile, bankers interested in funding CCS projects prefer the contract-for-difference arrangements against the EU ETS carbon prices for a period of one decade.

Fortunately, venture capital-supported startups and large oil and gas firms mentioned above also show a strong commitment to promoting the sector.

But one more problem persists – large discounts on carbon prices in favor of the lenders, according to Ruth Herbert. The CEO of CCSA said:

“The challenge is convincing financiers to invest capital. They do not quite trust the carbon price or politicians.”

She added that financiers wanting to support long-term CCS think that only 30% of carbon prices is worth funding.