Xpansiv released its carbon trading insight for 2022, here are some key takeaways.

2022 was a tough year for global financial and commodity markets, including the voluntary carbon market (VCM).

Many VCM traders became more cautious due to macroeconomic conditions and the Russian invasion of Ukraine. This leads to a 32% decline in CBL trading volume in H2 2022.

VCM-specific metrics also decreased, with issuances down 6% and retirement growth slowing to 2% due to concerns about carbon credit integrity.

Despite these challenges, the VCM proved to be resilient and continued to develop its market structure.

Trading of spot standardized contracts increased by 97% as shown below, providing better price transparency and liquidity.

The volume of CME Group’s CBL emissions futures rose by 345%. This indicates a strong market adoption of these contracts for managing price risk in a regulated market.

This article will examine data from Xpansiv’s spot market, CBL, to provide an overview of how the VCM evolved and matured in 2022.

The article will cover major trends in the VCM. These include changes in trading volume, the emergence of new markets, and the impact of global events on the market.

Short Term Pain for Long Term Gain

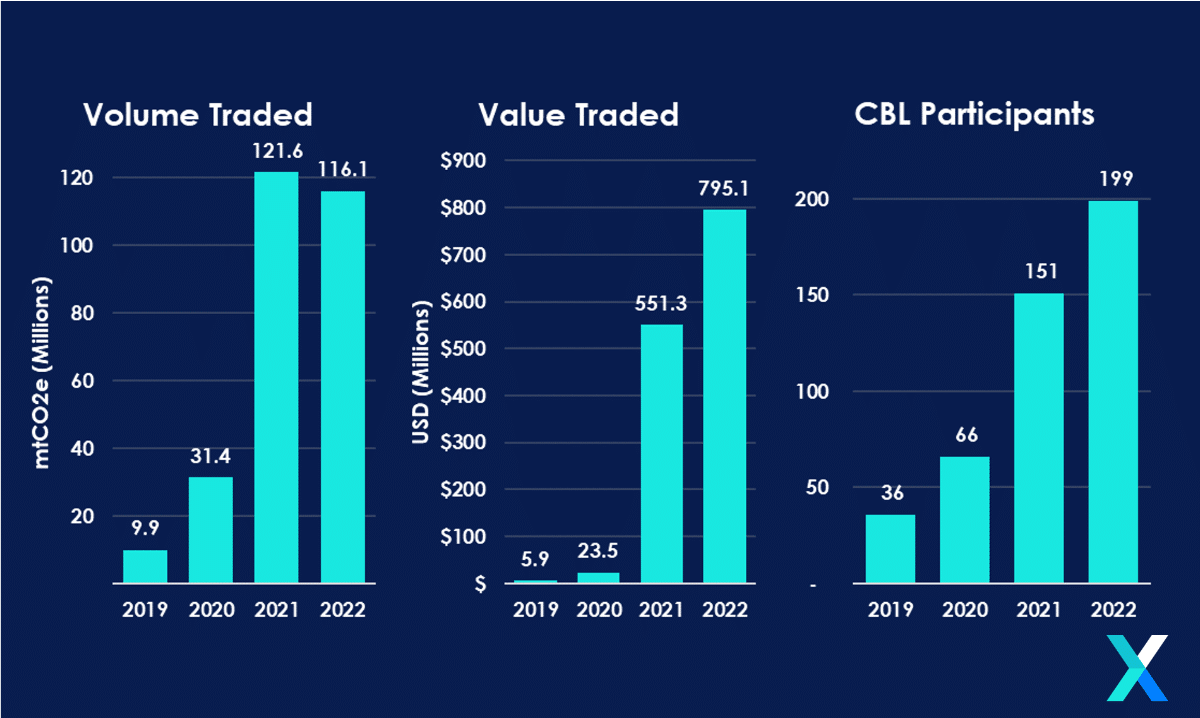

Despite slow trading, the voluntary carbon market (VCM) continued to grow in 2022.

Credits traded on CBL increased by 44% to over $795 million USD, and volume traded totaled 116 million tons, only 6% less than 2021.

The number of firms transacting in CBL’s spot market increased to almost 200 firms, up 32% from 2021.

