The artificial intelligence (AI) boom has entered a new phase. It is no longer just about innovation or market dominance. Instead, it is now deeply tied to energy demand, emissions, and capital discipline. As a result, the rapid expansion of AI infrastructure is pushing Big Tech into an uncomfortable position—balancing climate commitments with rising environmental costs.

Data compiled for CNBC by carbon management platform Ceezer shows a sharp rise in carbon credit purchases across the sector. Companies are scaling AI aggressively, yet at the same time, they are leaning more heavily on carbon markets to offset the emissions they cannot yet avoid.

This shift is not happening in isolation. It reflects a broader structural tension between growth, sustainability, and financial performance.

AI Expansion Is Driving Both Emissions and Offsets

Tech giants such as Alphabet, Microsoft, Meta, and Amazon are collectively expected to spend close to $700 billion this year to scale their AI capabilities. This includes building hyperscale data centers, deploying advanced chips, and expanding global cloud infrastructure.

However, these investments come with a high environmental cost. AI systems require vast computing power, which in turn demands continuous electricity and cooling. Water use is also rising, particularly in large data center clusters. Consequently, emissions are increasing even as companies reaffirm their net-zero ambitions.

This is where carbon credits play a growing role. Each credit represents one metric ton of carbon dioxide either reduced or removed from the atmosphere. By purchasing these credits, companies aim to offset emissions that remain difficult to eliminate in the short term.

Yet this approach raises a fundamental question. Are carbon credits acting as a bridge to decarbonization—or becoming a substitute for it?

A Market Surge Signals Structural Dependence

The scale of growth in carbon credit purchases suggests a structural shift rather than a temporary adjustment.

In 2022, permanent carbon removal purchases across these companies stood at just over 14,000 credits. Within a year, that figure jumped dramatically to 11.92 million. The momentum did not slow. Purchases increased to 24.4 million in 2024 and then surged to 68.4 million in 2025.

This exponential rise highlights how quickly AI-driven emissions are feeding into carbon markets. More importantly, it shows that demand for high-quality removal credits is accelerating faster than supply.

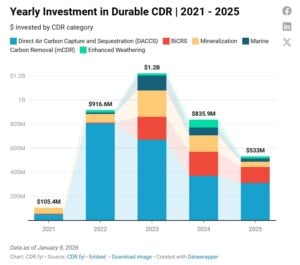

At the same time, companies are not relying on a single solution. Their portfolios include nature-based projects such as forestry and soil carbon, alongside engineered approaches like direct air capture. Long-term offtake agreements are also becoming more common, helping secure future credit supply while supporting project development.

However, the rapid increase in demand raises concerns about market depth. High-integrity carbon removal credits remain scarce, and scaling them is both capital-intensive and time-consuming.

Microsoft Sets the Pace—but Questions Remain

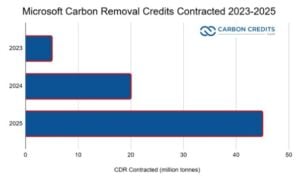

Among its peers, Microsoft has taken a clear lead in carbon removal efforts. The company reported a 247% increase in credit purchases between fiscal 2022 and 2023, followed by a further 337% jump in 2024. Growth continued into the next fiscal year, roughly doubling again.

More notably, Microsoft expanded its carbon removal agreements to 45 million metric tons of CO₂ in 2025, up from 22 million tons the previous year. These agreements span multiple geographies and technologies, reflecting a diversified approach to carbon removal.

The company is now a top climate leader, intending to become carbon-negative by 2030. Its strategy emphasizes reducing emissions first and then removing what cannot be avoided.

However, a key gap remains. It has not explicitly tied its carbon credit strategy to its AI expansion. While the correlation is clear, the lack of direct disclosure leaves room for interpretation.

This ambiguity is not unique to Microsoft. It reflects a broader issue across the sector, where sustainability narratives are evolving faster than reporting frameworks.

- MUST READ: Microsoft Q2 FY26 Earnings: $81B Revenue, AI Momentum, and a 150% Jump in Water Use by 2030

Free Cash Flow Pressures Are Becoming Harder to Ignore

While environmental concerns are rising, financial pressures are also building.

The CNBC report further highlighted that the scale of AI investment is unprecedented. As companies ramp up spending, free cash flow is beginning to decline. The four largest U.S. tech firms generated a combined $237 billion in free cash flow in 2024. That figure dropped to $200 billion in 2025, and further declines are expected.

