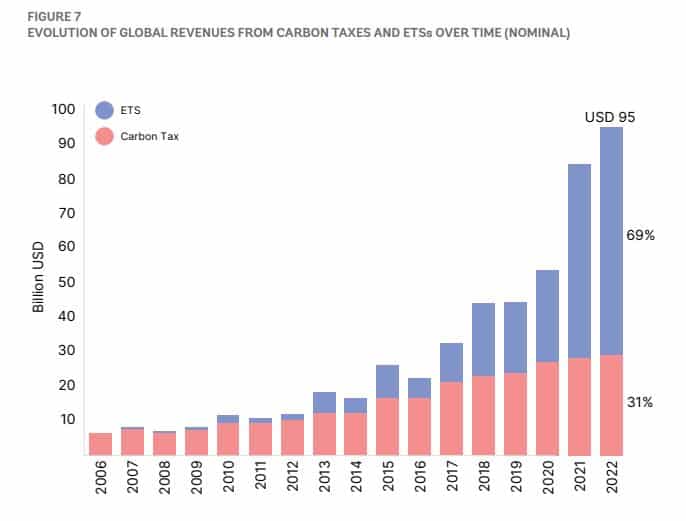

Amid the global energy crisis and economic issues, revenues from carbon credits traded in emissions trading systems (ETS) and carbon taxes hit record high in 2022 reaching almost $100 billion, per the World Bank carbon pricing report.

Carbon pricing is an essential policy tool useful in decarbonizing global economies. Through various instruments, carbon prices bring economic incentives to make climate-friendly changes in consumption, production, and investment.

The World Bank’s State and Trends in Carbon Pricing 2023 report provides an updated overview of the existing and emerging carbon pricing instruments worldwide. It also explores the trends and drivers of those instruments, including carbon taxes, carbon crediting mechanisms, and emissions trading systems.

As highlighted in the report, carbon pricing has to continue growing, in price and coverage, to drive climate action and meet the Paris goals. Here are the six key takeaways from the World Bank carbon pricing report.

#1. Carbon prices growth slowed but showed resilience

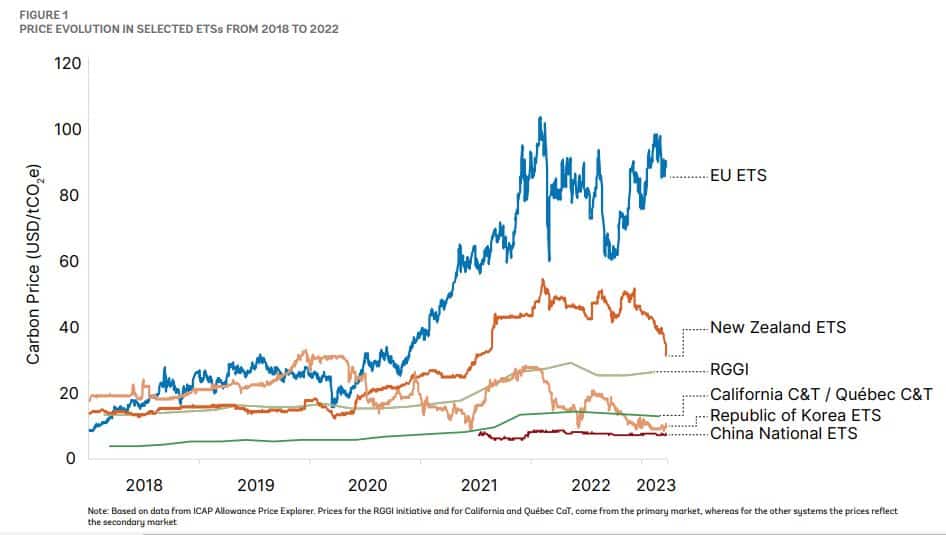

After years of high growth, carbon prices in ETSs and carbon taxes had slowed but showed resilience. They have made it through the global energy crisis last year, and even half of the instruments’ prices have increased. About a third have the same prices while fewer than 15% decline.