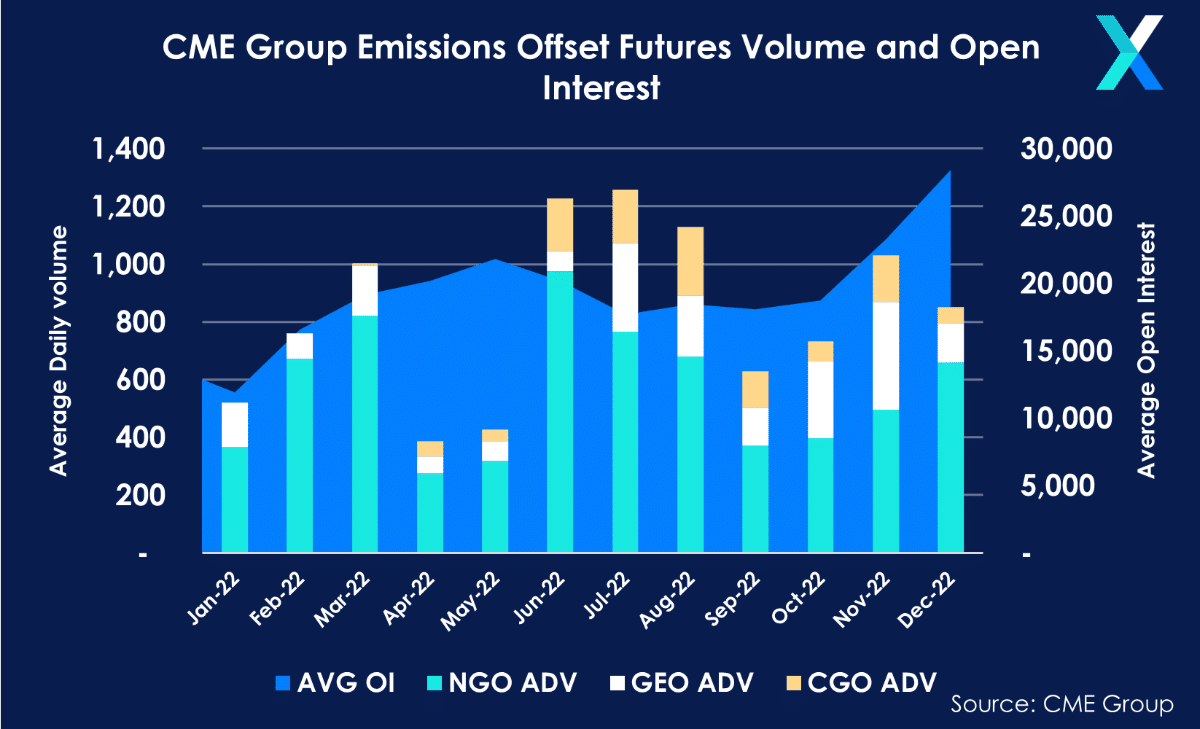

The derivatives markets also grew, with CBL GEO futures contracts traded by CME Group exceeding 209 million credits.

Average daily volume for the contracts rose by 281% to 835 contracts (equivalent to 835,000 credits).

Open interest on the contracts also increased throughout the year. It peaks above 29 million tons in December, indicating strong market participation.

Standardized Carbon Contracts are Growing

Usage of standardized spot market contracts saw significant growth in 2022. Volume traded through spot GEO contracts on CBL increased by 97% from 2021 levels, up to 32.3 million tons.

The portion of total CBL volume traded through standardized contracts increased as well, peaking at 38% of spot volume in Q3 2022. Standardized contracts provided the market with clear price signals throughout the turbulence of 2022. It allows market participants to quickly evaluate specific market segments.

Among the standardized contracts, the N-GEO emerged as the most prominent VCM benchmark. In particular, N-GEO volume accounted for 31.5% of CBL spot contract volume, and over 68% of futures volume.

