In 2024, the Carbon Capture, Utilization, and Storage (CCUS) landscape is poised for significant developments, with key themes and trends shaping the industry. Wood Mackenzie had some predictions for the year as laid out in their report, expecting storage capacity to grow rapidly.

CCUS has long been a crucial energy transition topic, playing an important role in the global net zero 2050 scenario. The research company predicted that CCUS capacity will increase from 80 metric ton per annum (Mtpa) to over 500 Mtpa.

Here are the major takeaways from Wood Mackenzie 2024 CCUS outlook report.

Unprecedented Number of CCUS Project Final Investment Decisions (FIDs)

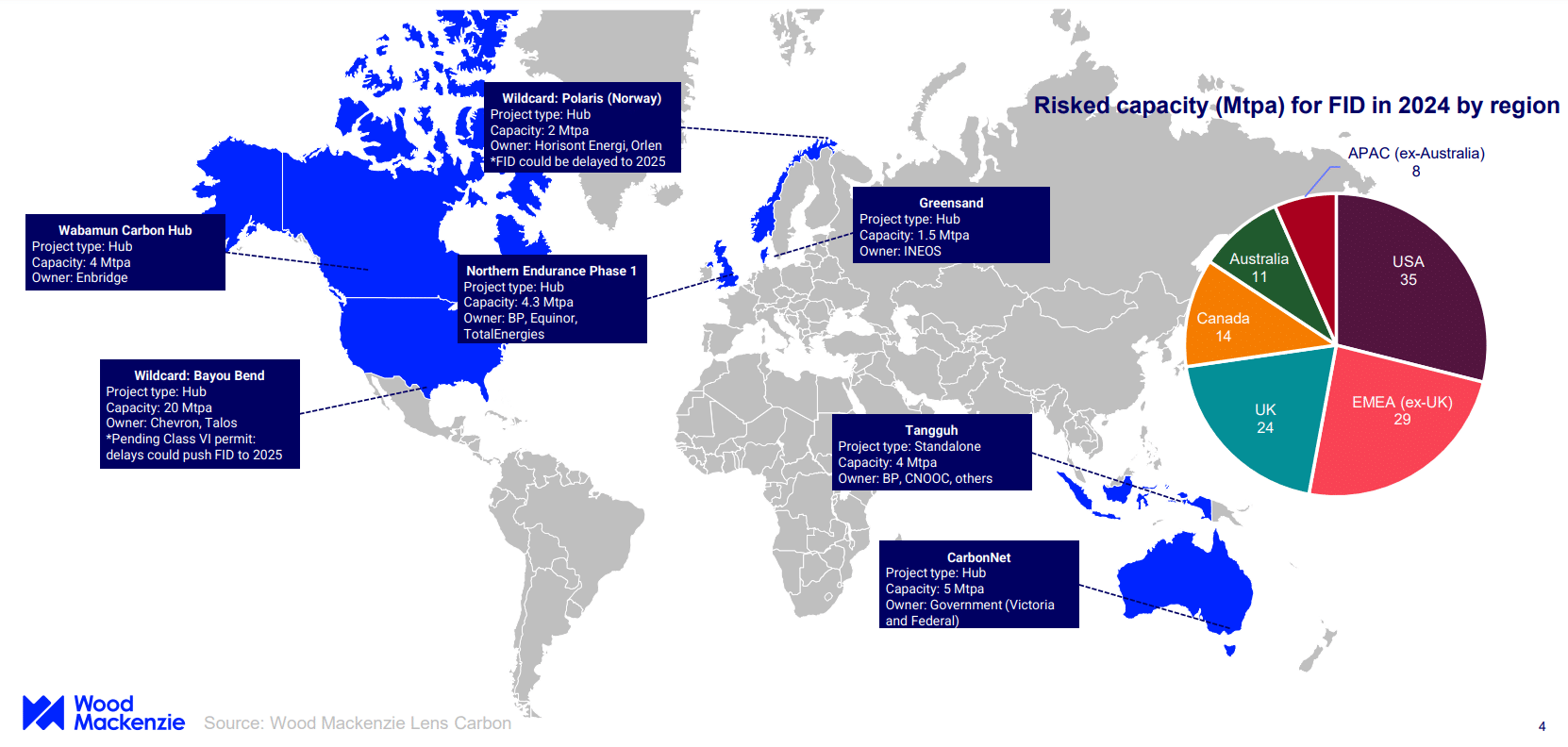

The global CCUS pipeline would grow, with 119 projects aiming for FID in 2024, representing the largest number to date. These projects collectively target 115 Mtpa capture capacity and 240 Mtpa storage capacity. The map below shows the CCUS project hotspots and each region’s risked capacity.

Those projects reaching FID status this year are primarily hubs in North America and Europe. As illustrated below, the increase in projects’ capacity estimated this year more than doubled compared to last year. Over 60% is in North America.