The European Union ETS recorded the largest increases, with price surging 100 Euros for the first time. It is linked with the Switzerland ETSs.

But in other ETS, carbon prices were down by up to 35% like the case of Republic of Korea ETS.

While some countries or jurisdictions toned down their plans to increase carbon prices, many didn’t. In fact, several of them decided to strengthen their existing ETSs and carbon taxes in the coming years.

For instance, Singapore made changes in its carbon pricing bill that will increase the nation’s carbon tax beginning in 2026, from USD 4-34 to USD 38-60. Likewise, Canada is pursuing its plan to increase its federal baseline to go over USD 127 by 2030.

Apart from policy changes, energy markets and drought were some of the biggest factors affecting carbon prices in most ETSs. In many European nations, the combined effects were enough to halt the declining trend in coal use while higher power sector CO2 emissions caused EU ETS to rise.

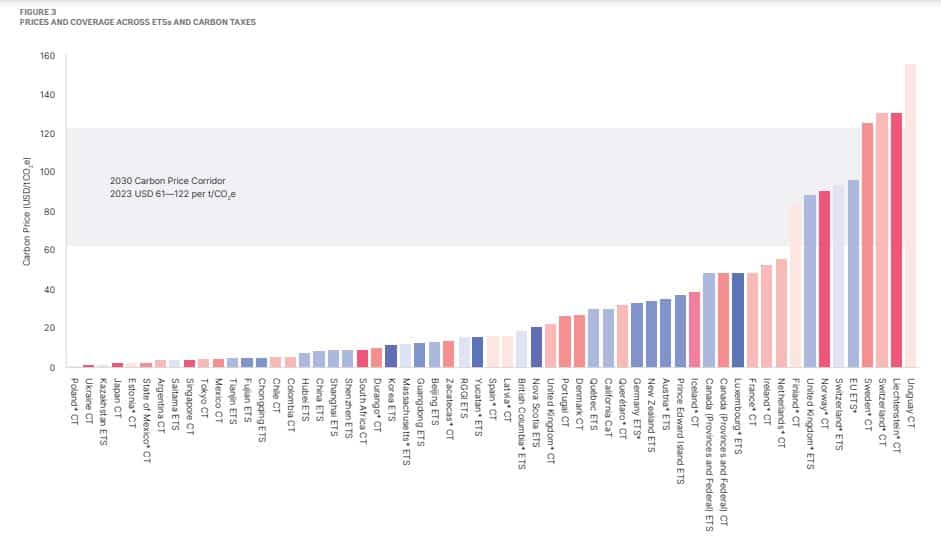

Overall, carbon prices have to grow in the long term to drive investments at the scale and pace needed. To keep global warming below 2°C, prices need to reach $50/tCO2 to $100/tCO2 by 2030. Factoring in inflation, that price range would be at $61 to $122 by 2030 in 2023 USD.

As of April 2023, under 5% of global GHG emissions are covered by a direct carbon price at or above the range suggested by 2030 (in 2023 US dollar value). Most of these high-price carbon pricing instruments are found in European countries as seen in the chart below. Blue shades refer to ETS prices while the pink ones represent carbon taxes.

