Lithium battery energy storage systems (BESS) are now an essential part of the world’s energy transition. These systems store electricity from wind, solar, and other clean power and help keep grids stable when demand rises.

In 2025, the BESS market grew at a record pace. China has taken the lead, and global demand for lithium batteries is climbing fast. These trends show how battery storage is reshaping energy systems around the world.

2025: A Record-Breaking Year in BESS Deployments

Lithium‑ion chemistry remains the dominant technology in both large‑scale and behind‑the‑meter storage systems. These batteries help balance power grids. They support renewable energy and allow utilities and businesses to use energy flexibly.

BESS installations are becoming essential for clean energy infrastructure. This is due to more renewables being added and demand for stable power increasing.

The year 2025 was a landmark year for lithium BESS installations. According to Benchmark Mineral Intelligence, around 315 GWh of battery energy storage capacity was installed worldwide in 2025. This figure represents nearly 50% year‑on‑year growth compared with 2024. China and the United States led global deployments, with China far outpacing all other countries.

A striking sign of China’s dominance came in December 2025. China installed 18 GW (65 GWh) of large‑scale battery storage in that month alone. That amount of capacity was greater than all the battery storage that the United States installed over the entire year. This shows how rapidly China has expanded its energy storage footprint.

Through October 2025, global grid‑scale BESS capacity reached 156 GWh, a 38 % increase from the same period in 2024. China contributed a significant share of this growth, but Europe, North America, and the rest of the world also showed gains in deployment.

Data from Benchmark Mineral Intelligence shows a clear trend: BESS capacity grew in several months of 2025. In October, installations surged by 29% compared to last year. China contributed around 8.8 GWh of new grid-scale capacity that month.

Global Lithium‑Ion Demand Skyrockets

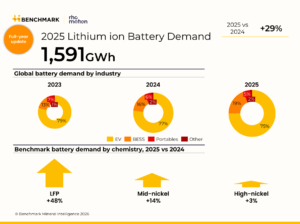

The surge in BESS deployment is part of a larger rise in lithium‑ion battery demand. In 2025, global demand for lithium‑ion batteries grew 29 %, reaching about 1.59 terawatt‑hours (TWh).

Energy storage growth in 2025 outpaced demand in the electric vehicle (EV) market. This increase came from both stationary storage and EVs.

Stationary storage demand in particular jumped by 51 % in 2025, compared with 26 % growth in EV battery demand. This shift signals that storage is becoming a major driver of lithium consumption alongside traditional EV markets.

Researchers highlight that battery chemistries also changed in 2025. Lithium iron phosphate (LFP) batteries grew faster than other cell types, with demand rising 48% year‑on‑year. China’s EV sector remains strong, but LFP’s share outside China also climbed to over 30 % of global battery demand.

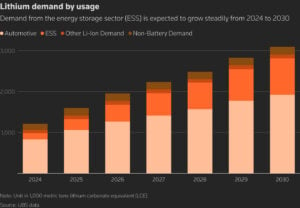

Industry analysis shows that global lithium use for energy storage may rise by 45.6% from 2025 to 2030. By 2030, it could reach about 312,934 metric tons. This forecast reflects the growing use of storage systems on power grids and for industrial demand.

Why China Leads the Storage Boom

China’s expansion in the BESS market traces back to sustained support and rapid industrial growth. China’s cumulative battery storage capacity doubled in 2024, reaching roughly 62 GW (141 GWh) by year‑end. Lithium‑ion batteries made up over 96 % of this capacity.

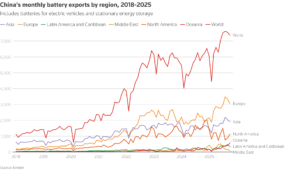

Chinese firms dominate both production and deployment. In 2025, Chinese manufacturers boost global shipments of lithium-ion cells for storage by around 75%. This growth is fueled by demands from power grids, renewable energy, and the expansion of data centers.

- Chinese exports of battery systems were valued at over $65 billion in the first ten months of 2025, reflecting strong global demand.

China’s leadership also stems from policy reforms that improve storage economics. Changes in market rules have allowed more battery storage to operate profitably. Batteries that can capture price differences throughout the day now have stronger business cases. This shift encourages more installations and higher utilization of grid‑connected storage.

Energy Storage: The Grid’s New Backbone

Lithium BESS installations play an important role in supporting the clean energy transition. Storage systems help keep electrical grids stable even when wind or solar power is variable. These systems can store excess renewable electricity during low demand and release it in times of high demand.

This capability helps grids handle peak demand and reduces the need to rely on fossil fuel peaking plants. It also helps spread renewable energy. It smooths out output and offers backup when sunlight or wind decreases. As renewable energy generation expands, storage will remain critical to grid flexibility.

The growth of storage also reflects falling battery costs. Battery pack prices for stationary storage dropped significantly in 2025.

Some industry reports say stationary storage costs dropped to about $70 per kilowatt-hour. This makes it one of the cheapest parts of the battery market. Lower costs help accelerate deployment and make storage investment more attractive for utilities and developers.

Looking Forward: Challenges, Innovation Paths, and Projected Growth

While growth remains strong, the battery storage sector faces some challenges. S&P Global forecasts a small drop in global storage installations in 2026. They predict capacity will fall by about 2.7% by 2025. This expected dip is linked to changes in China’s requirement for pairing storage with new solar projects.

Despite this short‑term dip, long‑term forecasts still point to strong growth through the 2030s as storage becomes central to grid modernization. Battery demand from grid installations is expected to rise even as some geographies adjust policies.

Beyond supply, the industry must also address innovation in long‑duration storage technologies. Lithium-ion systems still lead the market. However, alternatives like flow batteries and sodium-ion cells are starting to emerge. These technologies may help meet storage needs that require longer discharge durations.

Global production capacity for rechargeable lithium‑ion batteries is also growing rapidly. In 2025, total production capacity is set to surpass 2 TWh per year, having doubled from 1 TWh just a few years earlier. This expansion supports both EV demand and energy storage.

As storage continues to scale, its share of overall lithium demand is expected to grow. Some industry estimates suggest that by 2026, energy storage could account for around 31% of total lithium consumption, up from about 23 % in 2025. This shift underscores how storage is gaining ground relative to other uses like EV batteries.

China has emerged as the dominant force in both production and deployment. Its policy reforms and manufacturing scale are driving rapid growth. Meanwhile, falling battery costs and strong demand from grids and renewables are pushing stationary storage into the mainstream.

As BESS becomes more important for clean energy and grid reliability, investments, deployments, and innovations in lithium systems are likely to continue rising well into the next decade.