Albemarle Corporation, one of the world’s largest lithium producers, has closed its Kemerton lithium hydroxide processing plant in Western Australia. The company made the decision due to rising costs and competitive pressures in hard-rock lithium processing. The closure affects more than 250 jobs and dozens of contractors.

The Kemerton plant processed lithium from the Greenbushes mine and was intended to supply battery-grade lithium chemicals. Albemarle invested over US$4 billion in the site, but the facility never reached its target performance. The company cited structural challenges and higher operating costs compared with plants in China.

The shutdown highlights difficulties in building competitive lithium processing outside China. China currently dominates lithium refining and battery supply chains. Many Western firms have struggled to build profitable chemical conversion capacity, even with recent lithium price improvements.

Solid Earnings, Shaky Investor Sentiment

Albemarle reported its fourth-quarter and full-year 2025 earnings in mid-February 2026. The company posted net sales of US$1.4 billion, up about 16% year-on-year, driven by growth in energy storage volumes and pricing. Adjusted earnings before interest, tax, depreciation, and amortization (EBITDA) rose about 7% compared with 2024.

Despite these positive metrics, Albemarle’s stock fell sharply after the earnings release. Morningstar reported that on February 12, 2026, shares fell about 7%. This drop happened during a wider market sell-off. Still, the company’s profit outlook was better than what analysts expected.

Investors reacted to a mixed message from the earnings data. The company had sales growth and strong cash flow. However, the closure of the Kemerton plant and ongoing cost pressures affected sentiment. Some investors were cautious about near-term guidance amid global market volatility.

But Management Bets on a 2026 Demand Rebound

Despite short-term pressures, Albemarle’s management outlined a strong demand outlook for lithium in 2026. In a recent earnings call, company leaders projected that global lithium demand could grow by 15% to 40% in 2026.

This growth is driven in part by a sharp rise in stationary energy storage demand and continued EV adoption. Stationary storage includes large battery systems used for grid balancing, renewable energy smoothing, and data centers. These systems are becoming major new consumers of lithium-ion batteries.

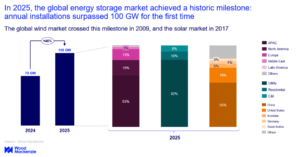

Industry reports say global energy storage installations more than doubled in 2025. This rise shows growing demand, extending beyond just electric vehicles.

Albemarle also reported that its free cash flow in 2025 was about US$692 million after cost controls and capital discipline. The company plans to keep capital expenditures steady in 2026. It will focus on boosting productivity and developing resources instead of expensive expansion projects.

EVs and Grid Storage Keep the Battery Boom Alive

Lithium is a key metal for lithium-ion batteries. These batteries power electric vehicles (EVs), grid storage systems, portable electronics, and more.

Electric vehicle adoption continues to grow globally. The International Energy Agency says EV sales hit around 20 million units in 2025. This makes up nearly 25% of all car sales globally. EVs alone account for about 75% of total lithium demand in 2025 in battery markets.

In addition, stationary energy storage systems are becoming more common. Battery storage helps balance renewable energy like wind and solar on the grid. Storage growth is part of broader climate and energy policies in many countries.

- Demand growth is also supported by new battery applications, such as data centers and backup power systems.

Some market analysts expect global lithium demand to more than double by the decade’s end. This will depend on EV adoption rates, renewable energy growth, and storage needs.

- MUST READ: How BESS and Lithium Demand Are Shaping Energy Storage: Global Shipments to Surge 50% in 2025

Processing Bottlenecks and Price Swings Complicate Supply

While demand is rising, the supply side of lithium faces challenges.

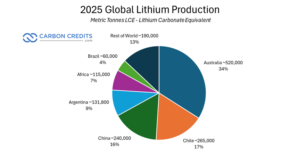

Mining output increased sharply between 2021 and 2025. Australia, Chile, and China expanded production during that period. However, processing capacity, especially outside China, has lagged.

The closure of Albemarle’s Kemerton plant underscores these supply constraints. Western plants face higher labor, energy, and infrastructure costs compared with counterparts in China. These factors make lithium hydroxide production less profitable in some regions.

China dominates downstream lithium processing and battery cell production. The country holds 60–70% of the world’s lithium chemical processing capacity. It also makes around 75% of lithium-ion batteries, based on data from the International Energy Agency.

- RELATED: China’s One Month Lithium Battery Energy Storage Installations Beat America’s One Whole Year

At the same time, some supply projects have delayed expansion, held back by financing costs, permitting hurdles, and fluctuating prices.

Price volatility has been a feature of the lithium market over the past few years. After reaching multiyear highs in 2022, lithium carbonate prices plunged through 2023 and 2024 due to oversupply. Prices bounced back in late 2025 and further skyrocketed in early 2026.

Cost Cuts and Capital Discipline Take Center Stage

Albemarle’s recent actions illustrate how lithium producers respond to shifting conditions.

The company cut costs, lowered capital spending, and sold non-core assets to boost its balance sheet. These moves helped Albemarle generate strong free cash flow even with price swings.

Management noted cost and productivity gains of US$100–150 million aimed for 2026. This will help boost profit margins, particularly in energy storage segments.

Albemarle’s strategy focuses on maintaining stable operations while positioning for long-term demand growth. This includes optimizing asset portfolios, managing supply chains, and shifting production toward lower-cost channels.

Other companies in the lithium sector are also adapting. Some are concentrating on mining expansions, processing partnerships, and technology improvements. Others are exploring recycling and alternative battery chemistries to reduce reliance on lithium.

Miners like Pilbara Minerals, SQM, and Sigma Lithium are expanding and optimizing supply. They do this to stay competitive during price cycles. Refiners like Ganfeng Lithium and Tianqi Lithium are expanding their conversion capacity. They are also integrating their supply chains.

Moreover, firms like Standard Lithium and EnergyX are developing direct lithium extraction methods. These aim to boost recovery and lower water impacts. Recycling companies like Redwood Materials, Li-Cycle, and Umicore are expanding systems. They recover lithium and other metals from used batteries.

Battery makers such as CATL are also investing in sodium-ion technology, which can reduce lithium demand in some market segments.

A Tightening Market in the Making?

The lithium market continues to evolve. There are signs of a structural shift as demand grows faster than supply in some scenarios.

Analysts expect that demand from EVs and energy storage will keep pushing lithium consumption up for the rest of the decade. Albemarle’s plant closure shows that supply issues and processing challenges might tighten the market. This could happen if new capacity isn’t ready soon.

Long-term forecasts suggest many countries and companies will need secure lithium sources. They will also need more downstream processing capacity to meet climate and clean energy goals.

For Albemarle, the mix of cost discipline, demand growth forecasts, and strategic positioning could help the company navigate a market that is both dynamic and competitive.