CO2 Storage Licensing Momentum

Licensing activity for CO2 storage will continue to support the increase in project capacity. New licensing rounds are anticipated in the US and the UK. Wood Mackenzie expects majors like Chevron, Equinor and TotalEnergies to bid in Texas.

Over in Denmark, the country opened applications for CCS licenses in 5 onshore areas in December last year. Australia also opened 10 new blocks for the 2023 GHG acreage release, where Santos, Woodside and INPEX are likely to increase current acreage.

Meanwhile, Southeast Asia may witness the formal opening of CO2 storage license areas in Malaysia and Indonesia. Petros is the sole company which received 2 CO2 storage licenses in Malaysia.

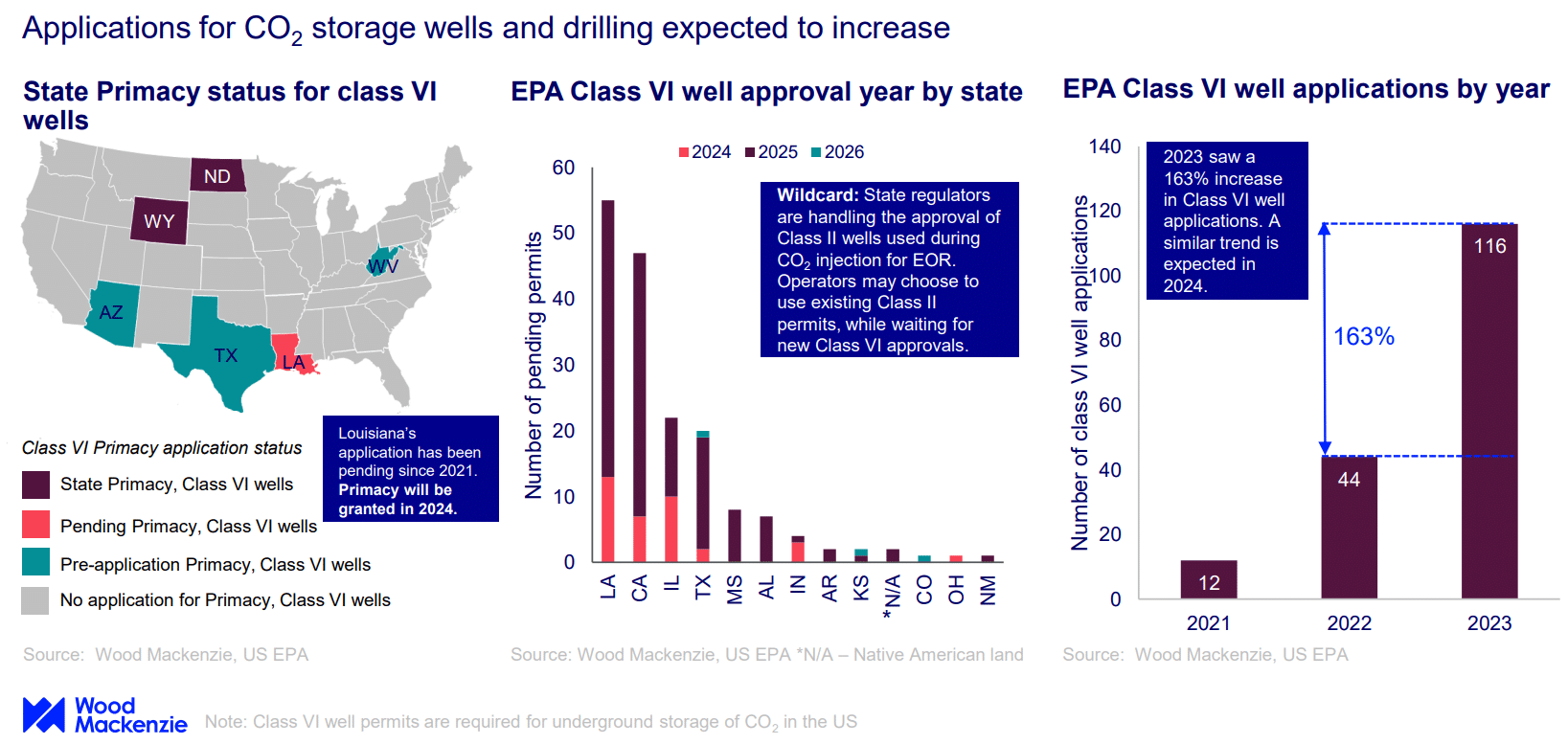

Moreover, regulatory changes are expected to expedite project timelines, leading to increased applications for CO2 storage wells and drilling.

Advancements in Direct Air Capture (DAC) and New Capture Technologies

In 2024, there will be a focus on achieving at-scale readiness for DAC. Direct air capture is one of the go-to capture technologies available today.

Below are the expected developments in DAC this year per Wood Mac outlook:

-

- Stratos, the world’s first global-scale DAC plant with a capacity of 0.5 Mtpa, is expected to reach or near the end of construction.