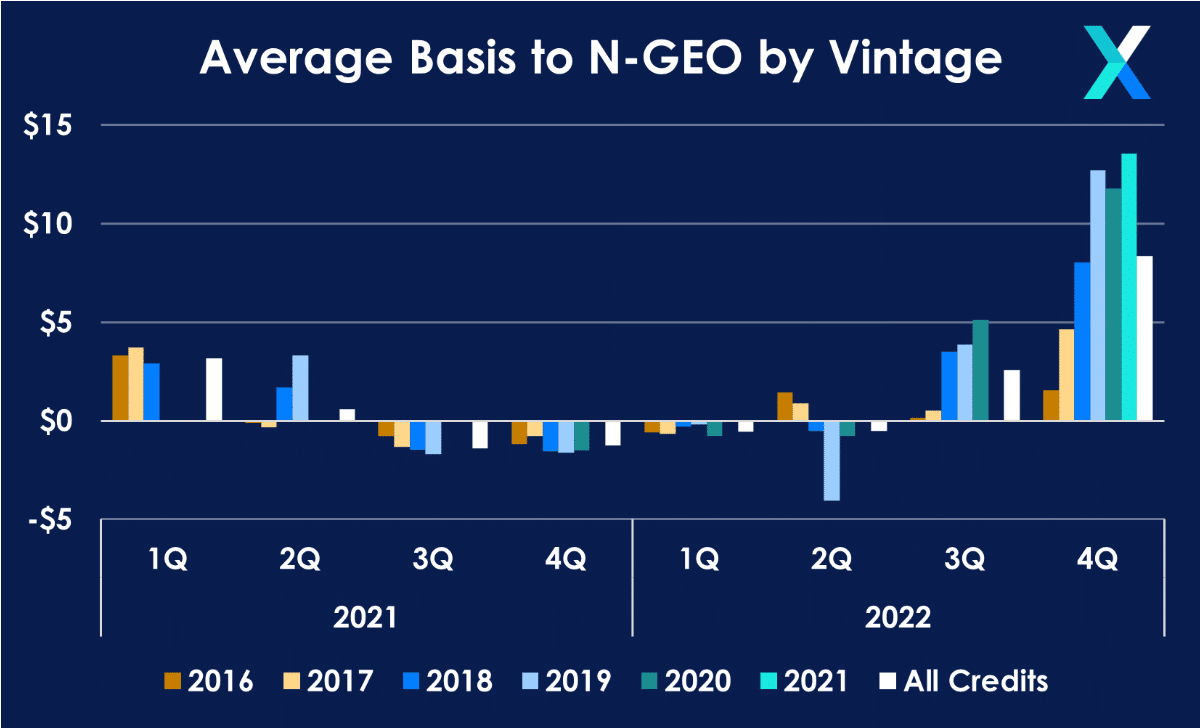

Basis Carbon

In 2022, a new trend emerged in the VCM called basis trading.

Basis trading involves pricing project-specific credits with additional attributes compared to standardized contracts like N-GEO.

Vintage was the most significant driver of premiums for eligible credits, with more recent credits achieving higher premiums.

Basis trading provides market participants with price transparency and expanded flexibility in project-specific credit transactions.

It also introduces clear and transparent pricing stratification in the VCM, with standardized contracts acting as a price floor for qualifying carbon credits.

As the VCM evolves and market sentiment shifts, standardized contracts will continue to produce price signals for the baseline qualification criteria. New indicators of value may be considered for future standardized contracts.

Growing Demand for High Quality

There was also an increasing demand for high-quality credits in the voluntary carbon market (VCM) in 2022.

Market participants were seeking credits with higher integrity and verifiability due to public attention towards credit integrity.

This resulted in the launch of the Sustainable Development Global Emissions Offset (SD-GEO) contract, which traded at significant premiums to other standardized contracts.

The SD-GEO contract accepts delivery of credits from clean cookstove projects with five or more verified SDG contributions.

Additionally, market liquidity for removals credits increased as the first blue carbon issuances became available, achieving record high prices above $30 on CBL.

These developments demonstrate the VCM’s evolving focus on quality and verifiability in carbon credits.

