CORSIA, managed by the International Civil Aviation Organization (ICAO), requires airlines to monitor and report their emissions, allowing them to purchase emission reduction units, also called carbon credits, if they exceed a set baseline.

The program updates impact both airlines and the carbon market, signalling which credits are eligible and influencing future market purchases.

What Are the New CORSIA Updates?

Recently, CORSIA reviewed and approved six carbon credit standards for its first phase. These include Winrock International’s American Carbon Registry and Architecture for REDD+ Transactions, which were approved without exclusions.

The Climate Action Reserve (CAR), Global Carbon Council (GCC), the Gold Standard, and Verra’s VCS program, were conditionally approved while CDM didn’t qualify for Phase I.

CORSIA allows credits from 2021 onwards with a corresponding adjustment to avoid double counting. This adjustment ensures that credits used for CORSIA don’t overlap with a country’s emission reduction goals under the Paris Agreement.

The mechanism ensures that the allocation of the credits represents real carbon reduction activity and sales, boosting carbon market integrity.

The CORSIA’s Technical Advisory Body (TAB) recommendations from the review influence the market by increasing demand for approved credits. This doesn’t only cover the airlines but also signals other buyers to consider the credits “best-in-class”.

This will affect credits currently available and the future ones, driving up demand in both cases. However, some high-quality credits endorsed by ICROA are not accepted under CORSIA, affecting their eligibility.

Apart from the reassessment, the TAB will also assess any new applications for standards that hadn’t already been approved. The ICAO Council will officially take into account TAB’s recommendations this fall after assessing new credit standard applications.

How Should Airlines Take The Changes?

For airlines preparing for CORSIA’s upcoming phases, it’s important to align their credit strategy with the TAB recommendations for compliance. They need to ensure they make CORSIA-compliant purchases before the true-up deadlines.

For the pilot phase (2021-2023), airlines don’t need to show compliance until January 31, 2025. For phase I (2024-2026), the deadline is January 31, 2028. To meet these deadlines, airlines should plan credit purchases well ahead to avoid any risks.

Due to CORSIA’s multi-year requirements, airlines might consider multi-year purchasing agreements to secure their credits. These agreements should align with both the pilot phase and phase I standards.

While some standards are conditionally approved for phase I, like VCS and Gold Standard, they’re likely to receive full approval.

It’s important to note that credits meeting post-2021 criteria are not yet available. Airlines can fulfill pilot phase purchasing requirements under the existing standards but need to wait for phase I eligible credits. Any long-term deals should consider these factors and specify the qualifying years.

To effectively implement a credit purchasing strategy, clear communication and internal education within airlines are crucial. Airlines should anticipate delays in the availability of Phase I credits, likely not until 2024 at the earliest.

Additionally, CORSIA eligibility rules may increase demand and prices for these credits, so airlines should budget accordingly.

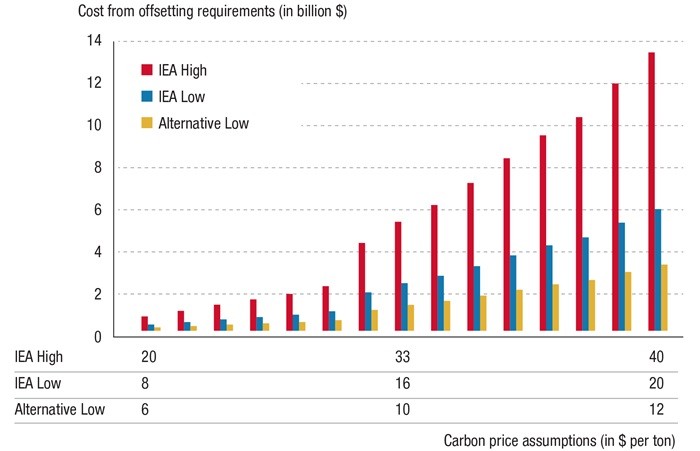

The ICAO estimated the costs from CORSIA offsetting for airline operators as shown in the following chart. This is under the assumption that carbon prices range from a low of $6 – $12 to a high of $20 – $40 per tonne of CO2.

What Are the Effects on Non-Airline Credit Buyers?

Airlines aren’t the only ones affected by CORSIA – the program also impacts those buying carbon credits beyond airlines.

As airlines rush to buy these credits, the limited market will see growing demand, leading to higher prices. Non-airline buyers might also view TAB recommendations as a sign of credit quality, increasing demand for CORSIA-eligible credits and their prices.

For those using CORSIA-approved credits in their carbon strategy, it’s smart to watch these market changes. Adjusting budgets, keeping stakeholders informed, and buying credits well ahead of deadlines can help prepare for these shifts.

While some high-quality credits aren’t eligible under CORSIA, they might meet other standards like the ICVCM’s Core Carbon Principles. These principles are still new but more information will be available on this framework and how the CORSIA credits will be aligned under it.

Balancing CORSIA-eligible credits with quality non-CORSIA ones (like Plan Vivo or Puro.earth credits) can help manage budget and availability issues caused by CORSIA. This mix allows better predictions of availability and less impact from price changes.

Stakeholders who value CORSIA credits might face increased demand and prices. To manage this, they might buy CORSIA credits being assessed by the ICVCM early. This way, they can avoid potential demand impacts caused by meeting the Core Carbon Principles’ criteria.

-

It’s important for credit buyers to discuss how they see CORSIA’s impact on credit quality with stakeholders.

Some might follow CORSIA’s lead strictly, so it’s wise to avoid buying CDM credits to match their preferences. Others might be more flexible, choosing more non-CORSIA credits to reduce risk when buying.

CORSIA’s latest review of carbon credit standards signifies a pivotal moment for airlines and non-airline buyers alike. Credit buyers should adapt their strategies to account for increased demand, pricing shifts, and explore a balanced mix of CORSIA-eligible and other high-quality credits to show commitment to real carbon reduction.