- Climeworks‘ Mammoth DAC project would start operations in the second half of 2024.

- The US Department of Energy would announce additional DAC hubs and finalize funding amounts.

- Startups may develop pilots featuring newer technologies, reaching technology readiness level 6.

Despite these advancements, challenges related to cost and execution risks remain. The research firm will continue to report how new DAC projects can help improve operational efficiency and reduce costs.

Introduction of New Capture Technologies and Industry Involvement

2024 would see project announcements, FIDs, and startups involving new capture technologies and industries. Notable projects, such as Svante’s Veloxotherm Technology, could play a game-changing role.

Projects for commission this year include carbon capture technologies developed by Aker Carbon Capture, LanzaTech, and Honeywell UOP. They’re located in Norway, South Africa, and the US, respectively.

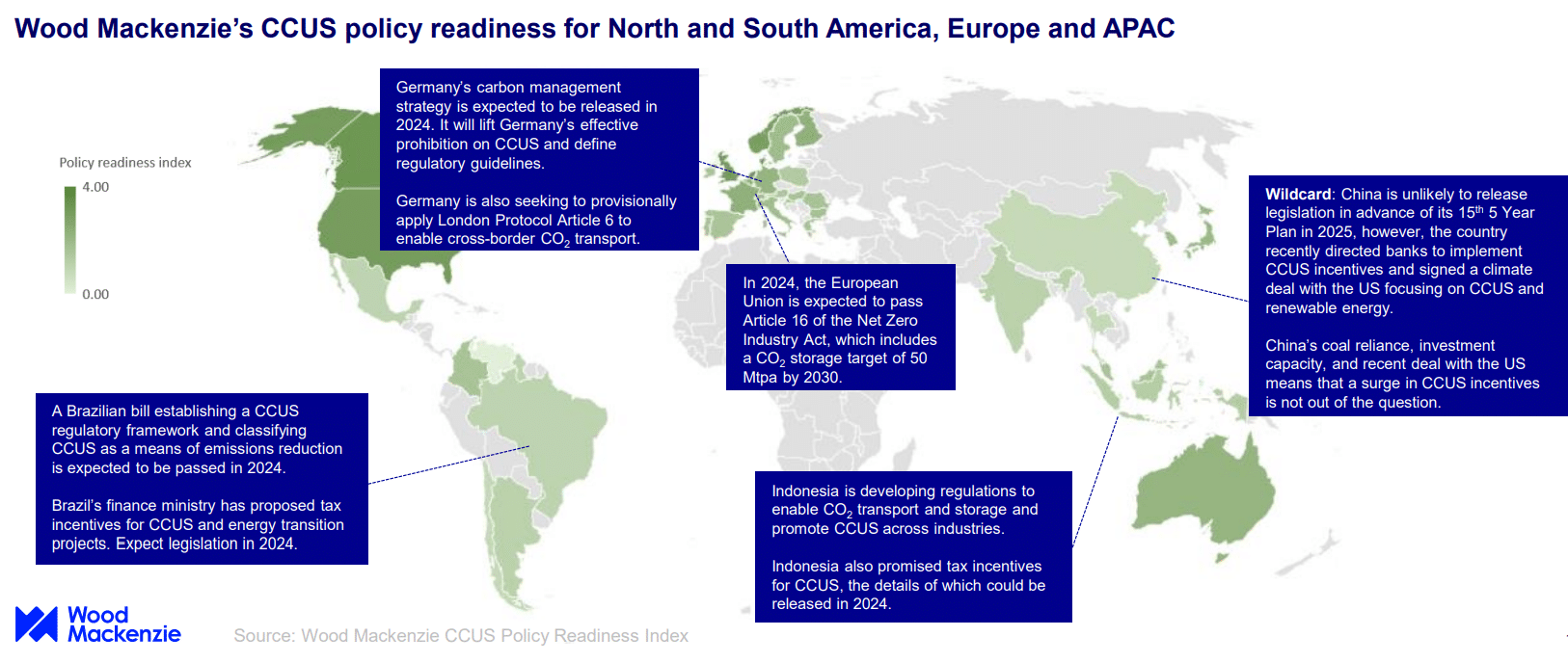

Lastly, the report also covers the evolving regulatory framework, highlighting the development of regulations.

It further explores the potential impact of global elections in 2024 on CCUS policies, particularly the U.S. elections. The full report provides in-depth insights into these predictions and trends shaping the CCUS landscape.

In a separate analysis last year, Wood Mackenzie said that to reach global net zero goals by 2050, carbon capture has to hit 7 billion tonnes of CO2 a year.

With an anticipated surge in Final Investment Decisions (FIDs), growing CO2 storage licensing momentum, and advancements in Direct Air Capture (DAC) and new capture technologies, 2024 unfolds as a pivotal chapter in the journey towards global net zero by 2050. The industry is poised for unprecedented growth, innovation, and strategic partnerships, positioning CCUS as a key player in the energy transition landscape.