#2. Number of ETSs and carbon taxes implemented slightly grew

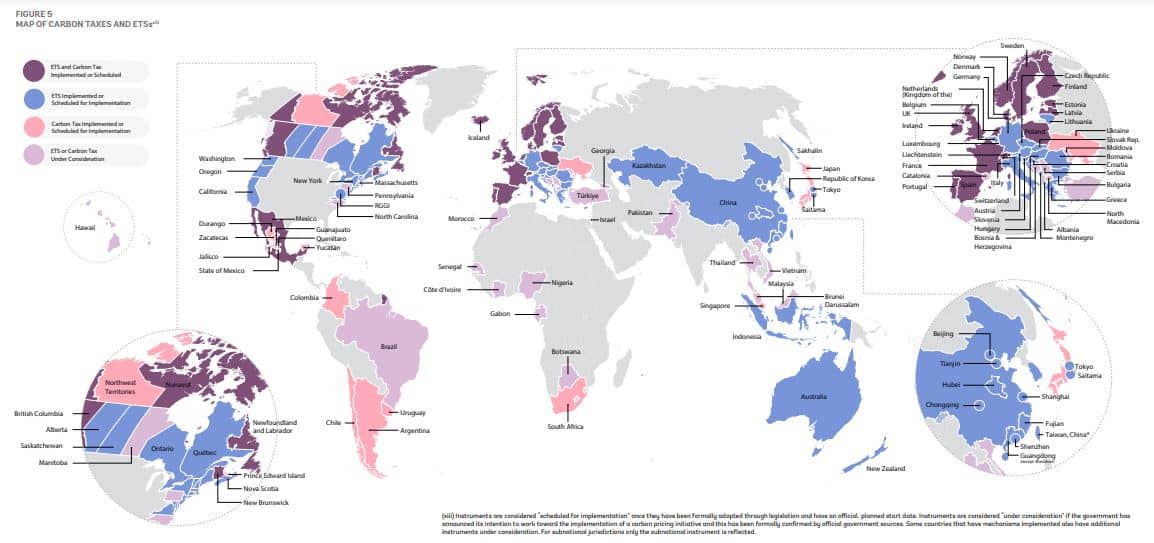

The number of ETS and carbon taxes adopted has gone up slightly to 73 as of April 2023. The increase is mostly in countries that are already pricing carbon, referring to the map below.

In 2022, several jurisdictions delivered on their existing plans for new ETSs or carbon taxes or increased their ambition. Some of them also revealed more proposals to develop new carbon pricing initiatives.

Emerging economies are showing growing interest in adopting carbon credit instruments but high-income nations still dominate the global market.

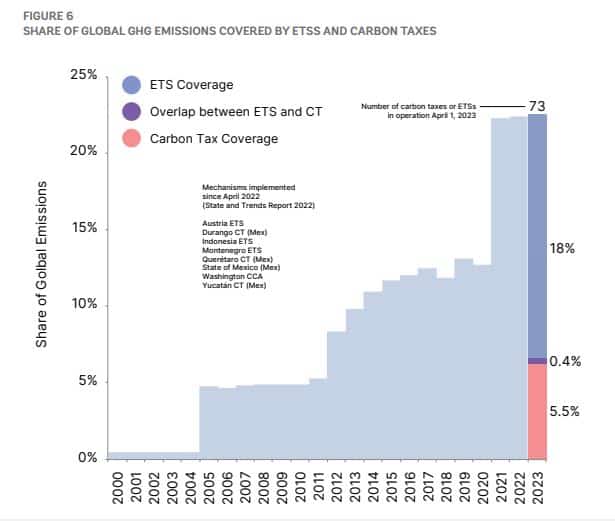

Overall, the little increase in the carbon instruments in operation cover about 23% of global carbon emissions. This rise represents a below 1% increase relative to the previous year.

Carbon pricing mechanisms today are mainly focused on energy and industrial emissions. Most carbon taxes cover certain fossil fuels used in different sectors, while ETSs often focus on big industrial facilities.

New Zealand will be the first country in the world to put a price on agricultural emissions in 2025. This is separate from the country’s existing ETS and will be applied at the farm level.

While other countries are also considering the creation of future ETS such as Malaysia, Vietnam, and Thailand, for instance. Meanwhile, Taiwan and China early this year passed a law to introduce a carbon tax on heavy emitters.

#3. Record high carbon revenues almost at $100 billion

This is perhaps the highlight of the report. Total carbon revenues from ETSs and taxes jump by over 10% in 2022, hitting about $95 billion. Compared to last year, the increase is worth $10 billion.

Carbon revenues are the product of the carbon price, specific emissions covered, and other pricing design factors like rebates and allocation methods.

Revenue in the EU ETS alone has grown 7x from 2017 amounts, generating a total of $42 billion in 2022. The $7.8 billion increase accounts for over 76% of the total increase in global carbon pricing revenues. This is partly because of higher prices, but also due to the shift from free carbon allowance allocation to auctioning.

In 2022, ETSs represented about 69% of government income from direct carbon prices, while carbon taxes took the remaining 31%.