2022 VCM by Region and Project

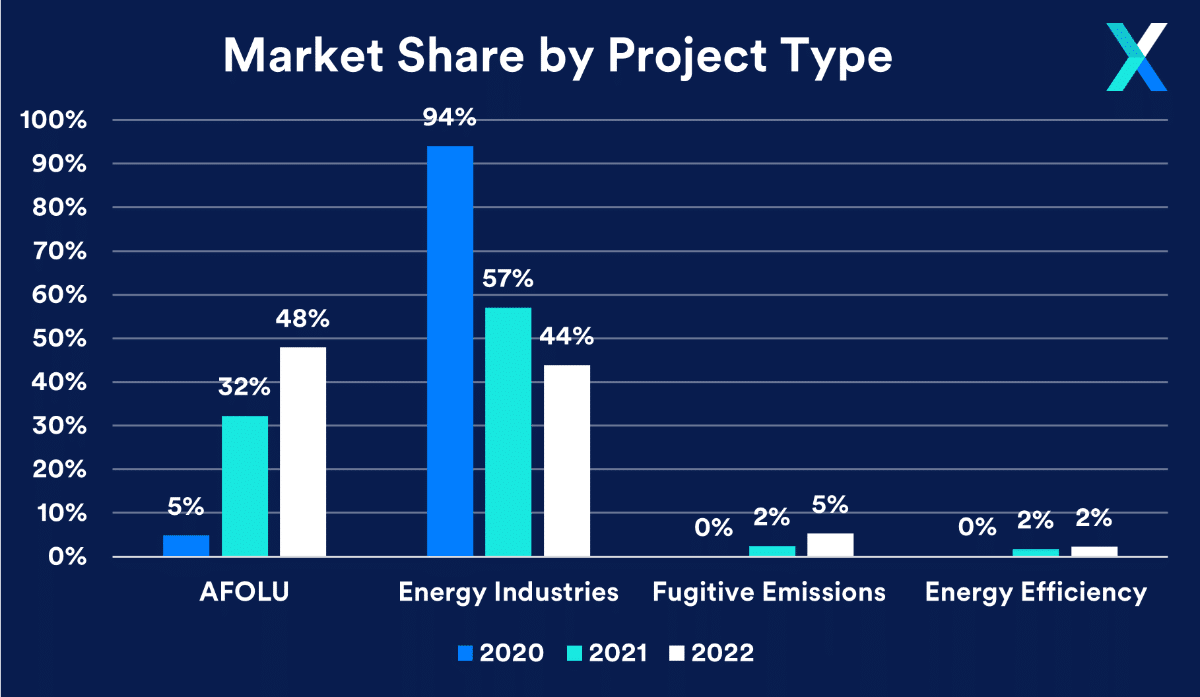

Project-specific credits traded on CBL totaled 74.7 million tons in 2022, revealing additional trends in the VCM.

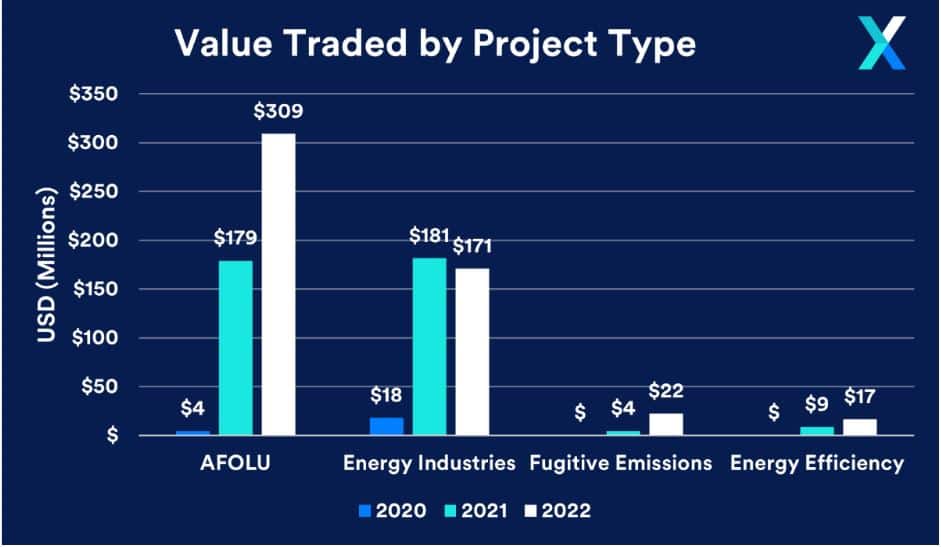

Nature-based credits, including AFOLU credits, became the most popular type of credit traded, surpassing energy industry credits.

The nature-based market share reached 48% of volume, with value traded exceeding $309 million, up 72% from 2021.