This trend signals a shift in capital allocation. Companies are prioritizing long-term growth over short-term financial efficiency. However, this comes at a cost. Lower cash generation reduces flexibility and may increase reliance on external financing.

For instance, Alphabet raised $25 billion through a bond sale in late 2025, while its long-term debt rose sharply to $46.5 billion. This move underscores how even cash-rich companies are turning to debt markets to sustain their AI ambitions.

For investors, the implications are significant. The AI story remains compelling, but it now comes with margin pressure, delayed returns, and increased financial risk.

- ALSO READ: Google Bets Big on Next-Gen Nuclear and Carbon Credits from Superpollutants For a Greener AI

Renewables Help Stabilize Emissions—but Not Fully

Despite the rise in emissions, the increase has not been as steep as some feared. This is largely due to the rapid adoption of renewable energy.

Hyperscalers have expanded their clean energy portfolios, securing power purchase agreements and investing in renewable projects. As a result, they have been able to offset part of the additional demand created by AI workloads.

Ceezer’s data suggest that while emissions rose alongside AI growth, the increase was relatively moderate. This indicates that companies are responding quickly by integrating renewable energy into their operations.

However, this strategy has limits. Renewable energy can reduce operational emissions, but it cannot fully eliminate the impact of rapid infrastructure expansion. As AI demand continues to grow, the gap between emissions and reductions may widen.

Stricter Rules Are Reshaping Carbon Credit Use

At the same time, the regulatory landscape for carbon credits is becoming more stringent. New frameworks are redefining how companies can use offsets within their climate strategies.

Initiatives such as the VCMI Scope 3 Action Code now allow limited use of high-quality credits, but only under strict disclosure conditions. Meanwhile, the Science Based Targets initiative (SBTi) continues to refine its guidance, particularly as Scope 3 emissions remain difficult to reduce.

The challenge is substantial. The global Scope 3 emissions gap is estimated at 1.4 billion tonnes and could increase significantly by 2030. This creates pressure on companies to find credible solutions without over-relying on offsets.

In parallel, disclosure frameworks such as CSRD are pushing companies to provide detailed explanations of their carbon credit strategies. This includes justifying project selection, verifying credit quality, and demonstrating measurable impact.

The direction is clear. Carbon credits are no longer a simple compliance tool. They are becoming part of a broader accountability framework.

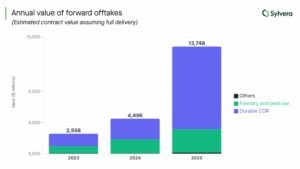

Carbon Removal Market Expands—but Supply Constraints Persist

The carbon removal market is growing rapidly, yet it remains constrained.

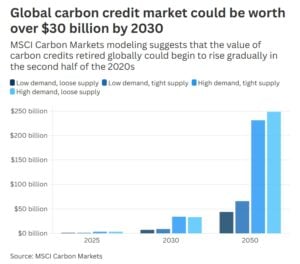

MSCI Projections suggest the global carbon credit market could exceed $30 billion by 2030. Corporate demand for carbon removal credits may surpass 150 million metric tons annually within the same timeframe.

However, supply is struggling to keep pace. High costs remain a major barrier, particularly for advanced technologies such as direct air capture, where prices often exceed $100 per ton.

In 2025, offtake agreements reached $13.7 billion, reflecting a strong corporate commitment. Yet these agreements will deliver only 78 million credits over the next decade. Actual durable carbon removal credits retired in the same year remained below 200,000.

This mismatch highlights a key issue. While demand is accelerating, real-world deployment is lagging. As a result, the market faces both growth potential and structural limitations.

The Bottom Line: A Delicate Balancing Act

Big Tech’s AI expansion is reshaping both the digital economy and the carbon market. On one side, companies are investing heavily in future growth. On the other hand, they are navigating rising emissions, tighter regulations, and increasing financial pressure.

Carbon credits are playing a critical role in bridging this gap. However, they are not a long-term solution on their own.

The path forward will require a more balanced approach—one that combines technological innovation with real emissions reductions and transparent reporting. Companies must prove that their climate commitments are more than offset strategies.

At the same time, investors will need to adjust expectations. The AI boom promises strong returns, but it also introduces new risks. Lower cash flow, higher capital intensity, and evolving climate obligations are all part of the equation.

Ultimately, the success of this transition will depend on execution. The companies leading the AI race must now show they can scale responsibly—without compromising either financial stability or climate credibility.