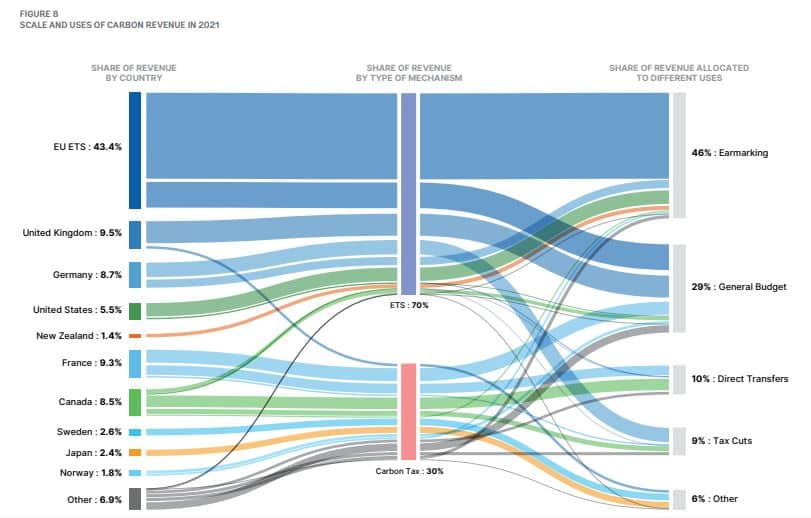

As to where the governments spend the carbon revenues, the following figure shows the percent share of different uses.

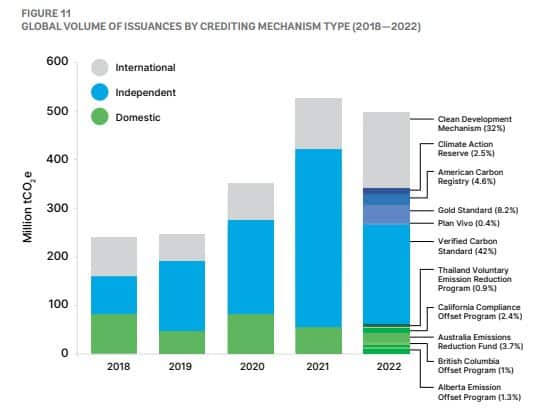

#4. Carbon credit markets slowed, and demand is mostly voluntary

After 2 years of steep growth, carbon credit markets slowed last year, with a +1% drop in retirements from 2021. A total of 196 million carbon credits were retired in 2022.

- The supply of new carbon credits and demand from end users decreased a little bit, reversing the previous year’s increase.

As seen below, independent crediting mechanisms or voluntary carbon markets supply most of the credits. But credit issuances from international mechanisms like the Clean Development Mechanism (CDM) grew in 2022, representing 30% of total issuance.

Voluntary corporate use of carbon credits remains to be the major source of demand in the market.

Also, more and more nations are thinking about establishing their own carbon credit mechanisms. This plan is often in conjunction with an ETS or carbon tax policy.

For example, both Indonesia and Vietnam made some preparations to establish domestic carbon credit schemes while South Africa assessed their internal standards to produce credits.