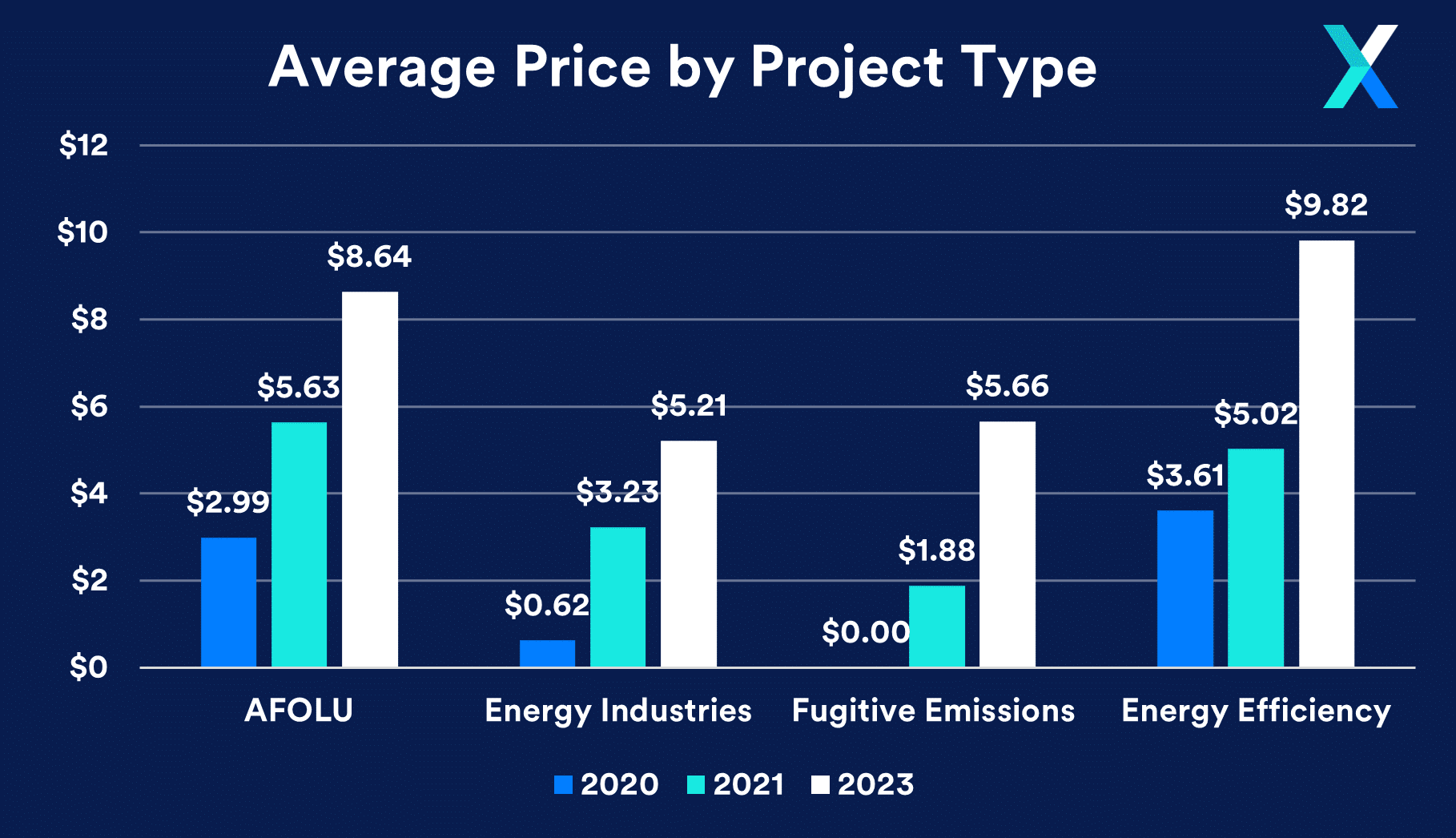

The average price of nature-based credits rose to $8.64 in 2022, making them the highest priced offsets, except for niche energy efficiency credits that averaged $9.82 per credit.

Xpansiv makes granular data generated from these transactions available through a subscription service.

These trends show a growing focus on nature-based solutions in the VCM, and the increasing importance of verifiability and integrity in carbon credits.