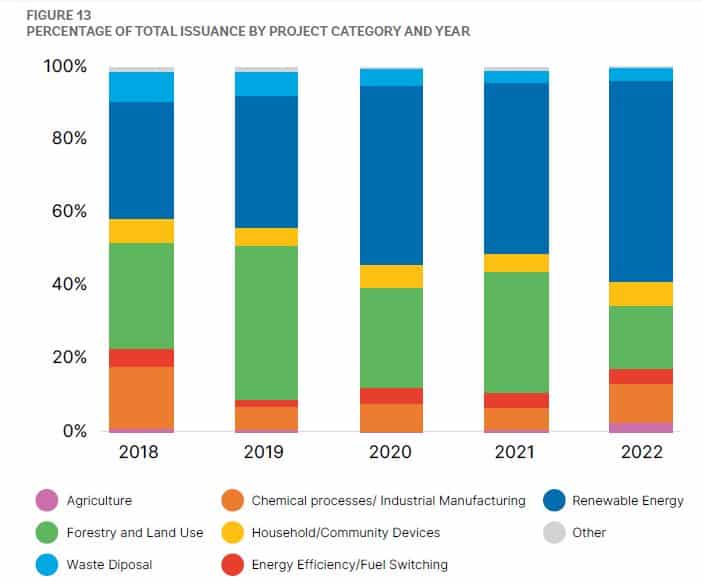

#5. Nature-Based carbon credits may overtake Renewable Energy

Renewable energy still dominates carbon markets. The share of carbon credits generated by renewable energy activities has been rising since 2018. They represent about 45% of registered projects and account for 55% of credit issuances in 2022.

In terms of carbon credits retired last year, 52% came from renewable energy projects, up from 44% in 2021. Renewable energy credits (RECs) are still widely available and among the cheapest credit types.

But as the cost of renewable energy fell significantly over the last 10 years, RE projects may no longer need the extra revenues from carbon credits. This signals that the value of RECs will eventually go down.

Thus, the supply of carbon credits from large RE projects will most likely decline over time. Some voluntary carbon crediting schemes have restricted eligibility, particularly for projects in the least developed nations.

Meanwhile, there has been a growing focus on nature-based activities. These include projects involving emissions reductions from agriculture and forestry and land use. The credits they produce often deliver co-benefits – other socio-economic benefits aside from carbon reduction – valued by many buyers.

Though credit issuances from forestry and land use activities drop in 2022, this may change soon, according to industry experts. Last year, 54% of new projects registered were for nature-based solutions, indicating a potential for supply expansion in the future.

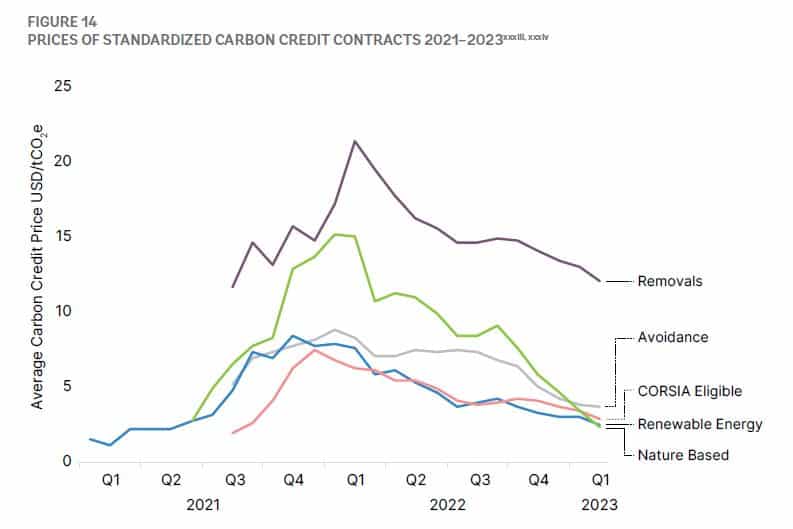

#6. Exchange-traded credits from removal projects trade at a premium

Carbon credit prices and trends vary across market segments and project types. Nature-based credits saw the highest price drop, from as much as $16 to below $5.

The rising use of standardized contracts is considered one factor of a downward trend in prices as seen below.

The price gap across most credit types or categories has narrowed, with exchange-traded credits from removal projects trading at a premium. Compared to carbon allowances traded in an ETS, carbon credits are heterogeneous.

Carbon credit prices vary due to several factors such as project type, credit issuer, credit vintage, and co-benefits. Hence, prices of different credit types vary a lot, reflecting project costs as well as buyer preferences. Newer credits sell at higher prices, according to Xpansiv CBL’s 2022 trading data.

Lastly, the carbon credit market continues to grow in diversity and sophistication, per World Bank’s report. More service providers, advanced technological platforms, improved products, and new investors will further drive market growth.

And as more countries sign deals to produce credits from emissions reductions and new integrity initiatives develop, standardization and transparency in the carbon credit market will follow soon.