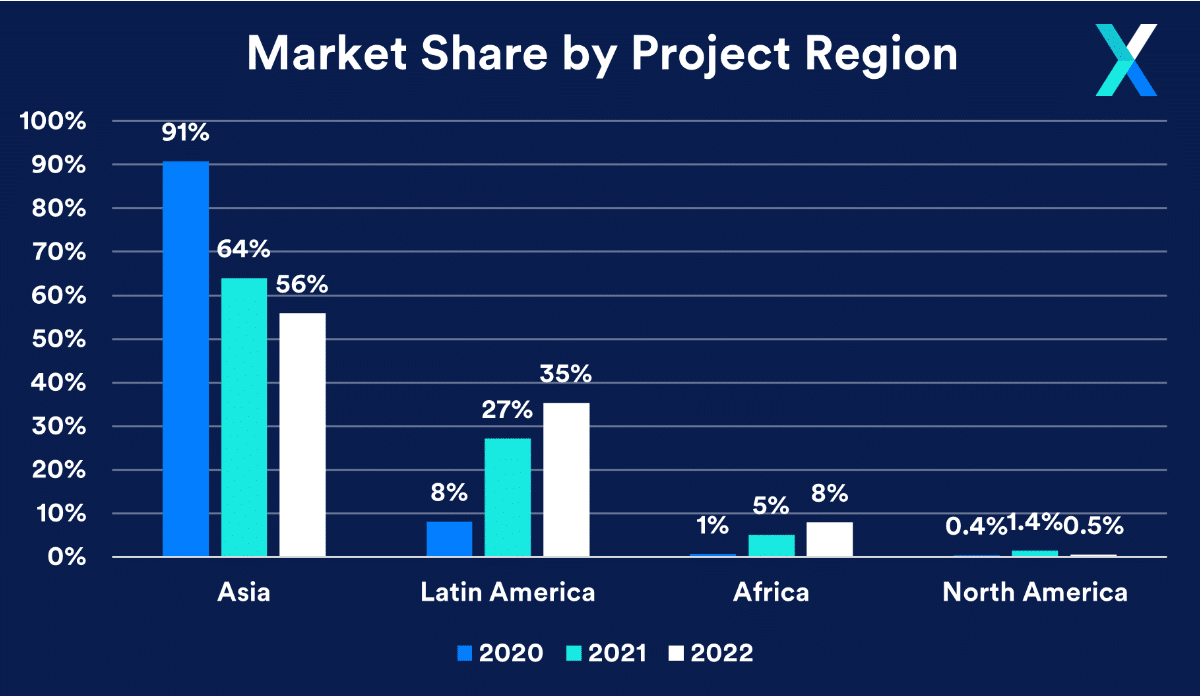

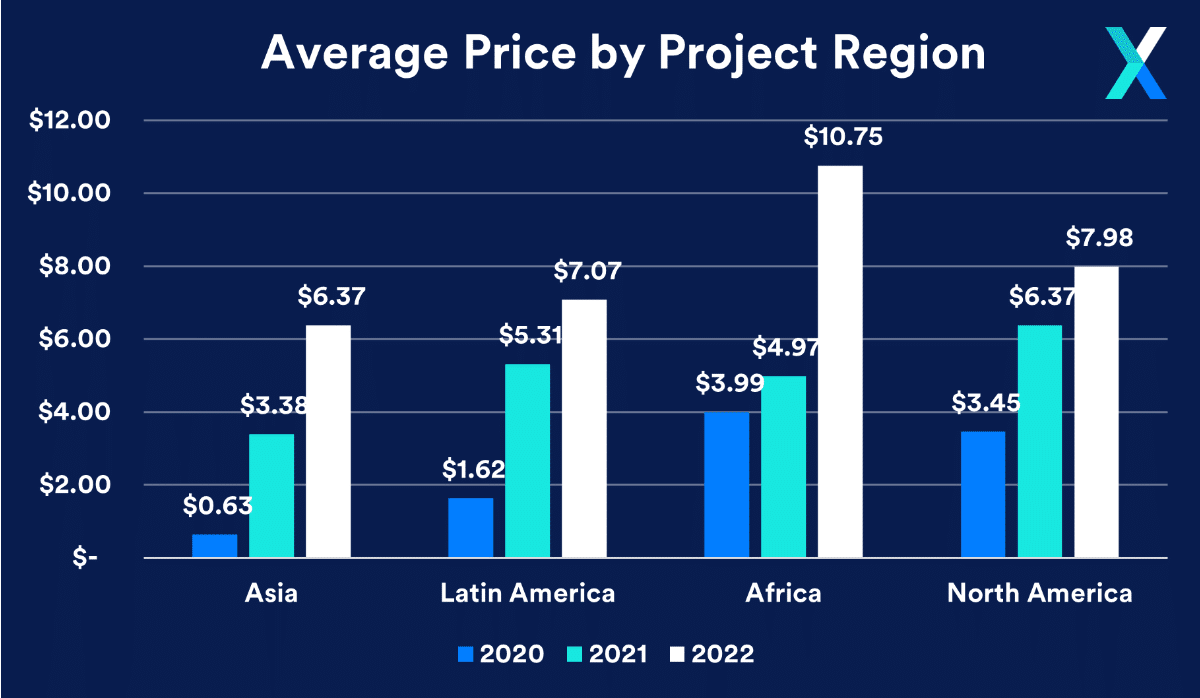

The share of traded credits generated from projects in Asia decreased in 2022, falling to 56% of CBL’s project-specific market.

Asian energy industry credits grew by 42% in 2022, and the rise of Latin American nature-based credits whose market share rose to 32%.

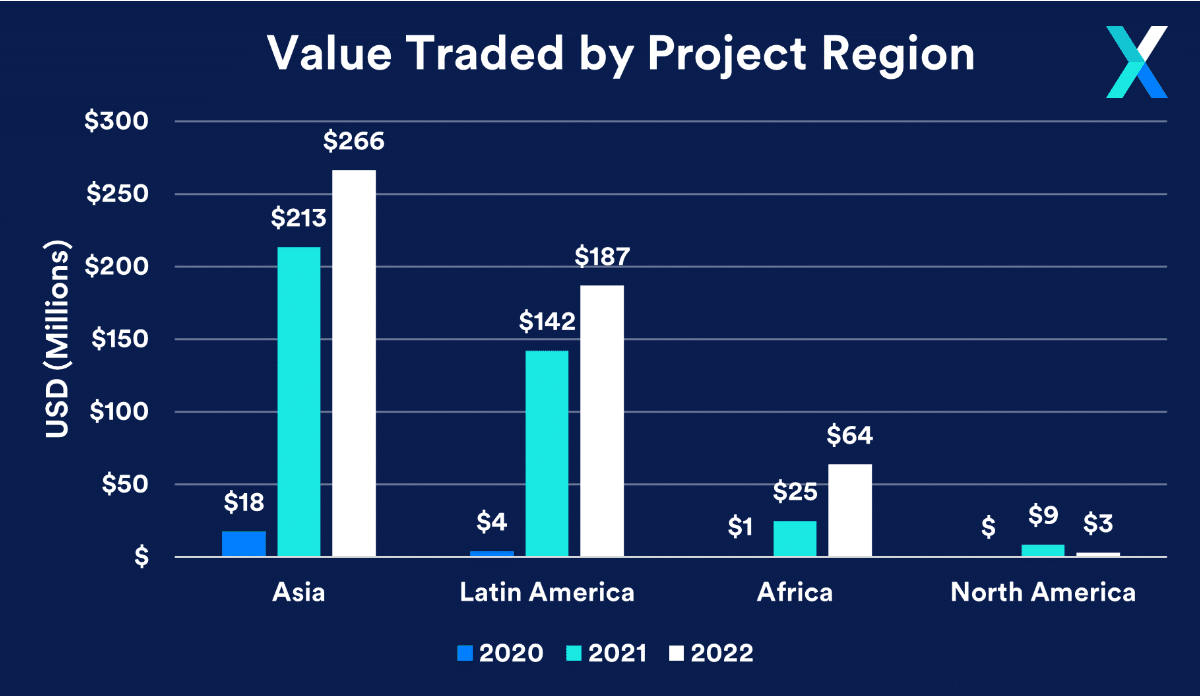

The African segment of the market saw significant growth in 2022, jumping to 8% of the market by volume with over $63.6 million in value traded.

The growth in the African segment was primarily driven by trading of nature-based credits, which rose by 164% to 3.9 million tons.

Lastly, the average price of credits from Africa was the highest among all regions at $10.75 per credit.

Read Xpansiv’s full report here.